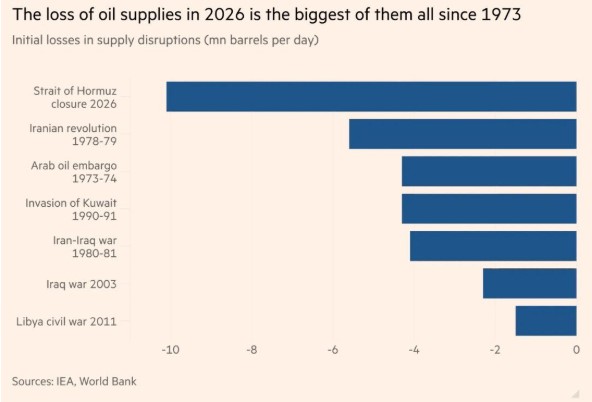

According to the World Bank and the IEA, no other energy crisis has has led to such a large loss of barrels of oil from the market as the closure of the Strait of Hormuz this year. This is evident in the FT chart we present below.

As time goes on and free navigation is not restored in the Strait of Hormuz, conditions in the market for oil and refined products are becoming more difficult, and this has an impact on inflation.

Even greater is the share of sulfuric acid transported through the Strait of Hormuz, which accounts for 50% of global volume. Vitriole, as we call it, is used in fertilizers, in refineries for the purification of petroleum products, in the production of chemicals, plastics, etc. Also, 28% of the world’s liquefied natural gas is transported via the same maritime route.

They say that three clocks are ticking right now. Iran’s clock, counting down to the gradual closure of some of its oil wells; Trump’s political clock for the U.S. midterm elections; and the economic clock for everyone else.

The price of U.S. crude stood at $105 per barrel last night, and the price of Brent at $114. However, we may not have seen the peak yet if the passage of ships is not permitted.

According to JP Morgan’s latest report , OECD commercial oil inventories are trending toward record lows between May 9 and May 30. At that point, if we reach it, price increases will become “exponential rather than linear.”

The problem is that even if commercial ships are allowed to pass through the Strait of Hormuz, it is likely that many of the first shipments will be used to replenish strategic and other reserves that have been depleted over the past two months. This means that relief at the consumer level will be less than many might expect in the first few months, if we are to believe the experts.

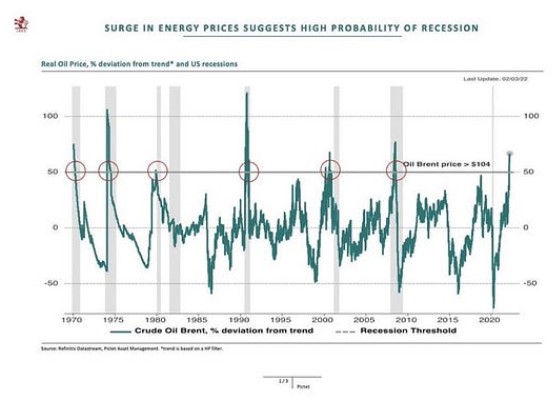

Historically, the consequences for economic activity can be dramatic. This is because history reveals a worrying pattern.When oil price deviations from the trend reach 50% or more, the economy enters a recession. This has happened in 6 out of the last 6 instances.

A glance at the chart below will confirm this. We are now at that level. Will history repeat itself or not? Of course, some things have changed compared to the past.

One of them is the massive liquidity injected by central banks after the 2008 crisis, which they continued to do until relatively recently. A significant portion of this liquidity is still in the market. But is it enough? We’ll know the answer in about a year from now.