In light of international developments that are creating a climate of instability and uncertainty, according to the results of the tourism survey conducted in 2025, it appears that the tourism experience in Western Crete is rated overall as highly positive, a fact that confirms the destination’s solid standing as a strong and attractive tourism product.

The findings demonstrate that visitors form a positive impression of both the natural characteristics of the region and key aspects of the services provided, a factor that substantially contributes to their overall satisfaction.

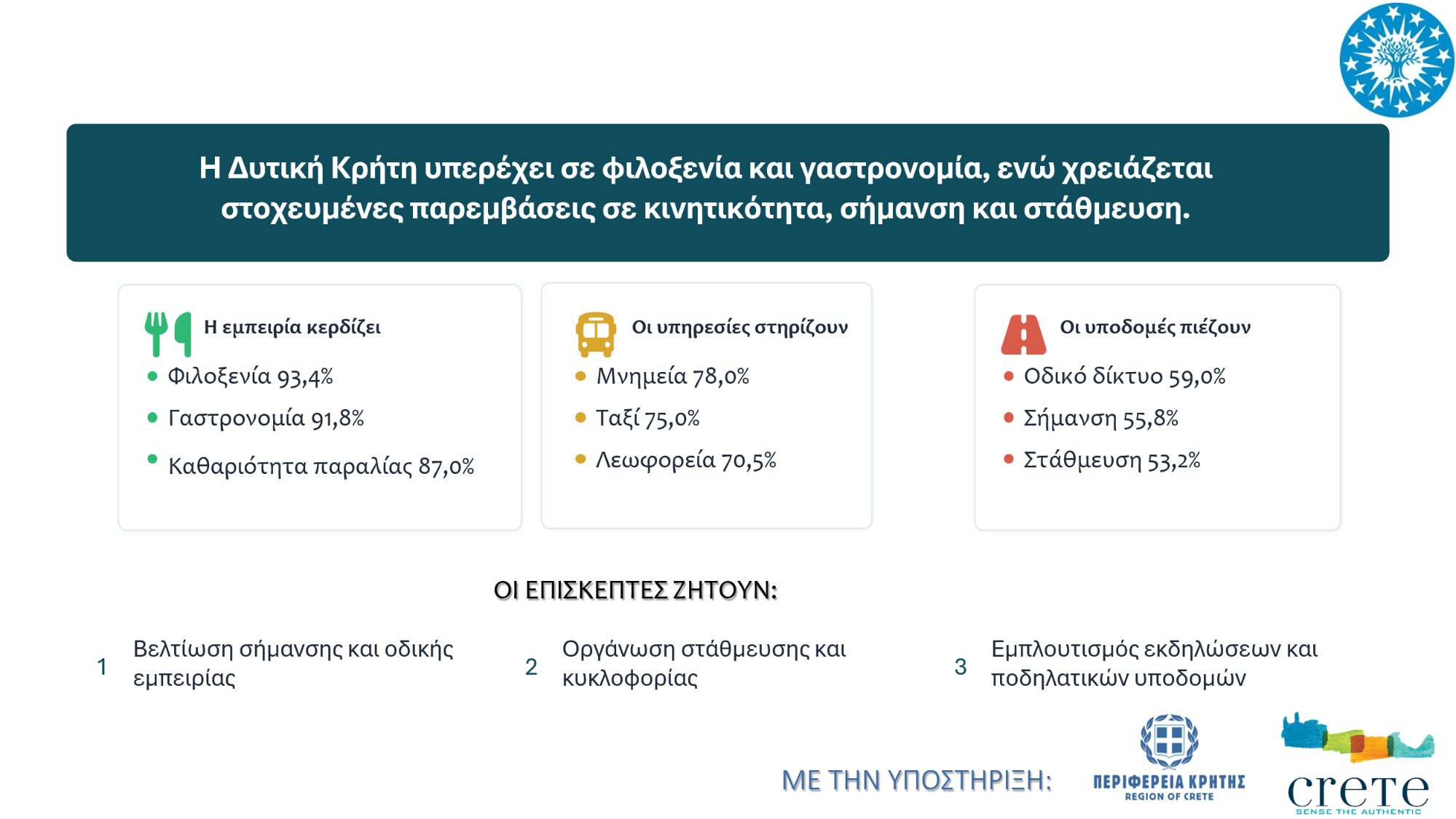

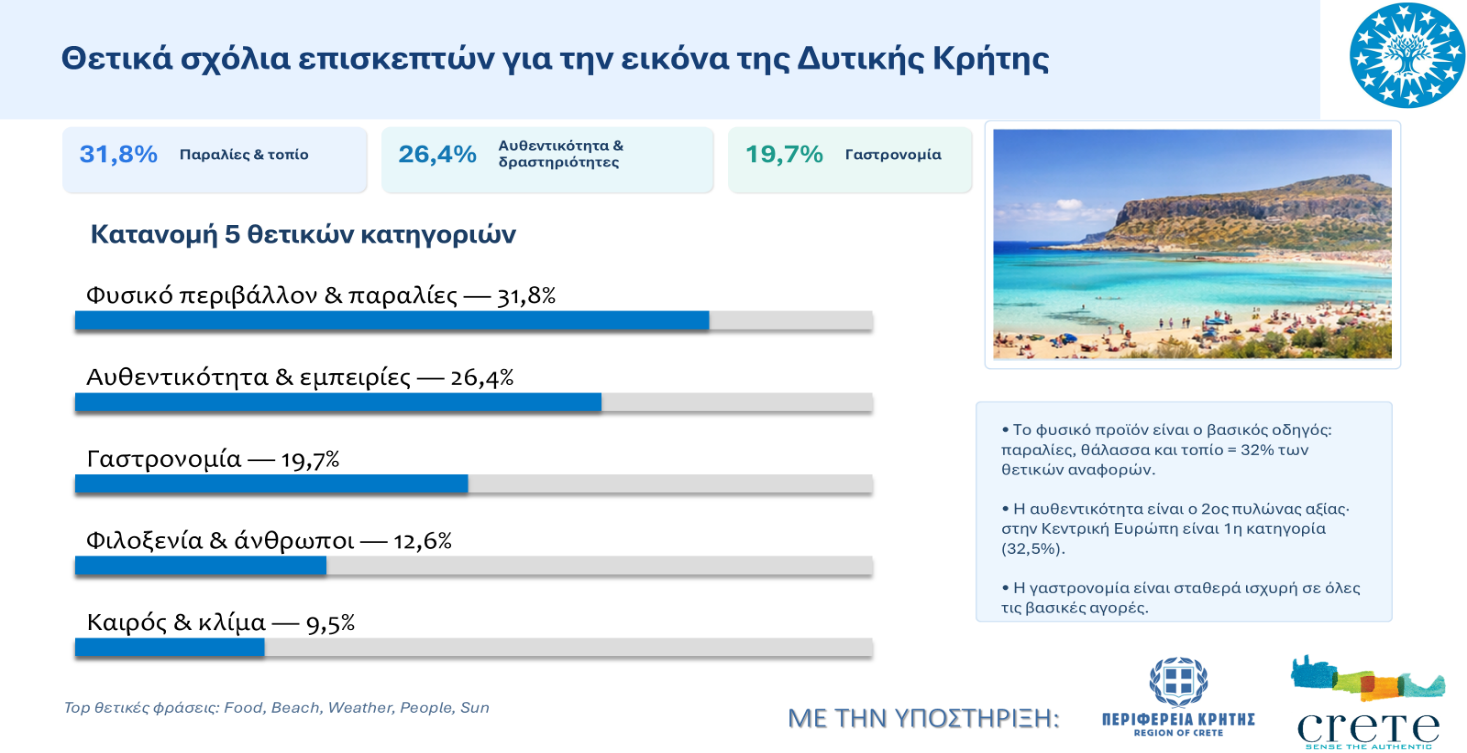

In particular, the highest ratings are recorded in areas related to the human element and the quality of the experiential aspect. Friendliness and hospitality, dining, Cretan cuisine, café and leisure services, as well as a sense of safety, constitute the key pillars upon which the positive evaluation of the destination is based.

This factor is particularly important, as it suggests that the competitiveness of Western Crete is not based solely on its natural resources, but also on the quality of human interaction and the preservation of an authentic hospitality experience. At the same time, the high ratings for the cleanliness of beaches and accommodations meet basic requirements for comfort, safety, and quality.

The Region of Crete’s participation in international trade shows and parallel events throughout the year in Crete contribute significantly to improving the destination’s image.

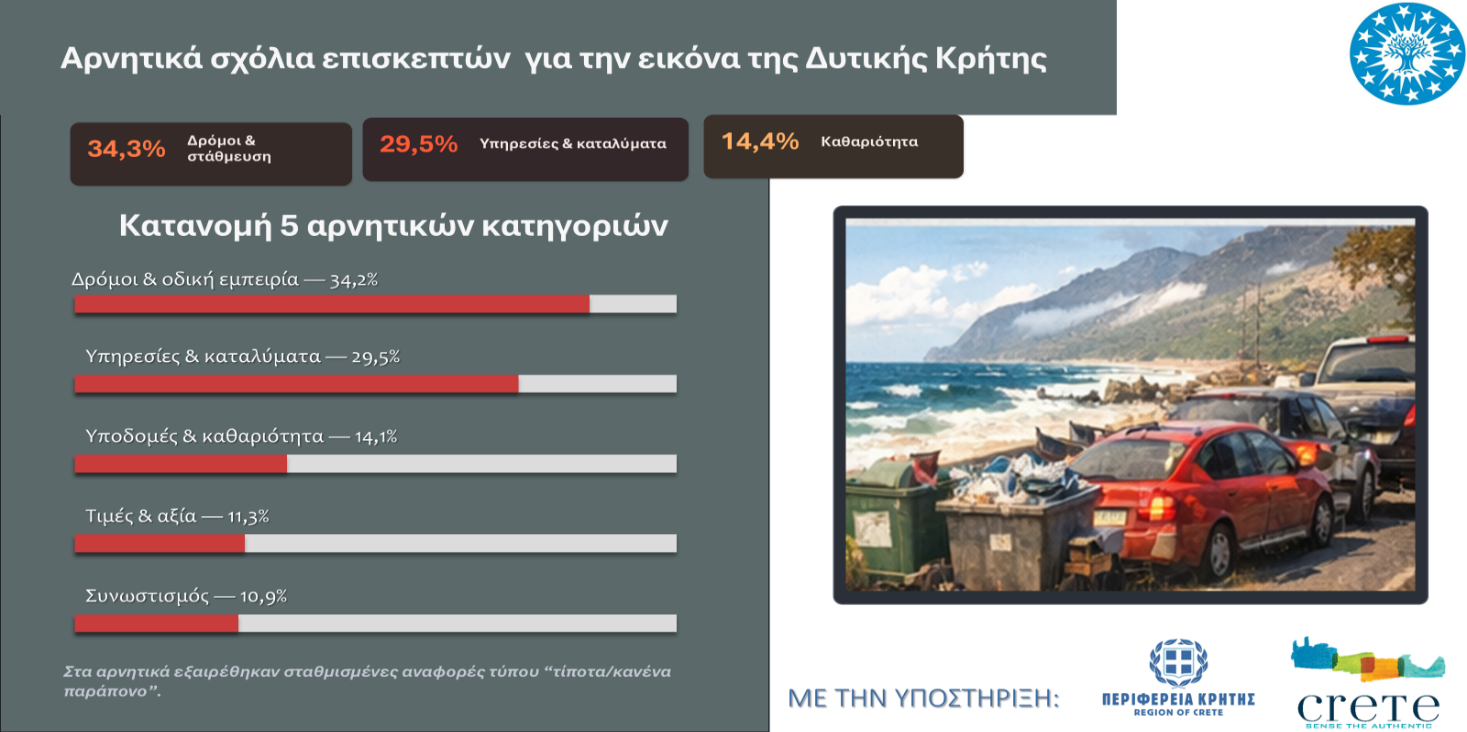

Despite the positive overall assessment, the survey also highlights certain weaknesses, which are mainly related to the operational aspects of the destination. The lowest scores are found in the road network, signage, traffic, parking facilities, and bicycle infrastructure.

Furthermore, these results indicate that the most significant difficulties faced by visitors do not concern the core of the tourist experience so much as issues of practical organization, accessibility, and mobility. Furthermore, the reckless use of plastic, particularly plastic bottles, necessitates proper management practices to reduce the carbon footprint on the environment.

Therefore, the key challenge for further enhancing the competitiveness of the Region of Crete lies in upgrading infrastructure and ensuring the sustainable management of the destination.

It should be noted that dissatisfaction rates regarding these services and infrastructure have decreased compared to previous years, a result of the efforts and actions undertaken by the Municipality of Chania, where despite the inconvenience visitors may experience due to ongoing construction projects, these are deemed absolutely necessary for the smooth functioning of the city.

According to the views of repeat tourists in particular, there is great anticipation for the reopening of the Central Municipal Market of Chania, where they will be able to sample and purchase local products; comments are also very positive regarding the widening of sidewalks, the creation of new parking spaces around the Center to relieve traffic congestion in the city, as well as the various cultural events, such as the Strata Festival, which attract their interest.

At the same time, the qualitative data from the presentation, through the thematic analysis of visitors’ comments, confirm this dual picture. On the one hand, positive comments focus mainly on the beaches, the natural landscape, the cuisine, authenticity, and hospitality.

On the other hand, negative comments primarily concern the roads, transportation, infrastructure organization, cleanliness in certain areas, prices, and overcrowding.

It is likely that overcrowding contributes to the very slight decline in positive comments (for the second consecutive tourist season) regarding service quality, as it suggests that the immediacy and friendliness of communication that characterized these tourism services are under strain.

Furthermore, for the 2025 tourism season, the increased pressure from the high flow of visitors results in tourism businesses approaching their capacity limits, a situation that may lead to higher prices, a decline in service quality, and infrastructure overload.

This contrast indicates that Western Crete possesses a strong and attractive core tourism product, which, however, requires operational support measures to make the destination more resilient, ensuring it continues to offer high-quality services.

Air Arrivals

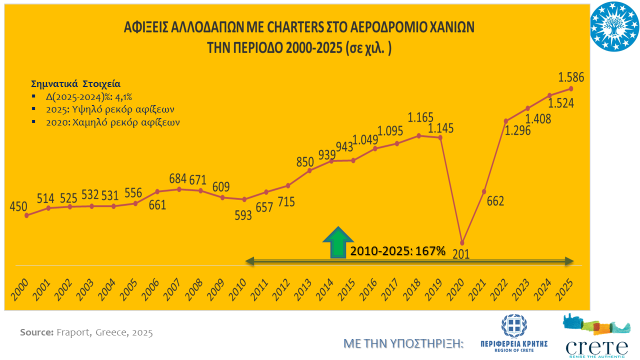

Regarding foreign tourist arrivals at Chania Airport and based on Fraport-Greece data for the year 2025, a record 1.6 million arrivals were recorded, marking a 4% increase compared to the previous year, 2024, when 1.5 million arrivals were recorded. This year’s increase, compared to 2024, is mainly attributable to non-Scandinavian visitors, who recorded a growth rate of 6.5%, while the number of Scandinavian visitors saw a slight decline.

Specifically among Scandinavians, the Danes recorded the largest increase at 3%, the Norwegians remained at the same levels, while the Swedes and Finns saw a 3% decrease. Overall, we observe that Scandinavians have stabilized at around 35% of total arrivals following the COVID-19 pandemic, whereas prior to that, their share had been established at around 50%.

This does not mean that Scandinavian arrivals are decreasing, but rather that non-Scandinavian arrivals are increasing at a much faster rate.

Regarding the main nationalities of non-Scandinavians, Germans, British, and Poles are the ones showing significant increases of 8%, 6%, and 5%, respectively. British and German visitors continue to hold the top two spots in total arrivals, accounting for 18% and 13% of total arrivals, respectively, while Polish visitors rank fourth with a share reaching 10%.

Visits

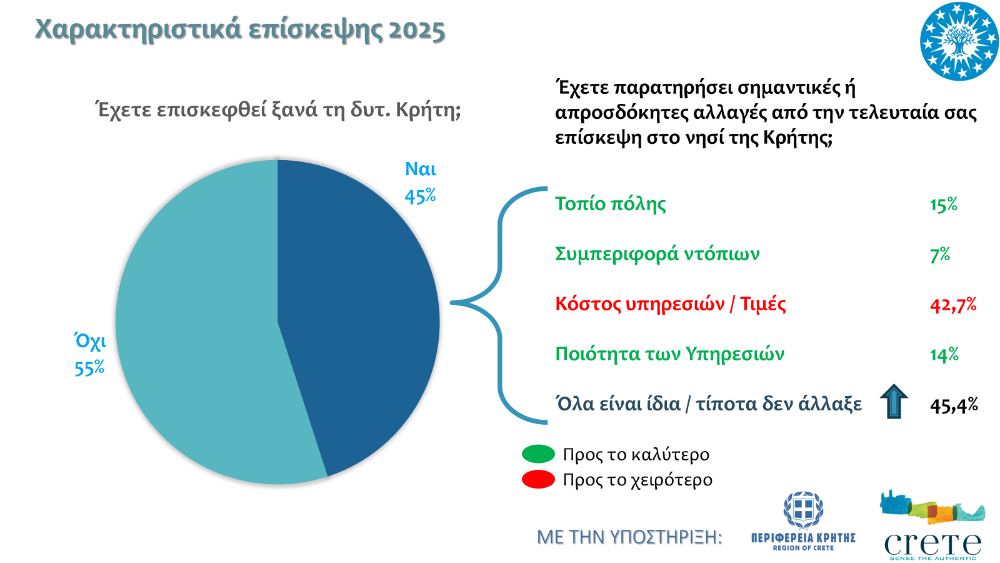

Compared to the previous year, this year, as in the past, a high percentage of foreign tourists are visiting Western Crete, with 45% of foreign tourists having visited Western Crete at least once in previous years.

Of those who had previously visited Western Crete, 45.4% did not notice any significant change—a percentage significantly higher than last year’s. Of the rest who did notice a change, four in ten cited higher prices and the increased cost of services, while 15% believe that the city’s landscape and the quality of services have improved, and 7% that the locals’ behavior has improved.

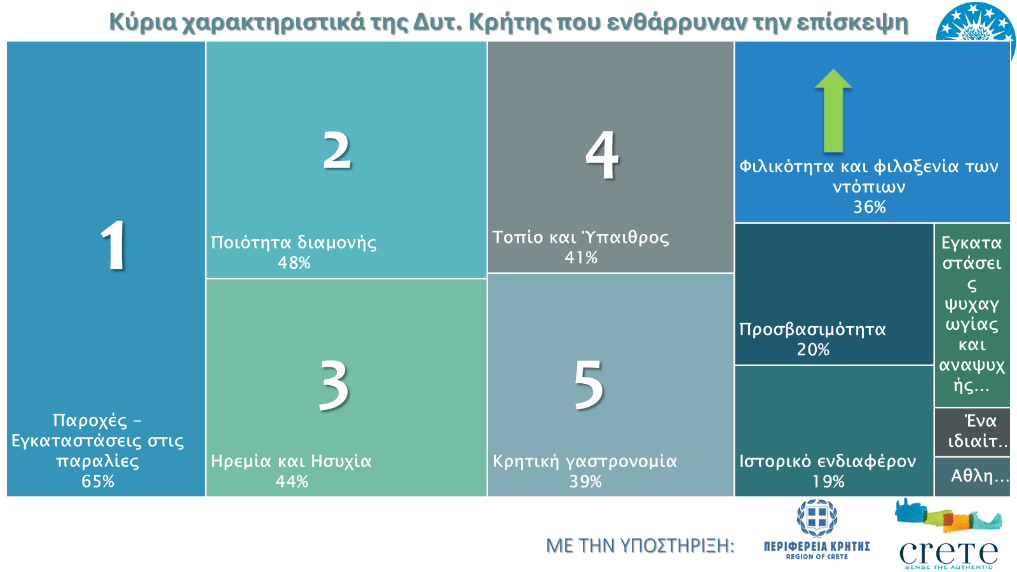

The main reasons tourists visit Western Crete remain the beaches (65%), the quality of accommodation (48%), the peace and quiet (44%), and the beauty of the landscape and countryside (41%). These are followed by Cretan cuisine (39%) and the friendliness and hospitality of the locals (36%), with percentages 5% higher than last year, constituting very strong incentives for choosing the region as a final destination.

Overall, the analysis shows that the tourism model of Western Crete remains primarily oriented toward the sea and the vacation experience, while alternative activities serve more as a complement than as the main focus of the visit.

Accommodation

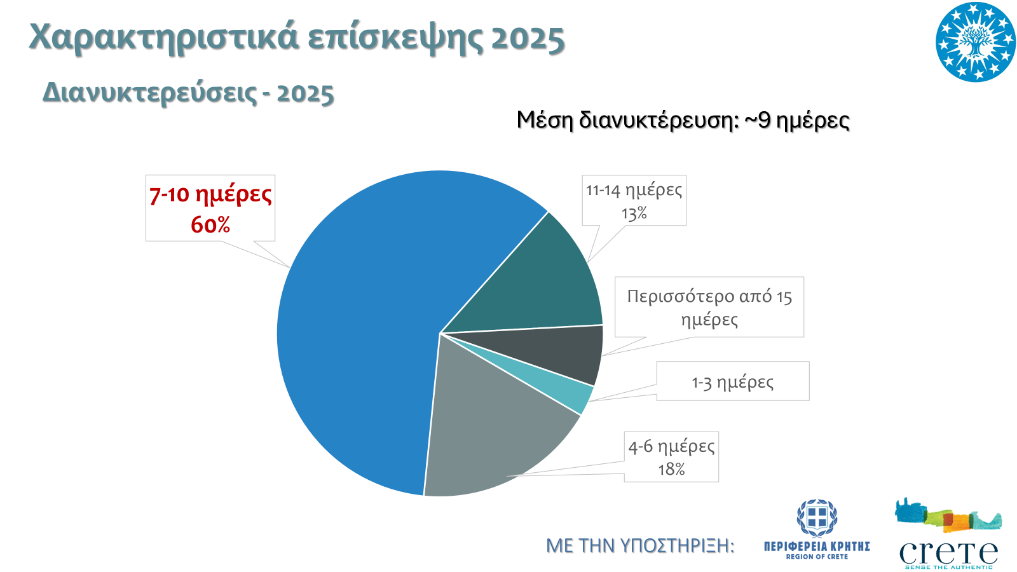

The number of days spent by foreign tourists during their vacations has remained stable compared to the previous year, as foreign tourists stayed an average of nine nights this year as well, with six out of ten taking vacations lasting 7–10 days.

Regarding vacation companions, there has been a 10% increase in those vacationing with their spouse, a percentage offset by those who prefer family vacations with children. One in ten tourists chooses to vacation with friends, a percentage equal to those vacationing with relatives or other family members, while 1.7% choose to vacation alone.

Regarding the type of accommodation and accommodation packages preferred by foreign tourists, half of foreign visitors do not prefer any accommodation package, one in five prefers bed and breakfast, just 17% choose all-inclusive, and 13% choose half-board.

Hotels remain the top choice among tourists, with more than six in ten tourists choosing them, while two in three foreign visitors prefer luxury 4- and 5-star hotels. The percentage of those choosing Airbnb accommodations is 16%, slightly higher than last year, while 13% opt for rental apartments or rooms, and 5% choose to rent a villa.

84% of tourists rated their stay at their accommodation as very good to excellent, 13% as fair, and just 2% rated their stay as poor or bad.

Economic Impact

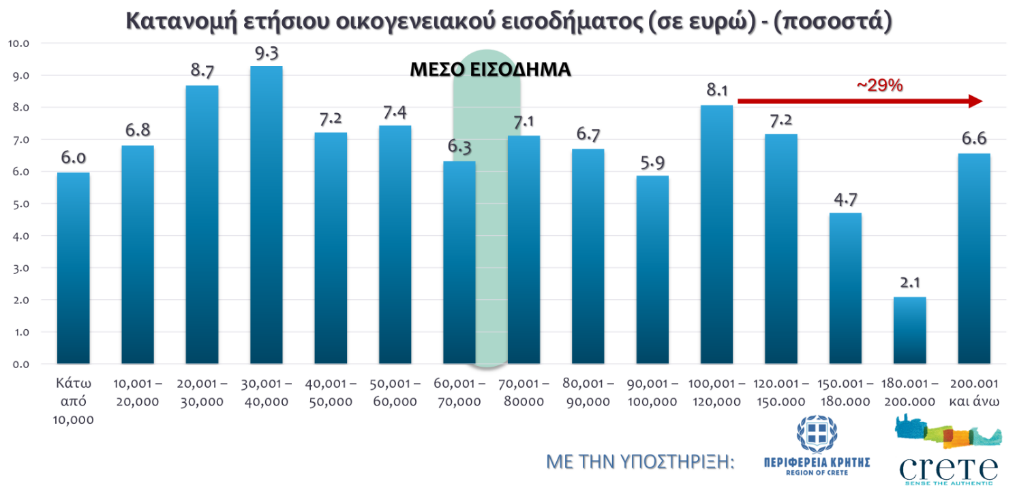

Their average income level remains high at 75,000 euros, while it is worth noting that a fairly high percentage falls into the high-income bracket, with approximately three in ten reporting an annual household income of over 100,000 euros.

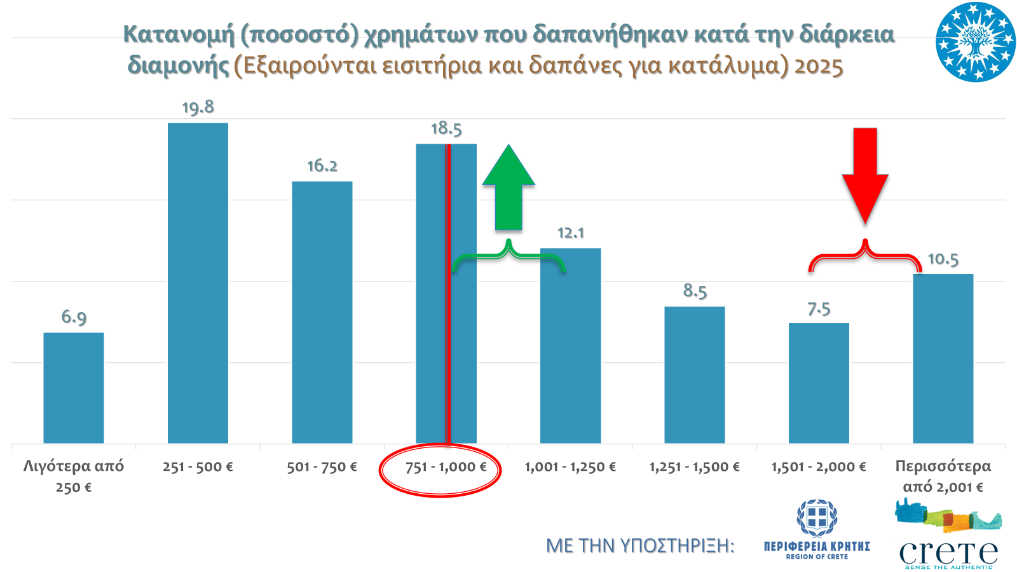

At this point, it should be noted that there has been a slight decrease in the average spending by foreign visitors, excluding ticket and accommodation costs, compared to last year, with the percentage of the highest spending categories decreasing and those between 750 and 1,250 euros increasing.

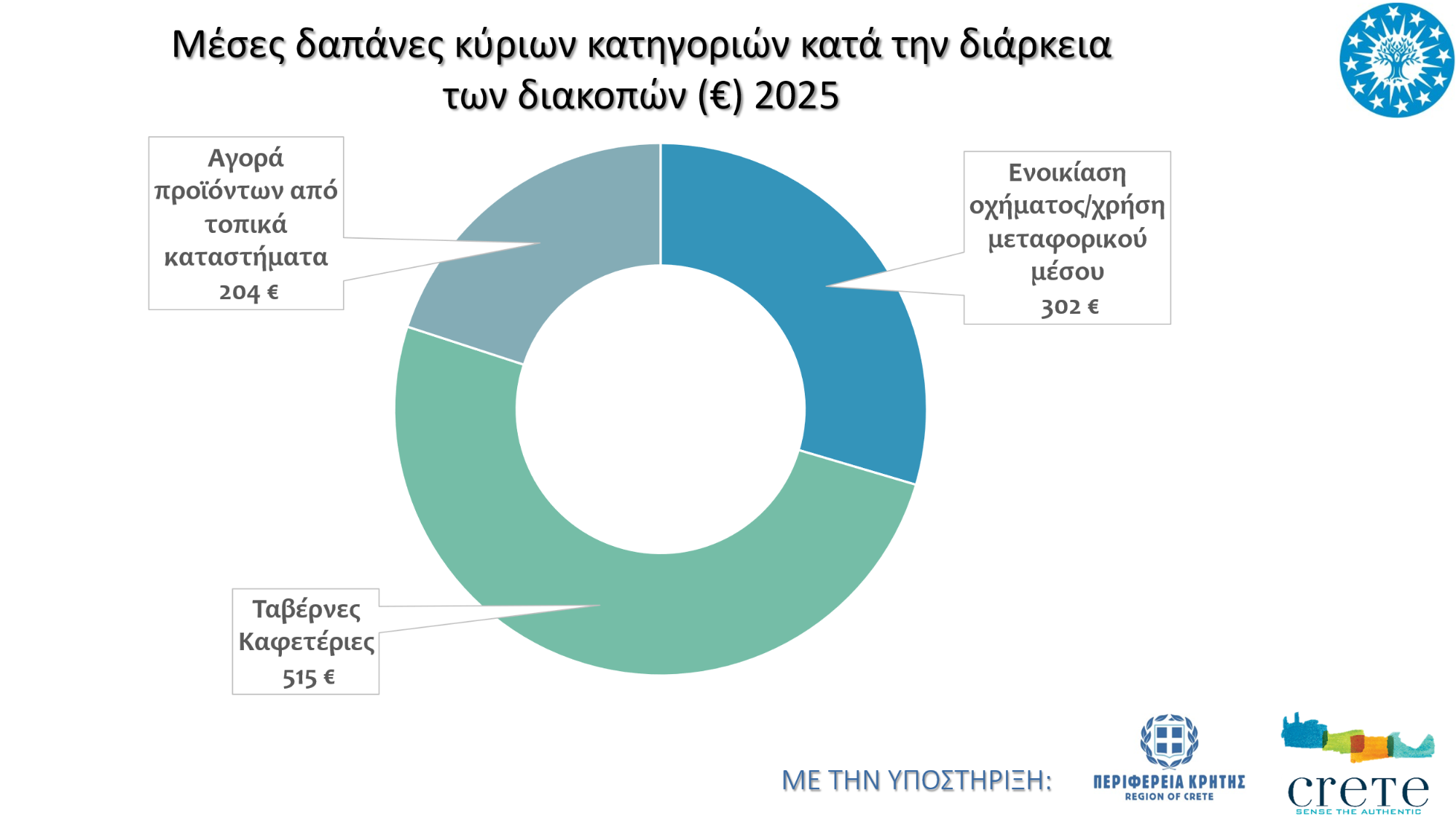

Regarding the categories of spending by all foreign tourists, regardless of origin, they appear to spend the most on dining, followed by transportation, and then on shopping. The amounts fall within the confidence intervals of the previous tourist season, with no sign of an upward trend.

Visitors from the U.S., Canada, and Australia, who, however, saw a significant decrease in spending compared to the previous year; the other country categories also show a slight decrease, with the exception of Scandinavians, who spent more.

Popular Destinations

Regarding the locations chosen by visitors, they continue to prefer the beaches, primarily those of Elafonisi, but also those of Balos and Falassarna. An equally significant number of tourists visit monasteries and churches, hiking trails, museums, and archaeological sites, primarily in Knossos.

Nevertheless, it is worth noting that one in three visitors appears not to be visiting locations far from their accommodation area this year either.

Quality of services and goods

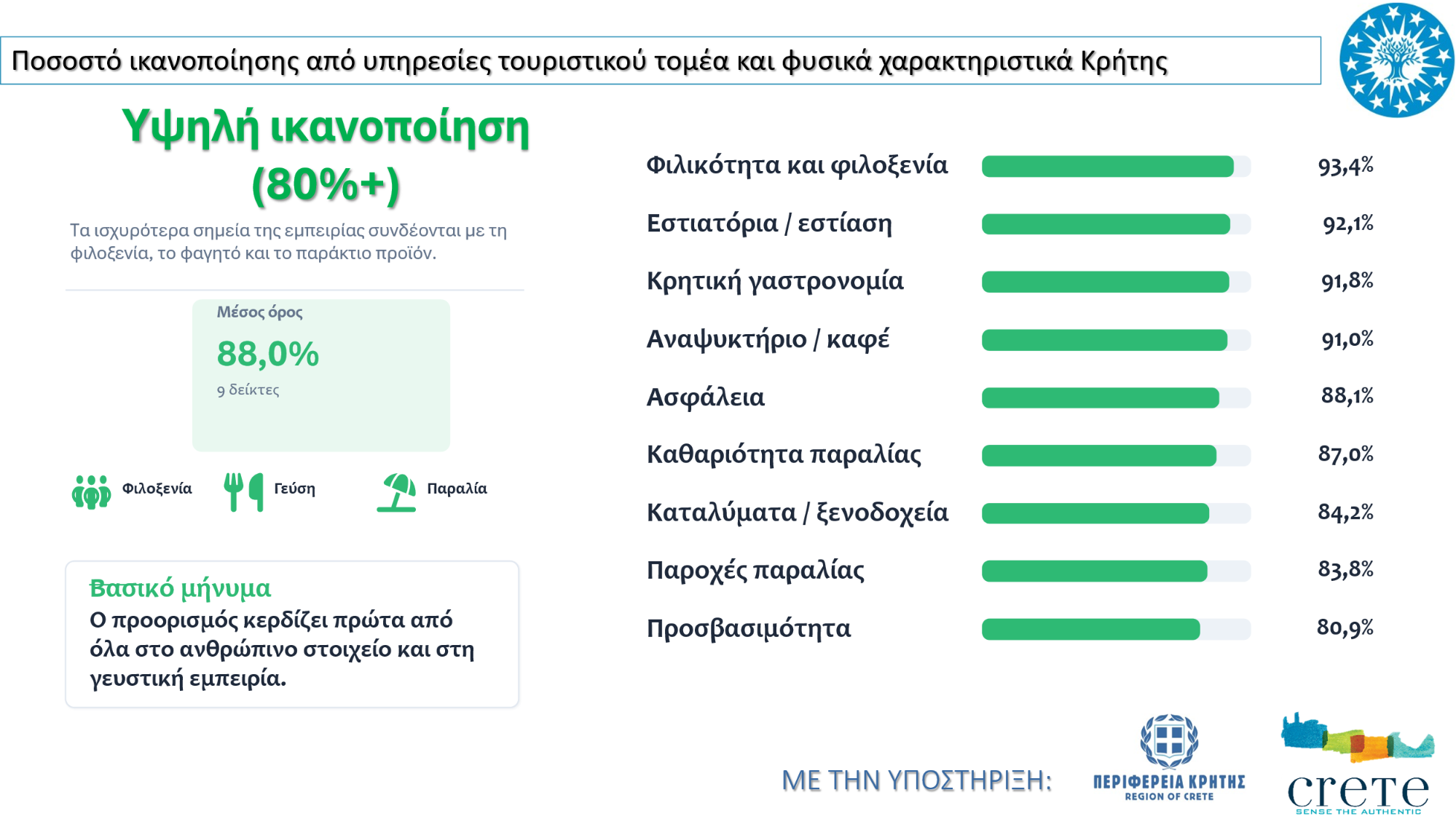

The category average stands at 88%, confirming an overall very high level of satisfaction. Consequently, it can be argued that Crete’s competitive advantage lies primarily in hospitality, culinary identity, and the overall quality of the tourist experience.

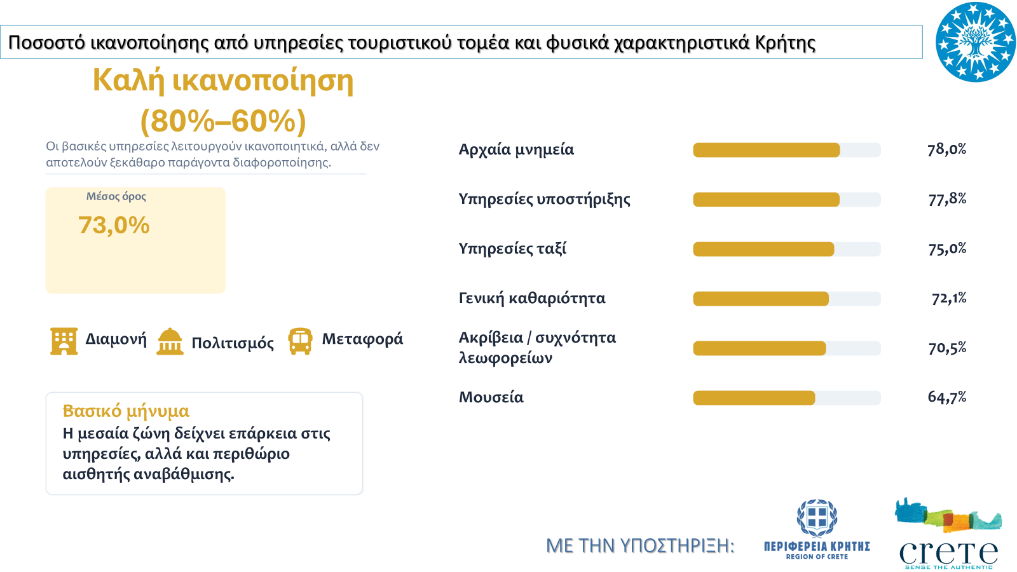

Regarding satisfaction rates among foreign tourists regarding other services offered, 78% were satisfied with ancient monuments and support services, three out of four were satisfied with taxi services, approximately seven in ten reported being satisfied with the overall cleanliness and punctuality of public transportation, while 65% were satisfied with their visit to museums.

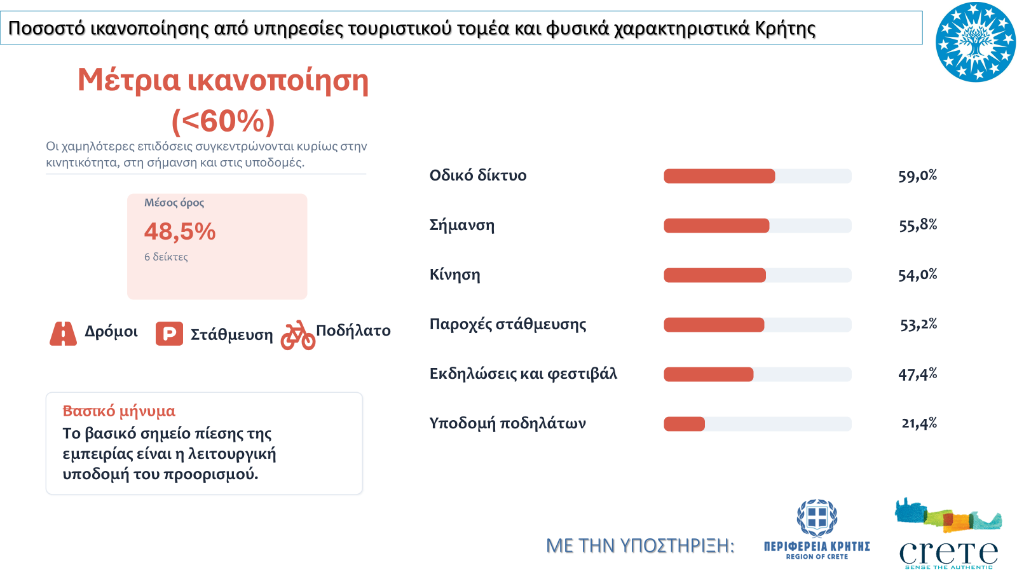

For these specific services, the average satisfaction rate is 73%, indicating that the services are adequate but there is room for improvement to make the destination more competitive.

Foreign tourists continue to express dissatisfaction with the poor condition of the road network and signage. Furthermore, due to the largest influx of tourists the region has ever experienced, there is strong dissatisfaction and concern regarding traffic congestion and the lack of available parking spaces, particularly in Chania City, as well as the inadequate infrastructure for bike lanes, which only 20% of respondents consider sufficient.

Thus, we can conclude that the greatest weakness of Chania as a destination is the inadequacy of its infrastructure and the problems created by the ever-increasing pressure exerted by the growing volume of tourism.

Sustainability

Regarding visitors’ views on the destination’s sustainability, four out of ten tourists have a positive opinion, a percentage similar to last year’s, but there is a slight shift from those who strongly agree to those who simply agree. In contrast, only 14% state that tourism in Crete has not developed in a sustainable manner.

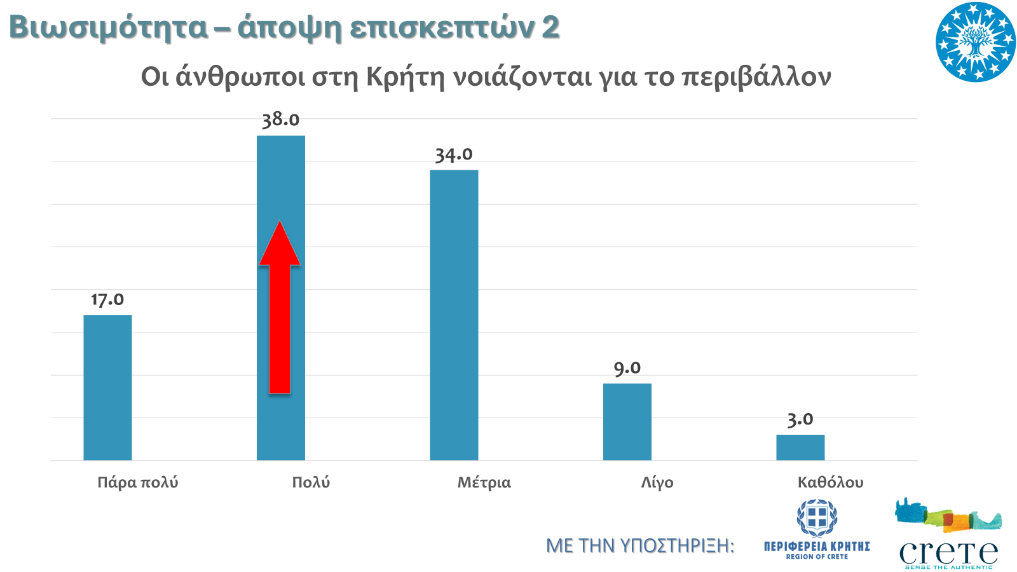

Regarding tourists’ views on whether local people care about the environment, 55% of tourists expressed a positive opinion, a slightly higher percentage than last year, while 12% of visitors made negative comments.

Overall assessment

The Net Promoter Score (NPS) for tourists in Crete for 2025 stands at +46.9, a figure considered particularly high and reflecting an overall very positive destination experience. This index indicates that visitors were not only satisfied with their visit but are also, to a significant degree, willing to recommend Crete to others—a critical factor for the island’s brand image and competitiveness.

More specifically, 51.4% of visitors fall into the positive category. This is the largest group, meaning that more than half of the tourists had such a positive experience that they act as “ambassadors” for the destination.

At the same time, 44.1% fall into the neutral category. This percentage is quite high and indicates that nearly half of the visitors had a good or satisfactory experience, though they did not reach a level of strong enthusiasm. This is a very critical finding: while the overall picture is positive, there is significant room for improvement to shift this large group toward the positive.

In other words, Crete does not face a significant problem of dissatisfaction, but rather the challenge of upgrading the experience from “good” to “excellent.” Negative responses are limited to just 4.5%, a very low percentage.

Furthermore, 51.5% of tourists state that they would visit the region during the winter season if there were direct flights from their city, a fact that highlights the destination’s potential even during the winter season.

Competition

Crete scores highly compared to competing destinations in terms of value for money, as five out of ten tourists state that Crete is the best destination and cannot be compared to any other. Of the remaining tourists, one in three considers Spain, Albania, and Turkey to be destinations with a better service-to-cost ratio, one in four considers Italy, and one in five considers Croatia.

Regarding other destinations, nearly one in ten cites Slovenia, Egypt, and Morocco as competing countries in terms of value for money.

What visitors say

It should be noted that these tourist reports do not carry the same weight as the evaluations they provided in direct questions about Western Crete, which ranked the tourism product at a very high level.

However, they allow us to delve into specific cases that might otherwise be overlooked in the main analysis. In this way, a comprehensive approach to analyzing the tourist experience is achieved.

Overall, it appears that while the basic characteristics of the destination are rated positively by all markets, differences are mainly found in how visitors perceive and evaluate the quality of the experience.

Most negative comments and complaints focus on poor driving behavior, the poor condition of the road network, and heavy traffic. At the same time, the lack of parking spaces, the large volume of trash, the reckless use of plastic, and overcrowding were highlighted.

The phenomenon of tourist congestion remains one of the concerning negative observations for this year as well. The excessive flow of visitors to iconic locations undermines the authentic experience, one of the key reasons why an increasing number of travelers choose Western Crete.

The research and analysis were conducted by the Western Crete Tourism Observatory and coordinated by the Department of Economics & Management of the Mediterranean Agronomic Institute of Chania (MAIC), in collaboration with the Laboratory of Financial Management Systems at the Technical University of Crete, the Department of Management Science & Technology at the Hellenic Mediterranean University (ELMEPA), and members of the Department of Economics at the University of Crete. This research was funded by the Region of Crete. Fraport-Greece and the staff of Chania Airport provide ongoing support to ensure the smooth conduct of the research.

* Konstantinos Zopounidis is an academic, professor, and director of the Laboratory of Financial Management Systems and Data Science at the Technical University of Crete. The authors of the analysis also include Dr. Georgios Baourakis, director of MAICh, Periklis Drakos, a lecturer in the Department of Economics at the University of Crete, and Georgios Angelakis, a researcher in the Department of Economics and Management at MAICh and a Ph.D. candidate in the Department of Management Science & Technology at ELMEPA.