The decision by the ExxonMobil–Helleniq Energy consortium to return the “West of Crete” offshore block to the Greek government— first reported by euro2day.gr—sets the stage for a new round of concessions in Greek waters.

This is because the consortium’s decision must be “read” in conjunction with yesterday’s statement by the Ministry of Environment and Energy that “EDEPE (note: the Hellenic Hydrocarbon and Energy Resources Management Company) will assess the feasibility of conducting 3D seismic surveys that will allow interested investors to continue exploration west of Crete.”

Other developments also point to the conclusion that a new round of concessions is being considered, with market executives recalling a recent statement by the head of EDEYEP, Aris Stefatos, at the 62nd Continental Europe Energy Council (CEEC) that “a tender for new seismic surveys in offshore areas will be announced soon.”

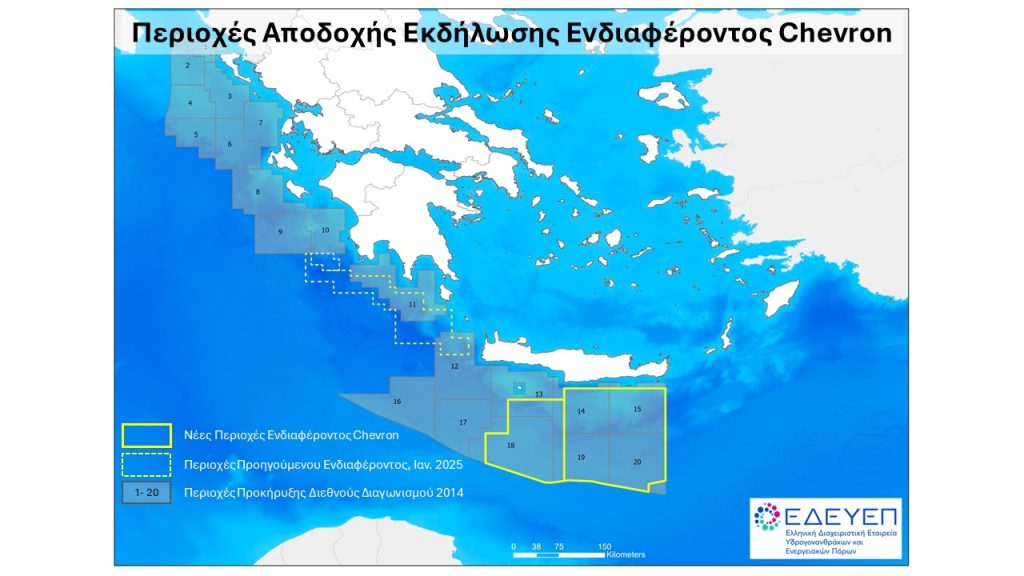

Although officials are keeping their cards close to their chest, sources in the hydrocarbon market point out that if one looks at the map showing the nine active Greek blocks, there is still a vast offshore area, stretching from the northern Ionian Sea to the southern Peloponnese— that is, up to the point where Chevron’s latest concessions begin—where new small or larger blocks could be delineated.

This includes both older blocks that have been returned to the state from time to time, such as the “West of Crete,” as well as new ones, which can be formed from the sections a company is required to relinquish when it moves on to the next exploration phase, as in the case of “Block 2” in the NW Ionian Sea.

In most concession contracts, the rule is that as exploration progresses and moves from initial seismic surveys to the drilling phase, the area shrinks and the company retains only the “prime areas” where it has identified potential targets, releasing the rest and returning them to the State.

Depending on the contract and the law, the mandatory relinquishment of areas varies, but it is usually equal to 20% of the initial area, which the government can combine with neighboring areas to create new blocks.

In summary, as our interlocutors say, there are several such large-scale areas where either the 2D seismic data is sparse (2D) and need to be densified, or new 3D surveys are needed because the mapping dates back to the 2010s and must be repeated using the latest technology, or no 3D surveys have been conducted at all, as in the “West of Crete” block.

In the case of this specific block, the committee determined, as stated in yesterday’s announcement by the Ministry of Environment and Energy, that "entering the next phase would require a very significant expenditure for the execution of three-dimensional (3D) seismic surveys before the consortium is in a position to make a decision on drilling."

This is a vast area of 20,000 square kilometers, part of which lies in very deep waters and is technically complex, with the American company apparently considering it less promising compared to the neighboring “Southwest of Crete,” which has also been awarded to the consortium.

However, according to market sources, a very large portion of it—just under 10,000 square kilometers — may be of interest, hence yesterday’s report from the Ministry of Environment and Energy that any new 3D surveys may allow interested parties to continue exploration.

Facing a new round of mapping

Taking all of the above into account, everything indicates that we are likely facing a new round of mapping in Greek waters, in order to map in detail anything that might be of interest so that it can subsequently be put out to tender, with the aim of attracting mid-cap companies, in addition to the two American giants.

The rationale is that a model similar to the one used in 2012 could be applied, based on the logic that even smaller targets may be of economic interest. At that time, the Greek Ministry of Environment and Energy had commissioned the Norwegian company PGS (now TGS) to conduct multiclient seismic surveys—as those carried out at the company’s own expense are called—which then sells the data to interested parties to participate in the tenders.

In 2012, the Norwegians had “surveyed” a total of 12,500 km, data which was reprocessed in 2018 using modern depth imaging methods (KPSDM), covering a large portion of the Greek seas.

In practice, something similar appears to be feasible now, a scenario facilitated by the fact that interested parties have been found to purchase the data.

Scenarios for a new open door

In summary, there is a series of plots for which the state, provided it sees potential, could announce a new “open door,” as it is called—that is, an open call for expressions of interest, meaning the area is available on a permanent basis.

At the same time, and because for some time now “everyone is talking to everyone,” as an industry insider puts it, it is not out of the question that we might see new “farm-in” deals, such as the one ExxonMobil made when it entered “Block 2” and purchased stakes from existing leaseholders.

It has been suggested that “Block 10” in the Gulf of Kyparissia could be such a case, where it has long been rumored that the concessionaire Helleniq Upstream is in talks with Chevron.