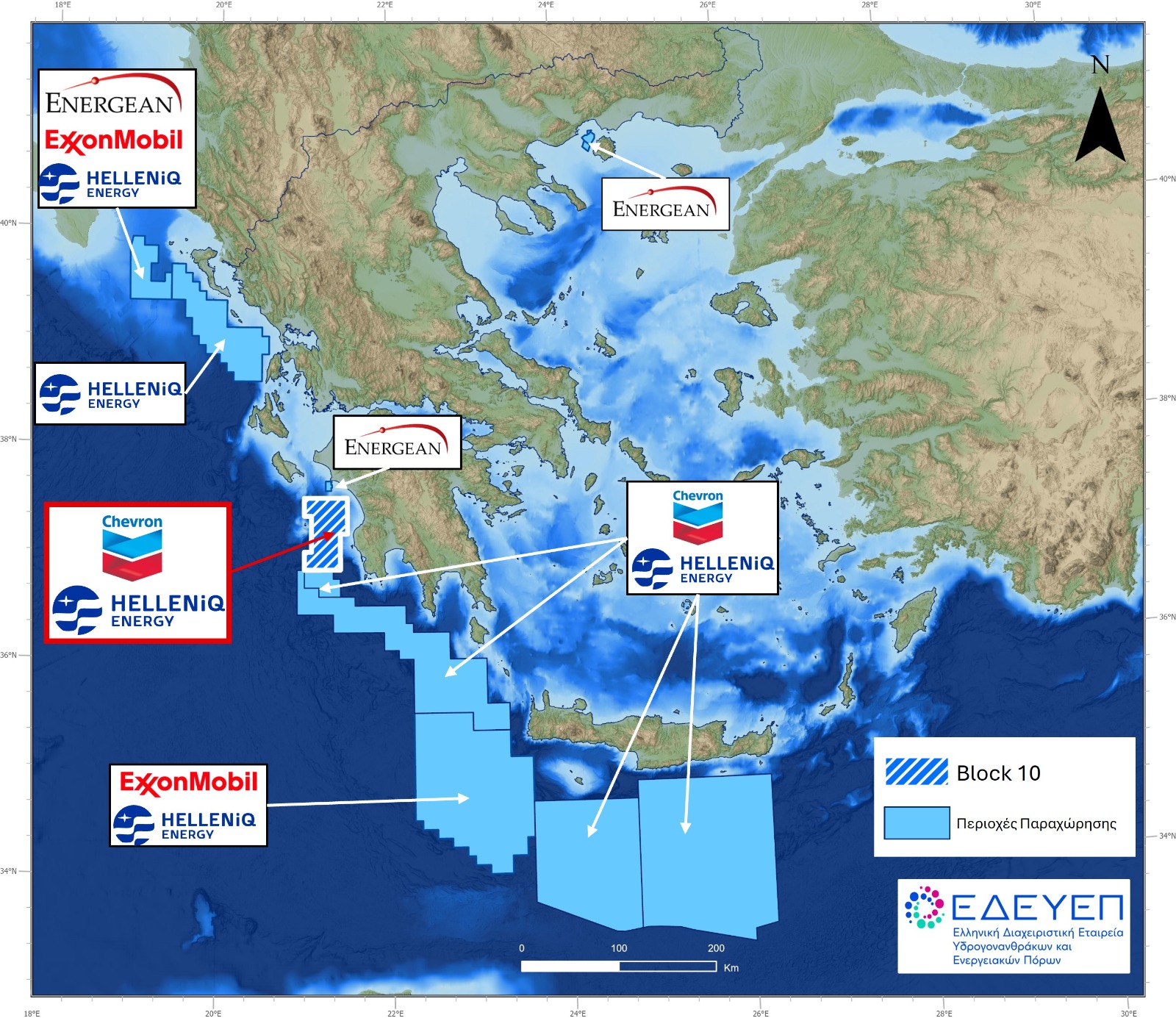

The impression that the coming years will see a flurry of drilling in Greek waters is reinforced by the fact that seven of the nine active Greek blocks are now led by Chevron and Exxon Mobil, not to mention the real possibility of new blocks being delineated.

Looking at the big picture on the map, one sees a vast contiguous geographical arc of concessions granted to the two American giants, stretching from the western Peloponnese to the southern tip of Crete, covering a total area of 64,559 square kilometers—roughly half the country’s land area.

Of this area under exploration, the overwhelming majority— comprising 5 blocks totaling 49,000 square kilometers— is operated by Chevron, leaving ExxonMobil far behind in second place with only two blocks (following the return of the Western Crete block to the State) and approximately 17,500 square kilometers.

As for the key question—why Chevron acquired 70% of Hellenic Energy’s stake in “Block 10” of the Gulf of Kyparissia, a deal the two sides had been negotiating for some time— the answer is that this statistically increases the chances of locating exploitable targets in the area south of the Peloponnese.

Adding up, as shown on the map, the 2,376 sq. km of “Block 10” with the two other blocks where it is already the operator, “A2” (826 sq. km) and “Southern Peloponnese” (10,211 sq. km), a single exploration area is created—a continuous, elongated field—which offers the company great flexibility in selecting drilling targets.

Mathematically, the odds of a successful drilling increase. Hence the request from the new consortium for an 18-month extension of the second exploration phase. This is so that the data retrieved from the vessel’s surveys (note: beginning in October) in the neighboring concession areas (“A2” and “South Peloponnese”) can be evaluated together with the existing 2D and 3D seismic data for “Block 10” collected by Helleniq Energy in previous years, and decisions can be made regarding the broader region.

Scenarios for an oil structure in “Block 10”

On second thought, Chevron’s move to enter “Block 10” may also be linked to its geological structure. The plot is adjacent to the offshore deposit at Katakolo, Elis, which is estimated to have potential reserves of 14 million barrels of oil at a shallow depth of 300 meters, but all indications are that it will not be developed. The area has now been included, as of 2025, in the strict protection zone of the new Ionian National Marine Park, with all that this entails.

However, the issue of “Block 10” being adjacent to the aforementioned oil deposit is also highlighted on the website of the Hellenic Hydrocarbon and Energy Resources Management Company (EDEYEP).

“The proven oil system in the neighboring licensed area of Western Katakolo, combined with the large number of surface natural oil and gas seeps in the wider region, make ‘Block 10’ a particularly interesting area. Furthermore, several oil and natural gas fields have been discovered in Albania, which belong to the same fold and thrust zone and share the same geological characteristics,” it is noted.

When asked, therefore, whether the new block Chevron is entering might also have an oil structure, experts do not rule it out at all. “It depends on the stratigraphic level and the target. The chances of finding natural gas increase as we move south,” they note, referring to the southern Peloponnese and, of course, Crete.

When will we see drilling?

Another question concerns when we will see drilling. If the new plan is approved immediately, then factoring in the 18-month extension requested by the consortium, we are looking at around December 2027 for the decision on the first drilling, with an estimated cost of $100 million. The drilling is expected to take place sometime in the second quarter of 2028.

The best answer to the question of when we will see the first drilling operations in Greek waters is provided by the outlook of the national program for the next 10 years (Exploration Program: 10-Year Outlook) by EDEYEP itself, which, based on yesterday’s developments, indicates that:

- In “Block 2” in the northwestern Ionian Sea (Energean, ExxonMobil, Helleniq Energy), the first drilling is expected in February 2027. This will provide the first answer in decades to what lies beneath the Greek seas.

- In the “Ionian Block” (Helleniq Energy), the first quarter of 2028. Note that, along with Katakolo, these are the only blocks where the concessionaire still holds a 100% stake.

- In “Block 10” of the Gulf of Kyparissia (Chevron, Helleniq Energy), in the second quarter of 2028.

- In “SW Crete” (ExxonMobil, Helleniq Energy) in the third quarter of 2028.

- In “A2” (Chevron-Helleniq Energy) in the second and third quarters of 2031.

- In “Southern Peloponnese” (Chevron-Helleniq Energy) in the fourth quarter of 2031.

- In “South Crete 1” (Chevron-Helleniq Energy) in the second or third quarter of 2032.

- In “South Crete 2” (Chevron-Helleniq Energy) in the fourth quarter of 2032

Of course, the above are merely forecasts, as the term “outlook” implies. The outcome will be determined in the field, based on exploration findings, the type of hydrocarbons, the characteristics of the basin, the depths, and the distance from the mainland.

If the above drillings lead to exploitable reserves, then sometime between 2032 and 2035, we will see the first production of hydrocarbons in Greece, as estimated months ago by the head of EDEYEP, Aris Stefatos.

At the same time, we must not forget that the recent decision by the ExxonMobil–Helleniq Energy consortium to return the “West of Crete” offshore block to the State creates the conditions for a new round of concessions in Greek waters.

This is because the consortium’s decision must be interpreted in conjunction with the Ministry of Environment and Energy’s statement that “EDEP will assess the possibilities for conducting 3D seismic surveys that will allow interested investors to continue exploration west of Crete.”

The possibility of delineating new blocks in the arc stretching from the northern Ionian Sea to the southern Peloponnese is real, and there are various areas that either have sparse two-dimensional (2D) seismic data that needs to be densified, or require new 3D surveys.