For the first time since China’s rise in the early 2000s, a technology is not merely transforming companies or industries; it is reshaping the very structure of the global economy.

Artificial Intelligence has moved beyond the realm of innovation and is rapidly transforming into a new form of economic power—a force that requires enormous amounts of energy, industrial equipment, semiconductors, and funding.

The result is a profound and structural shift in liquidity. AI is absorbing capital at a rate that affects bond yields, strengthens the dollar, shifts the balance between the U.S. and Europe, and revalues the entire investment universe. This is not just another tech hype cycle. It is a new economic reality that is already shaping the investment environment of the coming decade.

1. Investments in AI are causing global macroeconomic awe

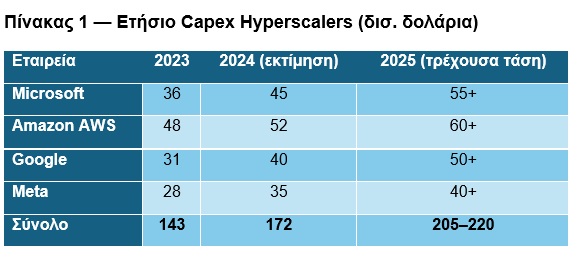

American hyperscalers (as major investors in artificial intelligence are called)—Microsoft, Amazon, Google, and Meta—have entered an unprecedented race to acquire computing power.

Their total capital expenditures on data centers, GPUs, energy infrastructure, and network systems now run at an annual rate approaching $250–300 billion. The scale of this investment is not merely impressive; it is macroeconomically decisive.

The financing for this wave comes primarily from internal cash flows, debt issuance, and private credit, creating ever-increasing demand for dollar liquidity. The result is increased pressure on U.S. bond yields and a parallel strengthening of the dollar as the global financial hub.

AI now functions as a mechanism for absorbing global liquidity, shifting capital from traditional sectors toward artificial intelligence infrastructure and creating a new investment landscape.

The concentration of such a large volume of capital in a single sector is creating a historic shift: markets are no longer driven exclusively by the economic cycle, but increasingly by the needs of AI infrastructure.

2. The Energy Reality — Data Centers Are the New Industrial Giants

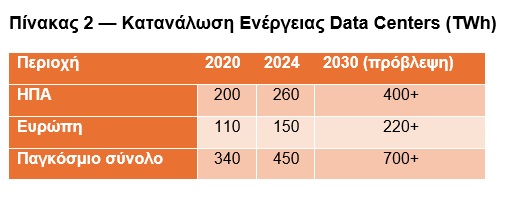

Data centers are rapidly becoming one of the world’s largest consumers of electricity. The energy consumption of AI clusters is growing at rates exceeding 25% annually, while in regions such as Virginia and Texas, demand from data centers is already the primary driver of growth in total energy consumption.

Europe is in an even more difficult position. Ireland is restricting new facilities due to a lack of power, the Netherlands is freezing permits, and Germany is facing serious delays in high-voltage transmission projects. AI is not just a digital revolution; it is an energy revolution.

This energy pressure is already affecting LNG markets, nuclear investments, demand for transformers and substations, as well as the entire electricity infrastructure chain. AI now resembles heavy industry more than the software economy.

3. Semiconductors — The New Strategic Commodity of Our Time

Advanced processors and high-bandwidth memory have evolved into the most important strategic commodity of the new economy. TSMC controls nearly all advanced chip production, while NVIDIA has gained pricing power that resembles an energy cartel more than a conventional technology company.

Demand for HBM memory is growing at rates exceeding 200% annually, creating persistent supply bottlenecks. The geopolitical dimension is equally critical: Taiwan has become one of the most important strategic hubs of the global economy. The world’s dependence on such a limited number of producers creates a new form of systemic risk—a risk that markets may still be underestimating.

4. Infrastructure: The Big Winner

The true value of AI isn’t created solely in software. It’s created in infrastructure. The major beneficiaries of the new cycle are energy companies, transformer manufacturers, high-voltage cable producers, cooling companies, industrial manufacturers, and private credit markets financing the data center boom.

Industrial real estate assets are already seeing historically high demand, while delivery times for critical equipment have skyrocketed.

Delivery times have more than doubled, revealing a market that is already overheating. AI is not just a technological transition. It is the creation of a new global industrial value chain.

5. The Great Investment Transition

The dominant investment narrative of the next decade may not be AI applications themselves, but the physical infrastructure required for them to function. The market is gradually shifting toward energy sufficiency, power grids, industrial production, semiconductors, and strategic supply chains.

In other words, AI does not merely lead to technological development; it leads to reindustrialization. And like every major industrial transition in history, this one requires massive capital, long-term investments, geopolitical stability, and energy security.

Conclusion

Artificial Intelligence is not a temporary stock market bubble. It is the new infrastructure of the global economy. It is reshaping capital flows, energy demand, semiconductor production, the geopolitical balance, and the structure of the markets themselves.

AI acts as a magnet for liquidity, drawing capital away from the rest of the economy and creating a new investment cycle that resembles an industrial revolution more than traditional technological innovation.

For investors, understanding this transition is critical. AI is not a consumer product. It is infrastructure. And infrastructure has longevity, depth, and macroeconomic influence.

Markets are just beginning to price in this new reality —and those who recognize it early may gain a significant strategic advantage.

Sources: Annual Reports: Microsoft, Amazon, Alphabet, Meta (2023–2024), International Energy Agency (IEA), Data Centre Energy Outlook 2024, U.S. Energy Information Administration (EIA), Electricity Consumption Data 2024, ASML & TSMC Investor Presentations (2024), McKinsey Global Institute, AI Infrastructure Report 2024, Goldman Sachs Global Investment Research, AI Capex Cycle 2024

* Nicholas Havoutis has many years of experience leading strategic financial units, having served as an executive at JPMorgan (New York), Chase Manhattan Bank (London), and Eurobank (Athens). At the same time, he has a significant presence in the SME sector. Today, as head of SoZone Limited, he advises companies and investors on international expansion, organic optimization, and M&A strategies.