Every country is eventually faced with a decisive choice: to passively adapt to its circumstances or to redesign them. Mostchoose the former .They invoke geography, history, "objective constraints."

Few choose the latter. They treat development as a technical project—not as a historical accident. Over the past sixty years, countries as diverse as Singapore, Ireland, Estonia, South Korea, Israel, Rwanda, and the United Arab Emirates have proven that national transformation is not a mystery.

It is a project. The essential question is not why they succeeded. It is specifically what they did.

Common sense behind success

Despite their differences, successful countries followed a similar sequence of steps. First, they set a clear economic direction. They did not try to do everything. Then they created stable rules that inspired confidence in investors and citizens.

They studied what worked internationally and adapted it without ideological obsessions. They invested in education linked to production. And, most importantly, they maintained policy consistency for decades.

Growth was not a slogan. It was repeated implementation.

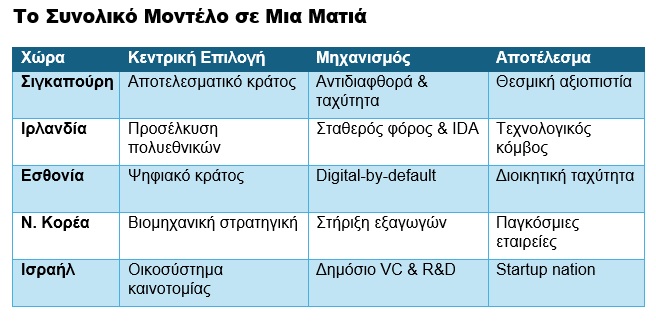

Singapore: The state became a competitive advantage

In 1965, after independence, Singapore was a small port with no natural resources and social instability. Its leadership understood that the economy would not grow unless the state functioned flawlessly.

So it started with the administration. Public officials were paid competitively and evaluated strictly. Corruption was punished immediately. Investment procedures were drastically simplified and a central business attraction service was created. At the same time, the country invested in infrastructure and public housing, ensuring social stability.

From a per capita income of around $500 in 1965, the country now exceeds $80,000. The message was clear: when the state operates with discipline, growth accelerates.

Ireland: A country that attracts investment

In the 1980s, Ireland faced high unemployment and mass emigration. Instead of waiting for investment, it decided to go out and get it.

It created a specialized agency, IDA Ireland, with the mission of directly approaching multinationals. It established a stable and low corporate tax rate, invested in universities with an emphasis on technology, and capitalized on the advantage of the English language within the European market.

It was no coincidence that the tech giants set up shop in Dublin. They were invited through decades of consistent policy. Per capita GDP skyrocketed from around $5,000 to over $100,000.

Estonia: A model for digital restart

After 1991, Estonia did not have the resources for a heavy public system. Instead of expanding it, it redesigned it digitally from scratch. It instituted digital identity for all citizens and adopted the principle that the state does not ask twice for data it already has. Almost all services were moved online, and starting a company became a matter of minutes.

Digitization was not a technological luxury. It was administrative reform.

South Korea: The epitome of developmental consistency

After the Korean War, the country was one of the poorest in the world. The government selected strategic industrial sectors and systematically supported them for decades. Funding was linked to export performance, and education was geared toward technology and engineering.

The crucial factor was not a single reform, but consistency. The strategy was maintained regardless of which government was in power. The country evolved from an agricultural economy into an industrial and technological hub.

Israel: Redesign through innovation

With no natural resources and under constant geopolitical pressure, Israel invested in knowledge. It created a public venture capital program that shared the risk with private investors, connected universities with businesses, and leveraged expertise from military research.

Innovation did not happen spontaneously. It was designed as a system.

From Rwanda to the UAE: First trust, then development

After the 1994 genocide, Rwanda began by restoring order, administrative discipline, and curbing corruption. It created an environment where rules were clear and enforced.

In the United Arab Emirates, the strategy focused on diversifying the economy. Special economic zones were created, business start-up procedures were simplified, and the state acted as an active investor.

In both cases, trust preceded prosperity.

What this means for Greece

Greece has significant advantages: European integration, a geostrategic location, a strong diaspora, and a high-level human resource base. The issue is not potential. It is institutional continuity and speed of implementation. International experience shows that progress requires:

- stable investment environment,

- a fast and digital state,

- clear productive direction with continuity.

None of these options are unknown. All have been tried and tested. Economic "miracles" were not the result of luck or a particular culture. They were the result of choices that were implemented consistently. National success is not inherited. It is built.

The examples are before us. The methods are known. The knowledge is available. The only question that remains is whether a country decides to use it.

Sources: World Bank – World Development Indicators (GDP, growth, investment), OECD – Economic Surveys and Policy Reviews, Transparency International – Corruption Perceptions Index, IDA Ireland – Official investment attraction strategy, e-Estonia – Digital state & public services, Israel Innovation Authority – Startup ecosystem and R&D policy, Lee Kuan Yew – From Third World to First, UAE Ministry of Economy – Economic policy and investment strategies

* Nicholas Havoutis has many years of experience in leading strategic financial units, having served as an executive at JPMorgan (New York), Chase Manhattan Bank (London), and Eurobank (Athens). At the same time, he has a significant presence in the media. Today, as head of SoZone Limited, he advises companies and investors on international development, organic optimization, and merger and acquisition strategies.