The year 2026 finds the global economy at a rare historical turning point. After a fifteen-year period in which growth was driven by software, platforms, and intangible business models, the global economy is returning to the physical world: energy, networks, industry, defense, and infrastructure.

This return is not theoretical. It is measurable.

The global computing power of AI data centers is expected to increase by 110% between 2024 and 2027. Each hyperscale center requires up to 50,000 tons of copper, approximately 500 tons of aluminum, and significant amounts of silver for high-conductivity applications.

The International Energy Agency estimates that the energy transition will require double the consumption of copper, lithium, nickel, and cobalt by 2030.

At the same time, the geopolitically fragmented order—with tariffs, export controls, and resource nationalization—is turning metals into strategic tools of power.

In this environment, metals are no longer a cyclical trade. They are a strategic allocation. And the investor who understands the structure of their market also understands the decade ahead.

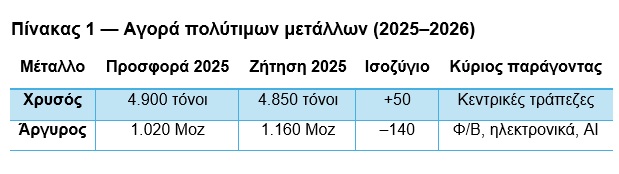

Precious metals — the technical divergence of gold and silver

Gold remains the ultimate hedge, but its momentum is stabilizing. The rise of recent years was supported by central banks and geopolitical uncertainty. With real interest rates normalizing, gold is moving into a zone of equilibrium.

Silver, on the other hand, is at the center of a technological boom in demand. Over 50% of its consumption is industrial—photovoltaics, high-density electronics, AI applications. In 2025, a deficit of 140 million ounces was recorded, the third consecutive one.

Silver is the only precious metal with a purely industrial growth driver—and that makes it critical for the coming decade.

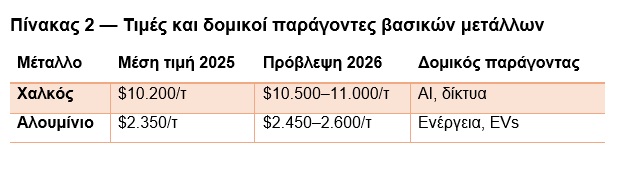

Base metals — the AI infrastructure supercycle

Copper is the metal defining the decade. S&P Global forecasts a 150,000-tonne deficit in 2026, which could exceed 500,000 tonnes by 2028. The price above $12,000/ton in 2025 was not a bubble; it was the market discounting a new era.

Copper is the “lifeline” of the AI economy. Every server, every cooling system, every transformer, every kilometer of transmission line depends on it. The phrase “copper is the new oil” is no exaggeration.

Aluminum, which is energy-intensive to produce, is benefiting from the energy crisis in Europe and rising demand from EVs and photovoltaics. Supply remains tight.

Copper and aluminum are now infrastructure metals, not cyclical industrial commodities.

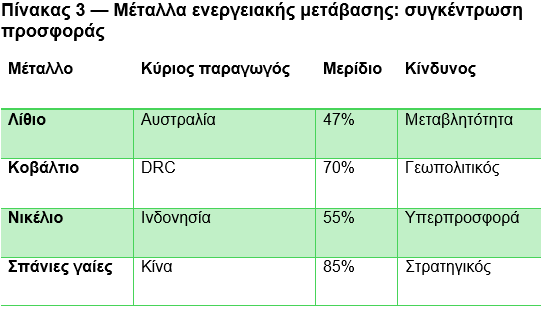

Energy transition metals — the technical picture of shortages

Lithium has rebounded sharply, but EV penetration continues. Cobalt remains geopolitically vulnerable because 70% of production comes from the Congo. Nickel is oversupplied due to Indonesia, but high-purity nickel (Class 1) remains scarce. Rare earths are 85% controlled by China.

The energy transition cannot proceed without these metals. The shortages are structural.

Ferrous metals — the new industrial geography

China is slowing down, but India is growing at a rate of over 7%. The West is bringing back defense, EV, infrastructure, and energy production. Demand for steel is shifting from construction to strategic industries. Iron ore remains in balance, but quality (62% Fe vs. 65% Fe) is becoming critical.

What does all this mean for investors

For investors, the key distinction is between structural and cyclical demand. The former defines the decade. The latter creates opportunities, but not strategic positions.

Structural demand concerns metals that form the backbone of the new economy: artificial intelligence, high-power networks, electromobility, renewable energy sources, and defense. This includes copper, silver, aluminum, and rare earths. These metals do not follow the economic cycle; they follow the very architecture of the future. They are the metals of conductivity, energy storage, networks, and critical technologies. Their demand is structural, inelastic, and long-term.

Cyclical demand pertains to metals that exhibit high volatility but remain indispensable for the energy transition. Lithium, nickel, and cobalt fall into this category. Their prices fluctuate sharply due to supply, geographic concentration, and technological changes, but their long-term need is a given. This category offers tactical opportunities—but not a stable core portfolio.

The defensive anchors remain gold and the platinum group metals (PGMs): platinum, palladium, rhodium, iridium, osmium, and ruthenium. These metals are used in catalysts, chemical processes, specialized industrial applications, and critical high-tech value chains. They are not growth metals; they are stability and hedging metals, serving as a safety net during periods of instability.

The above is not an investment recommendation—it is an analytical framework. The coming decade is also a material one. And metals are at its core.

Conclusion — The decade built on metals

The next decade will be defined by the expansion of networks, the development of AI infrastructure, electromobility, and reindustrialization. All these transitions are metal-intensive. Software may run the world, but metals build it.

Sources: International Energy Agency (IEA), Global Critical Minerals Outlook 2025 — supply and demand for copper, lithium, nickel, cobalt, rare earths, energy transition, International Energy Agency (IEA), Copper – Analysis — copper demand forecasts through 2040, Silver Institute, World Silver Survey 2026 — silver deficit, demand 2025–2026.

* Nicholas Havoutis has many years of experience leading strategic financial units, having served as an executive at JPMorgan (New York), Chase Manhattan Bank (London), and Eurobank (Athens). At the same time, he has a significant presence in the SME sector. Today, as head of SoZone Limited, he advises companies and investors on international expansion, organic optimization, and M&A strategies.