ExxonMobil’s decision is reshuffling the deck in the Greek hydrocarbons game - Helleniq Energy to return the “West of Crete” block to the State, which will likely be put up for tender again, perhaps along with other blocks that had not attracted interest in the past.

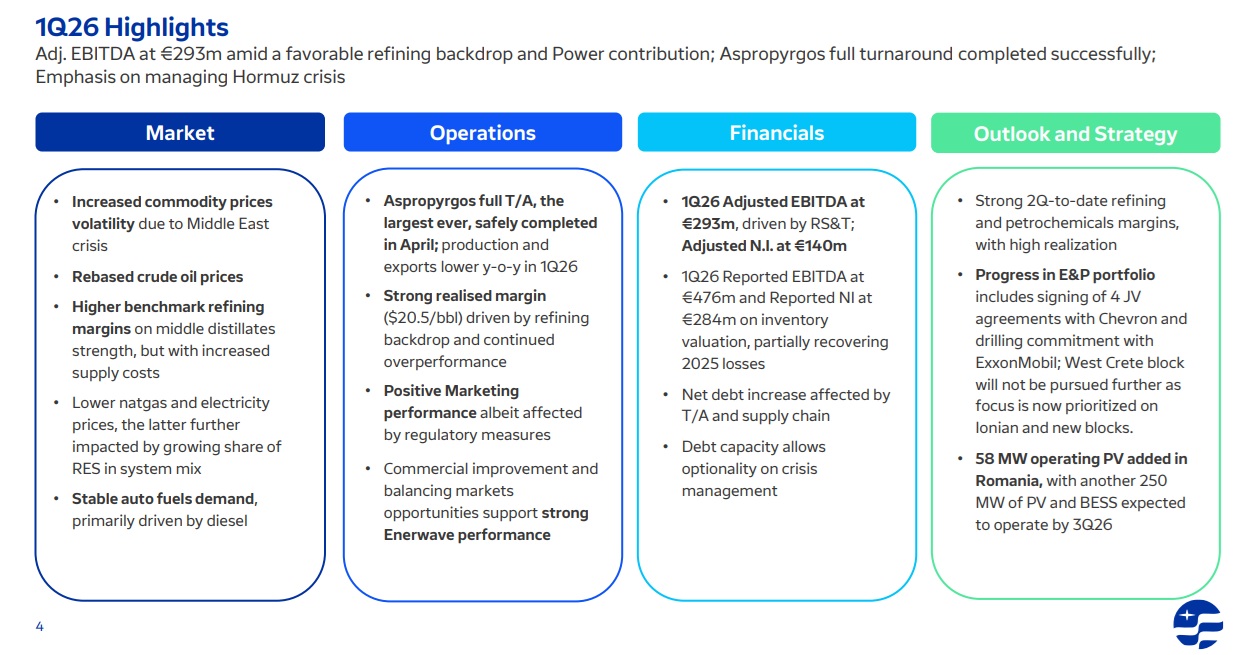

“The West Crete block will not be pursued further (i.e., developed), as the focus is now on the Ionian Sea and new blocks,” Helleniq Energy revealed during a recent presentation of results to analysts, officially announcing the decision to return the block to the Hellenic Hydrocarbon and Energy Resources Management Company (EDEYEP).

This development had been expected for some time, as ExxonMobil never conducted high-resolution 3D seismic surveys in this specific block, part of which is located in deep water, is technically complex, and less promising compared to its neighbor, the“Southwest of Crete” block, which has also been awarded to the consortium.

In practice, this means that following the expiration of the second consecutive extension (which ended on April 6, 2026) granted to the consortium for the first phase of exploration, this specific block will revert to EDEYEP.

This, in turn, opens the way for the latter to redraw the block and, after first announcing a tender for new seismic surveys, to re-launch it on its own or, most likely, together with other blocks that had not attracted interest in the past. The redrawing scenario is linked to the fact that part of it may be of particular interest, and because it involves deep waters, any interest will likely come from a major player.

“Soon, EDEYEP will announce a tender for new seismic surveys in offshore areas,” said EDEYEP head Aris Stefatos a few days ago from the podium of the 62nd Continental Europe Energy Council (CEEC) held in Athens.

The category of blocks under discussion for re-entry into the market may include plots from earlier concession rounds, dating back to the 2010s, none of which ever proceeded—each for its own reasons—ranging from“NW Peloponnese” and“Patraikos,”to“Western Crete.”

“We’ve captured the market’s attention, and now there are areas we want to revisit—something we’re already doing and are in the process of evaluating. In Cairo (Egypes 2026), we met with specialized companies involved in area development to potentially make them more attractive,” Mr. Stefatos had also said a month ago at the 7th Power & Gas Forum.

In reality, the areas referred to by the company’s CEO are the so-called “relinquished areas” (as they are termed in industry jargon), which include the onshore“Aetolia-Acarnania,”“Arta-Preveza,” and“Ioannina.”

The concessionaires (e.g., Repsol, Helleniq Energy, Energean) returned them to the State, either because they did not identify viable reserves or because they were unable to complete their exploration work due to bureaucracy, local opposition, and other obstacles.

The goal is to bring mid-cap companies into the mix, since while the above may not be “world-class targets”—as deposits capable of yielding large quantities are called—they are estimated to be economically viable as well.

Scenarios for a new open door

In summary, there is a series of plots for which the state, provided it sees potential, could announce a new “open door,” as it is called. That is, an open call for expressions of interest, meaning that the area is available on a permanent basis. The same applies when the previous licensing process concerning the area in question has proven fruitless.

At the same time, and because for some time now “everyone is talking to everyone,” as an industry insider puts it, it is not out of the question that we will see new farm-in deals , such as the one ExxonMobil made by entering “Block 2” and purchasing stakes from the existing licensees.

It has been suggested that “Block 10” in the Gulf of Kyparissia could be one such case, where it has long been rumored that the concessionaire Helleniq Upstream has begun discussions with Chevron.