The year 2026 got off to a positive start for hotels in the country’s two largest urban centers, Athens and Thessaloniki, with the capital narrowly edging out the “Bride of Thermaikos.”

Hotel occupancy in Athens during the first quarter of the year rose by 2.4% compared to the same period in 2025, while the corresponding figure for hotels in Thessaloniki was negative. More specifically, hotels in the northern Greek city recorded a 1.1% decline.

The average price per night in the capital’s hotels rose by 2%, while that in the northern Greek city increased further by 3.7%.

These results led to the average revenue per available room in Athens rising by 4.5% year-over-year, with the corresponding change for hotels in Thessaloniki reaching 2.6%. Specifically, RevPAR reached 60 euros.

The picture in Athens

The strongest month for hotels in the Greek capital was January, with occupancy rising 8% year-over-year and the average rate per night approaching a 5% increase.

This improvement is a continuation of the momentum established the previous year, highlighted by the particularly strong performance of hotels during the winter months. Revenue per available room increased by 13.5% in the first quarter of 2025/24. In contrast, during the April–October 2025 period, occupancy declined by 1.2%, although the average rate continued to rise by 2.7%.

This suggests that Athens is making progress in expanding demand during the winter season. However, last March saw significant variations in performance among hotels, with some properties recording a very high increase in demand compared to last year, while others saw a significant decline.

The situation in Thessaloniki

Similarly, for hotels in Thessaloniki, February was the best month. In terms of occupancy, the monthly picture was mixed: February recorded a 3.6% increase year-over-year, while January and March saw declines of 5.2% and 1.7%, respectively.

The lower occupancy rate in January may have been partly influenced by external disruptions, including farmers’ protests and road blockades that hampered domestic and cross-border travel.

As for the average daily fare, it rose in all three months: +1.3% in January, +5.8% in February, and +4.1% in March. In fact, the average price also exceeded the €100 threshold in January and March, indicating that the market maintained its pricing power despite the slight decline in occupancy.

The Outlook for Nafplio

Beyond the country’s two largest urban centers, GBR Consulting also highlights Nafplio, a tourist destination with significant growth potential.

The performance of the hotel sector in this Peloponnese city is based primarily on pricing dynamics rather than strong growth in demand. The latest available data indicate that the market is managing to maintain pricing power, even in an environment of moderate occupancy.

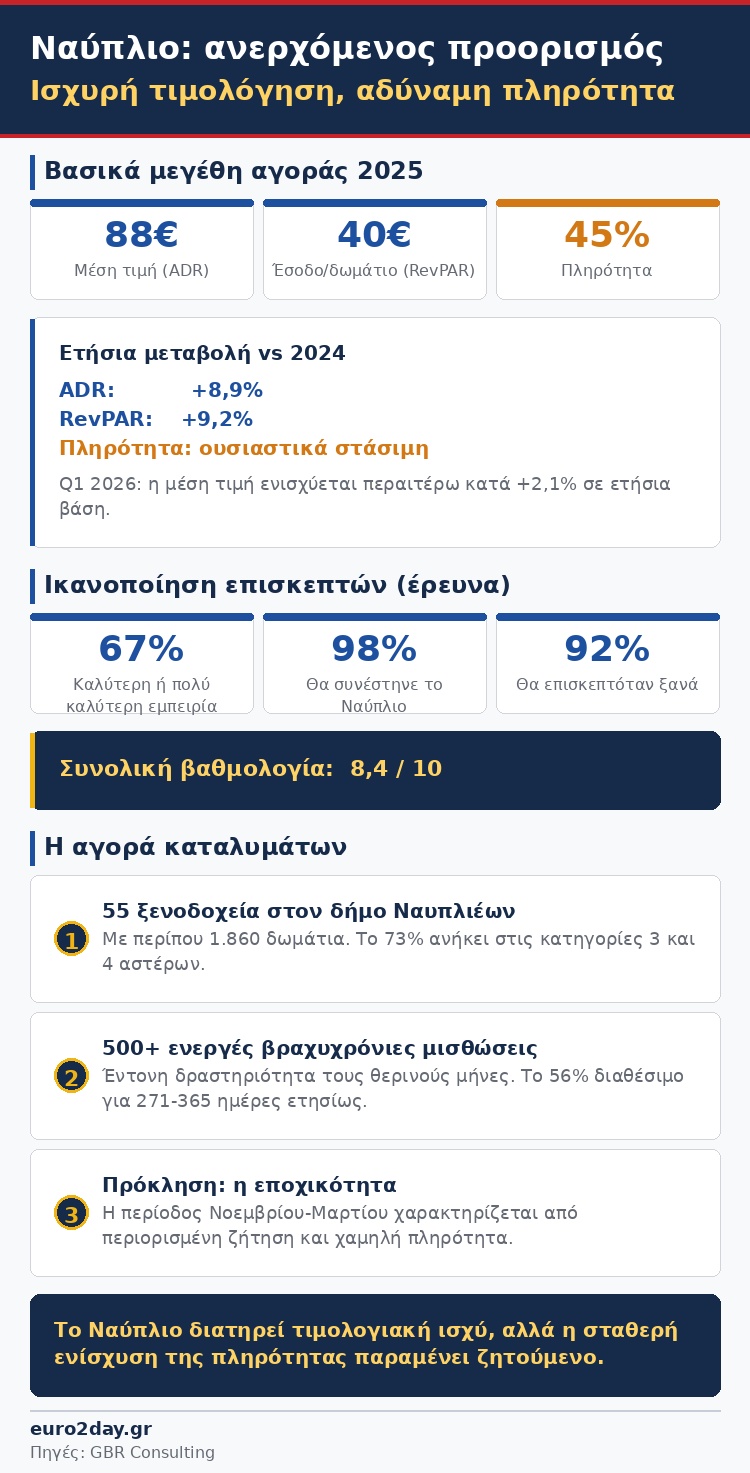

Specifically, in 2025 , the average daily rate (ADR) stood at 88 euros, marking an 8.9% increase compared to 2024. This rise also led to an improvement in RevPAR, which reached €40 (+9.2%), despite the fact that occupancy remained essentially flat at 45%.

This trend continued into 2026. During the first quarter, the average daily rate recorded a further increase of 2.1% year-over-year, confirming hotels’ ability to maintain higher rates. However, occupancy remains relatively low, particularly outside the peak season. Although there was an improvement in January and February (from a low base), March saw a decline once again.

The main challenge for Nafplio is the seasonality of demand. The winter season, from November to March, is characterized by limited demand, which prevents a steady increase in occupancy rates. At the same time, the high volume of short-term rentals creates additional competition, particularly during the summer months.

In the survey, 67% stated that their experience was better or much better than expected, 98% would recommend Nafplio to others, and 92% would visit again. The overall rating reached 8.4 out of 10.

It should be noted that the municipality of Nafplio has 55 hotels, 73% of which are in the 3- and 4-star categories, offering approximately 1,860 rooms. At the same time, the short-term rental market is particularly active during the summer season, with more than 500 active listings, while 56% of the listings are available for 271–365 days a year.