For Ray Dalio , the AI market is a bubble and it will burst. “All major technological changes produce bubbles,” he told Bloomberg yesterday. According to him, AI companies will spend $800 billion on capital investments this year alone. However, only 1% of their executives worldwide report a significant return on their AI investments (ROI).

By 2030, the industry needs $2 trillion in revenue to justify what is being built today, but Bain estimates it will fall short by $800 billion, Dalio emphasized.

For now, investors are rewarding companies that lay off employees due to AI, as this is seen as proof of technological progress in exchange for a theoretically dramatic increase in productivity in the future. This may be reflected immediately in companies’ financial statements, but the same cannot be said for the confirmation of productivity gains through external measurement.

Sometimes layoffs allow a company to report strong financial results in the short term, masking problems elsewhere. This does not mean they cannot be part of the company’s technological restructuring process.

In fact, the history of major technological changes shows that an increase in layoffs is not automatically linked to an increase in productivity, which translates into increased production. The railroad revolution dramatically increased the transport of people and goods. Machines did the same for industrial production. The internet created new markets and reduced distribution costs.

Dalio, like others, does not dispute artificial intelligence (AI) as a technology. They dispute the economics behind AI, pointing out that every bubble in history has had more or less the same ending.

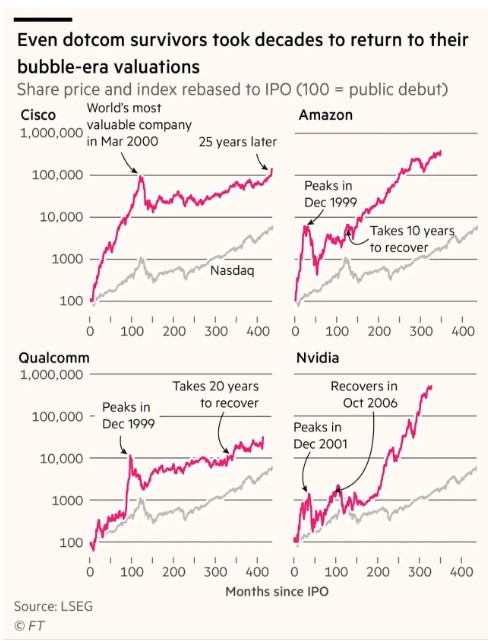

Typically, such narratives sometimes lead to stock market traps from which it takes investors years or decades to escape. The most notable example is the dot-com bubble of 2000. The charts below illustrate the stock performance of four companies that survived the “bloodbath”: Cisco, Qualcomm, Amazon, and Nvidia, from their debut on Wall Street to the present day.

It took 25 years from March 2000, when Cisco’s stock hit its all-time high, for it to return to that same level. It took Qualcomm’s stock about 20 years to recover from December 1999 and Amazon’s stock 10 years from December 1999. Even Nvidia stock, which peaked in December 2001, took five years—until 2006—to recover.

Obviously, the time it takes to recover is linked to the price at which the shares were purchased. Even if someone chose the right technology and company—e.g., Amazon, Nvidia— it will take a long time to recover if the purchase price was high and the valuation was wrong. This is exactly what happens when there is euphoria and a stock market bubble. The investor thinks the stock is a bargain because they believe it will keep going up. However, they later discover that this is not the case.