As part of a targeted monthly survey conducted by the Institute for Retail and Consumer Goods Research (IELKA), focusing exclusively on large supermarket chains regarding inflationary trends in the organized food retail sector, price trends in May 2026 were examined in comparison to May 2025.

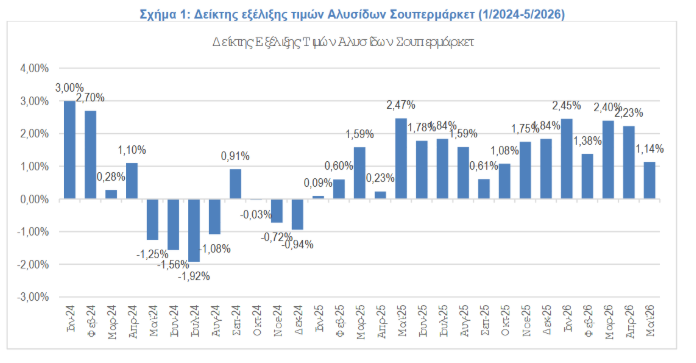

The survey found that inflation in supermarket chains stood at 1.14% in May 2026 compared to May 2025.

The price index for May 2026 compared to the previous month, April 2026, increased by 0.29%, while the rolling 12-month (May 2025 – April 2026) shows an increase of 1.79%.

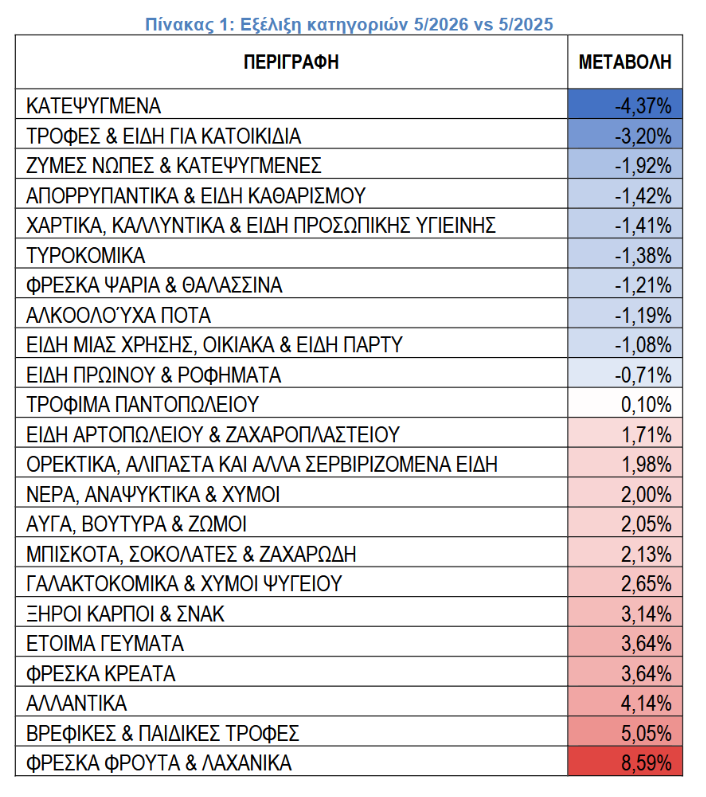

It should be noted that half of the inflationary pressure is attributable to the fresh fruits and vegetables category, which has been affected by adverse weather conditions and seasonality over the past two months. The remaining categories show comparatively very small fluctuations.

Of the 23 categories examined, 10 show an increase and 13 a decrease.

The largest price decreases in May 2026 compared to May 2025 are recorded in the following categories:

- Frozen foods: -4.37%

- Pet food and supplies: -3.20%

- Fresh and frozen baked goods: -1.92%

- Detergents and cleaning supplies: -1.42%

- Paper products, cosmetics, and personal hygiene items: -1.41%

The recorded decreases are the result of both market normalization and a reduction in producer prices for certain products.

The largest increases in May 2026 compared to May 2025 are recorded in the following categories:

- Fresh fruits and vegetables: +8.59%

- Baby and children's food: +5.05%

- Deli meats: +4.14%

- Fresh meat: +3.64%

- Ready-to-eat meals: +3.64%

The increases in fresh fruits and vegetables are mainly attributed to the weather conditions that prevailed from January through early May 2026, with increased rainfall, low temperatures, and flooding affecting production and causing delays in the new harvest of seasonal items.

In contrast, the remaining product categories show relatively small price fluctuations. Notably, the 22 product categories, excluding fresh fruits and vegetables, recorded a total inflation rate of just 0.45%.

The reasons attributed to the trend of broader price moderation for supermarket products:

- Inflation containment. Prices have remained stable over the past two years in large food retailers due to the high volumes of products they handle, economies of scale, their organizational and technological readiness, and private-label products.

- High inventory turnover. Price stabilization occurs much more quickly at large retail outlets due to higher inventory turnover. That is, they move their inventory more quickly and make new purchases sooner to replenish stock.

- Impact of private-label products. The sales share of private-label products is higher in large supermarket chains due to a wider product range, and has been increasing over the past two years.

About the IELKA survey

The survey’s conclusions and results are based on an analysis of all actual monthly sales rather than on a sample.

For the purposes of the study, the change in unit value per product category (sales by volume) between May 2026 and May 2025 was analyzed. This specific index reflects both price trends and consumer purchasing choices.

The aim of the study is to objectively record prices separately in the organized retail channel (supermarkets), which is now the primary distribution channel for basic consumer goods, with significant operational differences compared to the rest of the market due to both government measures and economies of scale.

The survey is conducted monthly, comparing price trends with the corresponding month of the previous year.