Consumers continue to spend, but they are relying more on credit and less on their savings. At least in the U.S. Major tech companies are competing with one another to see who will spend the most on AI, while the rest are stockpiling products just in case, as they worry about potential disruptions in the supply chain and rising costs.When households and businesses spend, economies typically grow. The same is true today. However, there is a risk that this economic boost could turn into a problem if, for example, consumers do not buy the products that companies are stockpiling.

For now, the market is brushing all this aside and focusing on the truce between the U.S. and Iran—which has led to a drop in oil prices—and the AI narrative about the major, positive impacts on productivity.

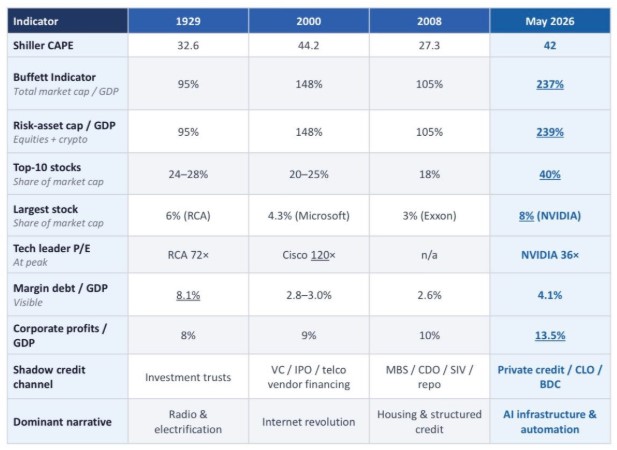

At the same time, others are concerned because they compare the characteristics of today’s stock market with those of past markets that were labeled as bubbles and find not only similarities but also instances where current conditions exceed those of the past. One of them is Emmanuel Ferry, who created the table below.

As you can see, Mr. Ferri compares various indicators of the U.S. stock market in May 2026 with those from 1929, 2000, and 2008. That is, the moments in history that have gone down as market bubbles.

The valuation of the current market based on the price-to-earnings ratio (Shiller CAPE) is the second highest after that of the dot-com bubble in 2000. Furthermore, the Buffett ratio— that is, market capitalization relative to GDP—stands at 232% and has never been higher.

Moreover, the degree of market concentration, as measured by the market capitalization of the 10 largest companies relative to the total, stands at 40% compared to 24%-28% in 1929 and 20%-25% in 2000. Traditional leverage (borrowing for stock purchases relative to GDP) stands at 4.1% and is nearly half of what it was in 1929 (8.1%). However, today the risk has shifted to the shadow financial sector, such as private credit, CLOs, etc.

AI supports the rally but also poses a significant risk. This is because, while today’s companies have cash flows and profits unlike their dot-com counterparts, the scale of investment is so vast that it creates the risk of excess capacity and falling returns in the future.

If 1929 was the leverage bubble, 2000 was the valuation bubble, and 2008 was the credit bubble, 2026 looks likethe bubble of concentration in a few companies, according to him.

However, his entire line of reasoning is based on the assumption that the underlying conditions measured by the above indicators have changed, so the comparison is unfounded and therefore the conclusion about a bubble may not hold up. In other words, high concentration is not the problem but a hallmark of the new situation.

Could things be different this time?