The tax authorities have some unpleasant surprises in store for taxpayers who are unaware of the “secrets” of the joint bank accounts held by the majority of families, for many and varied reasons, the main ones being better management of their finances and providing for their heirs in the event of death.

However, since the overwhelming majority of household accounts include more than one account holder (spouses, children, or parents), there are also many tax pitfalls which, if not carefully managed, can lead to significant tax burdens.

For example, a transfer of funds from a joint account to an individual account or to another joint account may, under certain conditions, be classified by the tax authorities as an informal gift, triggering an audit.

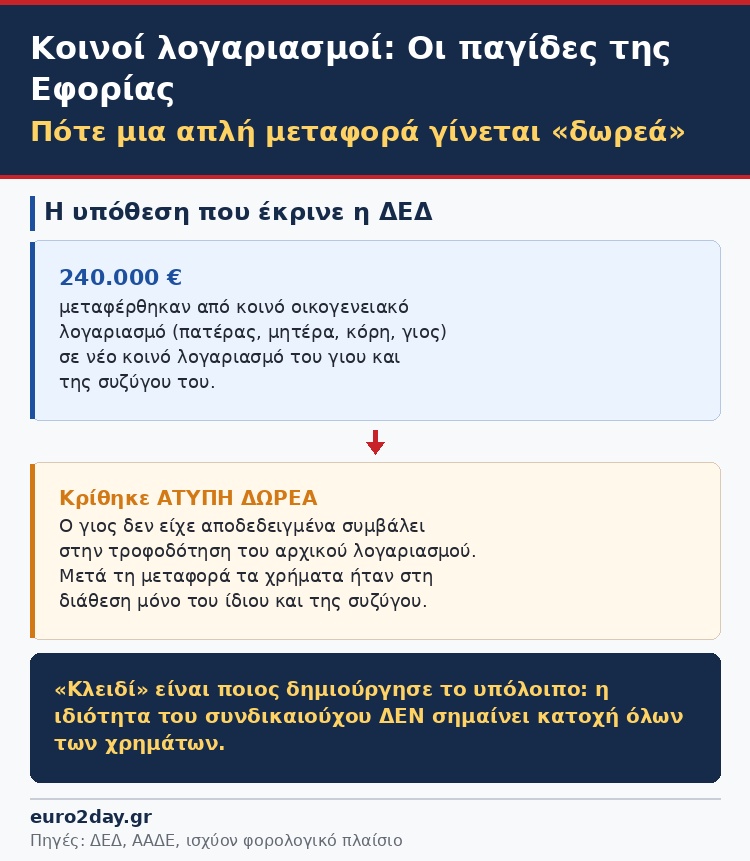

A typical example is a case that was referred to and reviewed by the Dispute Resolution Directorate (DRD), involving a transfer of funds from a joint account held by a parent and children to an individual account belonging to one of the children.

The DDS ruled that the transfer of 240,000 euros from a joint family account (father, mother, daughter, and son) to a new joint account held by the son and his wife constituted an informal gift.

The amount was considered a gift because the son who appealed to the Tax Appeals Board had not demonstrably contributed to the original joint account, and after the transfer, the funds were exclusively at his and his wife’s disposal.

The Tax Appeals Board’s decision, which rejected the taxpayer’s appeal, emphasizes that merely being a joint account holder is not sufficient to be considered the owner of all the funds in the account. If it is proven that the taxpayer did not contribute to the deposits and subsequently transfers the funds to an account under his or her control, this may constitute an informal gift for tax purposes.

The “key” is the creation of the balance

As stipulated by the current legal framework, when a joint account holder who has not contributed to the creation of the balance withdraws or transfers funds for personal use, the transaction may be considered a gift.

It is worth noting that thousands of cases involving financial parental contributions and informal gifts have been brought before the Dispute Resolution Directorate (DED), with taxpayers challenging taxes and fines imposed on them by the tax authorities and seeking their cancellation.

Many appeals concern parental gifts made in cash, rather than through the banking system as required by law, as well as cases of successive parental gifts to individuals who are not eligible for the 800,000-euro tax exemption.

Five Points to Watch

Five points that require attention are:

- Tax-exempt gifts up to 800,000 euros.

Cash gifts and parental gifts of up to 800,000 euros to first-degree relatives (parents, children, spouses, grandparents, and grandchildren) are tax-exempt, provided they are made through the banking system and properly reported. - Cash transfers are not tax-exempt.

When a parental gift is made in cash rather than through a bank transfer, a 10% tax is imposed with no tax-exempt allowance. - Transfers via IRIS

Sending small amounts from parents to children via instant payment systems, such as IRIS, for pocket money or to cover daily needs is not considered a gift and does not require filing a tax return, especially when the child is a dependent family member. - Successive Money

Transfers The Tax Authority carefully examines cases in which money is transferred successively among relatives to determine whether individuals who are not entitled to the tax exemption are attempting to take advantage of it. When such a practice is proven, a 20% tax may be imposed with no tax-exempt allowance. - Transfers to Joint Accounts

Particular caution is required when funds are deposited into a joint account held by the recipient and a third party. The tax authorities can investigate who ultimately used the funds and, if it is determined that the third party benefited, impose a gift tax. Experience in recent years shows that money transfers between relatives and joint account holders are increasingly becoming the focus of audits. For this reason, taxpayers are urged to keep complete documentation of their transactions and to strictly follow the prescribed procedures in order to avoid unpleasant tax surprises.

From the first euro

Those who are not eligible for the 800,000-euro tax-exempt threshold on parental gifts and donations lose their right to zero taxation and are taxed based on the degree of kinship or the method of transferring the funds, often starting from the very first euro.

The amount of tax is determined based on the reason for losing the tax-exempt status.

In the case of informal money transfers (in cash, without a documented bank transfer), if the recipients are first-degree relatives (parents, children, grandparents, grandchildren, spouses), the tax-free allowance is completely forfeited, and tax is imposed starting from the first euro at a rate of 10% of the total amount.

For second-degree relatives (siblings, nephews, nieces, uncles, aunts, stepfathers, stepmothers, great-grandfathers, and great-grandmothers), there is no tax-free allowance, and monetary gifts are taxed separately at a rate of 20% starting from the first euro.

The tax rate can even reach 40% for third-degree relatives or friends.

Under Scrutiny

The Independent Authority for Public Revenue (AADE) is now strictly scrutinizing cases where the 800,000-euro tax-free allowance is utilized.

According to the tax audit schedule, 1,080 cases related to financial parental gifts and donations are expected to be examined this year. The tax authorities are focusing primarily on cases where there are indications of circumvention of the 800,000-euro tax-exempt threshold. The relevant declarations are submitted electronically via the myProperty platform. The Independent Authority for Public Revenue (AADE) then cross-checks the data with the information provided by banking institutions.

If the bank does not confirm the transaction and the taxpayer does not provide the required supporting documents, the tax authorities may impose a tax without recognizing the tax-exempt threshold.