MARKETS: SpaceX’s debut on Wall Street was the most expensive in history. Elon Musk’s company raised $75 billion, with a valuation of approximately $1.77 trillion, automatically joining the ranks of the world’s largest companies.

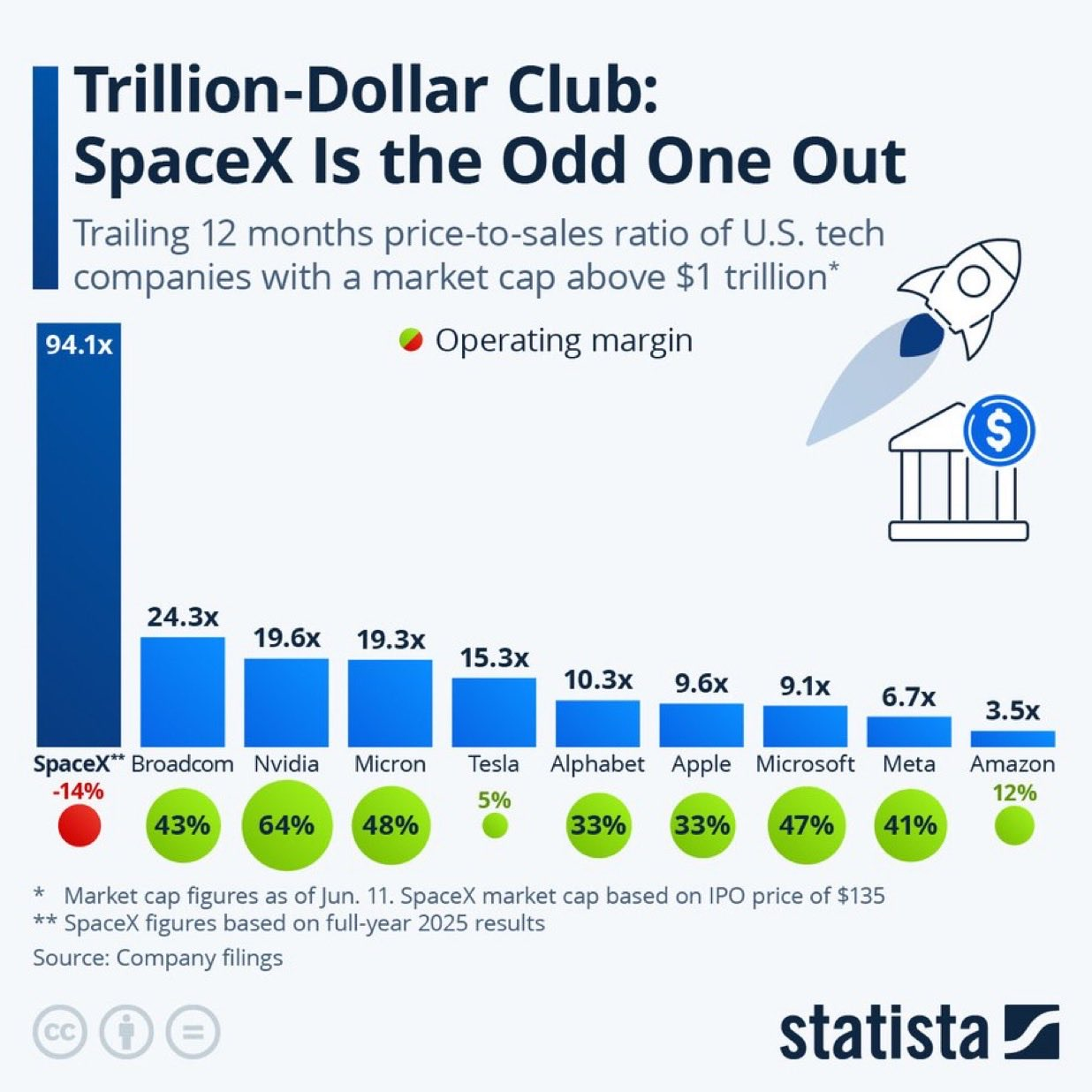

The comparison is nothing short of impressive—even… terrifying. At its IPO, SpaceX was valued at 94 times its… revenue (and rose… 19% in a single day), while Nvidia is at 20 times, Apple and Microsoft are close to 10, and Amazon is at 3.5.

Note also that SpaceX has a negative operating profit margin, while most major tech companies have margins of 30%, 40%, or even 60%.

In practice, participating investors paid “whatever it took,” to an unprecedented degree, to buy into a narrative. That space, satellites, communications, and artificial intelligence will create a new field of profitability, with unlimited prospects.

They may well be right. The problem is that, at such valuations, even a very “sound” story can become risky, as this market capitalization seems to discount almost all positive scenarios.

Two artificial intelligence companies are also hot on the heels of Musk’s firm. OpenAI is reportedly already filing for an IPO, according to Reuters, aiming for a valuation that could reach up to $1 trillion, in a listing that could take place as early as September.

Even more impressive is the case of Anthropic, the company behind Claude. It recently raised $65 billion in a new funding round, with a valuation of $965 billion, surpassing OpenAI’s previous valuation. It is now preparing for an initial public offering (IPO) to capitalize on the market window and secure funds for new investments.

Meanwhile, concern among a large segment of analysts and experts is growing over this trajectory toward… the stratosphere of valuations. Thus reminding the most optimistic, who… ignore them, that “markets are climbing a wall of worry.”

MARKETS II: The risk these experts see concerns not only new listings at “mythical” valuations, but also the way in which stock prices are rising, almost unstoppably.

As we have written before, leveraged stock trading is at very high, almost unprecedented levels. As the market rises, this fuels the rally. But when the tide turns, leverage becomes an accelerator of the decline.

At the same time, the gap between bond yields and stock earnings yields has narrowed dramatically compared to the past, and in some cases has nearly reversed.

In other words, investors now receive little or no additional return for buying stocks (which carry risk) instead of government bonds. This does not mean that a correction will occur tomorrow morning. It does mean, however, that the “safety cushion” is getting smaller and smaller.

If the market decides that expectations for AI, satellites, and new technology have outpaced actual earnings, the crash could be extremely sharp.

And then it won’t just be Wall Street that’s affected. Large international portfolios, European markets, and, of course, Athens will come under pressure. Which may be a “small fish” and a bit of an oddball, but, more or less, it swims in the same pool of liquidity.

SAMARAS: People from all walks of life are reportedly passing through the former prime minister’s office in Kolonaki, with the scent of elections growing stronger than ever. Antonis Samaras is in constant contact with political allies both in and outside Athens and is organizing at the leadership level, targeting the “patriotic, right-wing segment” of the political spectrum.

His intention, according to a source close to him, is to convince people that his agenda includes not only national issues but also a range of other major problems plaguing citizens, such as demographic trends, the rule of law, Greece’s (lack of) productivity, and the neglect of small and medium-sized businesses.

According to the same source, if Messinios ultimately proceeds with the creation of the new party, a potential 6–7% share of the vote would equate to 20–25 seats in the new Parliament, which would effectively make him a key player in future developments.

When asked if he could engage in talks with New Democracy regarding the future, he did not rule it out, but with the necessary precondition that “New Democracy be without Mitsotakis at the helm.”

THEOCHARIS: Haris Theocharis has resumed his fierce criticism of the former prime minister. Following the label “far-right” he applied to him and Antonis Samaras’s response to the “former Potami executive,” the Deputy Minister of Foreign Affairs stated (on SKAI) that if the rumored new party is formed, it would be a “second betrayal.”

“In political terms, there is no reason for a party to exist that would vie for right-wing voters. Therefore, only personal motives can justify it,” he emphasized.

This came shortly after Kyriakos Mitsotakis’s interview, in which, when asked about Mr. Samaras, he said, “I cannot imagine that he would harm the party that gave him a second chance.”

And tensions are rising dangerously.

MYLONAKIS: It took two months of hospitalization, treatment, and rehabilitation in Greece and Germany before the Deputy Minister to the Prime Minister was able to return home.

Giorgos Mylonakis’s health is improving, and his recovery is described as satisfactory, bringing smiles to his loved ones and to the Maximos Mansion.

In fact, his social media account has already become active again, sharing updates on Kyriakos Mitsotakis’s political actions and government policy in general.

URBAN PLANNING: The urban planning scandal appears to have many more chapters ahead of it. The case file already involves dozens of individuals, while rumors are circulating in the market about possible developments involving high-ranking officials at the Ministry of Environment and Energy in the coming days.

What is sparking debate is the timing. A ring that, according to what has come to light, is alleged to have been operating for years, is being exposed precisely at the moment when the prime minister is pushing for radical changes to the way urban planning operates and the transfer of critical responsibilities to the central government.

Coincidence or not, the case reinforces the arguments of those who maintain that the current model, based on local government, has reached its limits.

Why, however, all of this had not come to light for so many years is a question that likely remains unanswered.

Local Government: The government and Haris Doukas are at odds at every turn. This was confirmed in the wake of the new Local Government Code and the transfer of urban planning responsibilities from municipalities to central government agencies.

In a video posted on Instagram, the mayor of Athens questions the credibility of the measures and wonders whether these specific changes can truly enhance transparency and combat corruption. “They’re putting the wolf in charge of guarding the sheep,” he remarks sarcastically.

The response came immediately from the Ministry of the Interior, whose sources stated: “Once again, the Mayor of Athens has chosen to demonstrate his complete ignorance of local government. Once again, before referring to the Code, we recommend that he study it (or at least ask ChatGPT).”

GEK TERNA: The group is proceeding with the acquisition of an additional stake in Optimus Energy through its subsidiary Sustainable Energy Solutions. Specifically, the GEK Group, which already owns 51% of Optimus, will acquire an additional 43% of the company from Energyshare IKE for a consideration of €15.17 million.

Based on a corresponding valuation (€35.29 million for 100%), the intra-group transfer of 51% of Optimus Energy from Heron Energy to Sustainable was carried out for €18 million.

ADMIE HOLDINGS: The rights offering of ADMIE Holdings, which begins on Tuesday, will be conducted, as is well known, with the cancellation of existing shareholders’ preemptive rights.

For domestic investors, however, who will participate in the public offering, preferential treatment will apply during the allocation of new shares, with the aim of ensuring that their stake after the rights issue is equal to what they hold today.

A preferential allocation mechanism, but with expanded criteria (i.e., investment behavior, trading activity, loyalty as company shareholders), will also apply to the new shares, which will be offered through a private placement (book building).

ABAX: The Board of Directors of the listed company is proposing to the shareholders a new two-year buyback program for up to 5,000,000 shares (i.e., up to 3.37% of the share capital) with a maximum price of 5 euros per share and a minimum of 0.50 euros per share.

Prior to this, a decision must be made to terminate the existing share buyback program early and to authorize the Board of Directors to proceed with the disposal of treasury shares acquired under the program.

ELLACTOR: Final dividend of €0.05 per share (net €0.0475), with an ex-dividend date of July 20, the Board of Directors proposes to distribute to shareholders, who, however, had received an interim dividend of €0.50 per share at the end of last December.

In January 2025, shareholders also received €0.85 per share due to a capital return totaling €295.96 million.

Finally, it is proposed that €5.45 million from the 2025 tax-free profits be distributed to board members, senior executives, and employees as a reward for achieving targets.

ELLAKTOR II: Last year, the total (gross) compensation of Board members soared to €10.8 million (in 2024 it was €5.63 million) as the group’s asset stripping was initiated and largely completed, with its activities focused on the real estate and hospitality sectors.

The group’s CEO, Thymios Bouloutas, received total (gross) compensation of €4.2 million from the parent company in 2025, of which €4 million came from bonuses (i.e., variable compensation). He is also entitled to an additional €454,000 as compensation for positions he held in the group’s subsidiaries.

Substantial bonuses are also allocated to the other members of the strategic planning committee (chaired by the CEO), who are non-executive board members. Specifically, €4 million to Konstantinos Toubouros, €1.25 million to Panos Kyriakopoulos, and €750,000 to Georgios Triantafyllou.

Konstantinos Toubouros and Panos Kyriakopoulos also received €242,500 (gross amount) each for their roles as consultants to Attiki Odos S.A. and an additional €60,000 each as members of the Board of Directors at REDS and AKTOR Concessions.

ELLACTOR III: As a result of the group’s transformation and its focus on the real estate development and management sector, and secondarily on the hospitality sector, it was decided to reduce the number of Board members from 10 to 9.

It is proposed that all current Board members be re-elected, with the exception of Aris Xenofos (former CEO of the HFSF and HRADF), who currently serves as Vice Chairman (an independent non-executive Board member).