Just as important as establishing the terms and conditions for retirement as provided by law is—and sometimes even more so—the preparation of the insurance file for the thousands of EFKA insured individuals who are one, two, or even five steps away from becoming eligible for this benefit.

This is what social security experts point out, making it clear that a series of timely steps can significantly speed up the issuance of a pension, prevent errors in its calculation, and, in many cases, even lead to noticeably higher benefits.

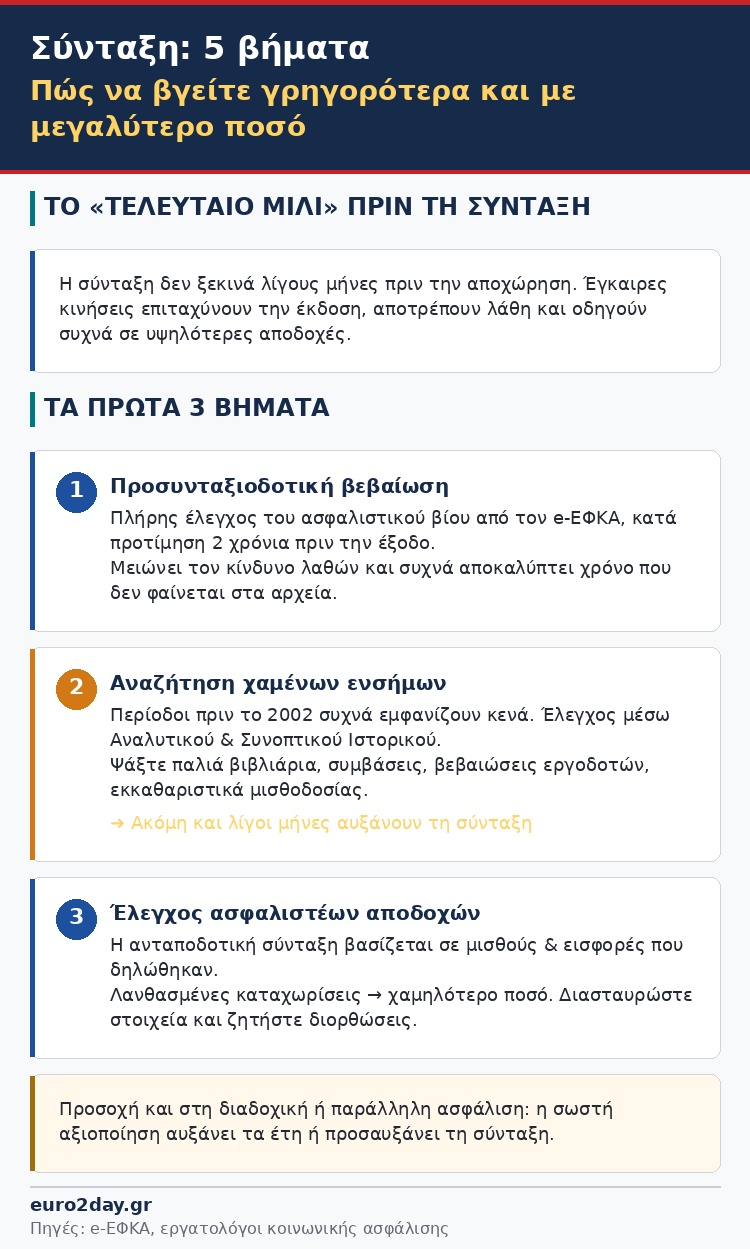

They also urge insured individuals who are in the… final stretch before retirement to be careful by taking five important steps that will lead to a faster or even higher pension.

The first step recommended by nearly all experts is to obtain a pre-retirement certificate from e-EFKA, preferably two years before retiring. This essentially involves a comprehensive review of one’s social security history, during which the total length of insurance coverage accumulated across all funds is recorded and verified.

This process reduces the risk of errors, facilitates the administration of pension payments, and often uncovers insurance periods that do not appear in the electronic records.

This is precisely where one of the most important steps lies—one that is crucial for a higher pension: the search for missing contribution stamps.

Despite significant progress in the digitization of social security data, several periods of employment—especially those prior to 2002—still have gaps. Many insured individuals discover shortly before retirement that months or even years of insurance coverage are missing from their electronic records.

Labor experts advise insured individuals not to wait until the last minute. The review should begin approximately two years before filing for retirement, using the Detailed and Summary Insurance History available through EFKA’s online services.

If any gaps are identified, individuals should search for old insurance books, employment contracts, employer certificates, payroll statements, or any other documentation that can prove employment.

Even a few months of insurance coverage can increase the pension, and in some cases, the recognition of lost time significantly affects the final amount.

Special attention is also required in cases of consecutive or concurrent insurance coverage. Many workers have been insured through more than one fund during their working lives or have paid contributions simultaneously to different agencies.

Properly accounting for this period can increase the number of years of insurance coverage or lead to a higher contributory pension. Experts recommend a thorough review before submitting the application, as in these cases, concurrent insurance translates to an additional monthly benefit.

Equally important is verifying the insurable earnings. This is the third and crucial step. The calculation of the contributory pension is based on the wages and contributions reported throughout one’s insurance history.

Incorrect or incomplete records can result in a lower pension amount. For this reason, insured individuals should cross-check their information and request corrections whenever discrepancies are found.

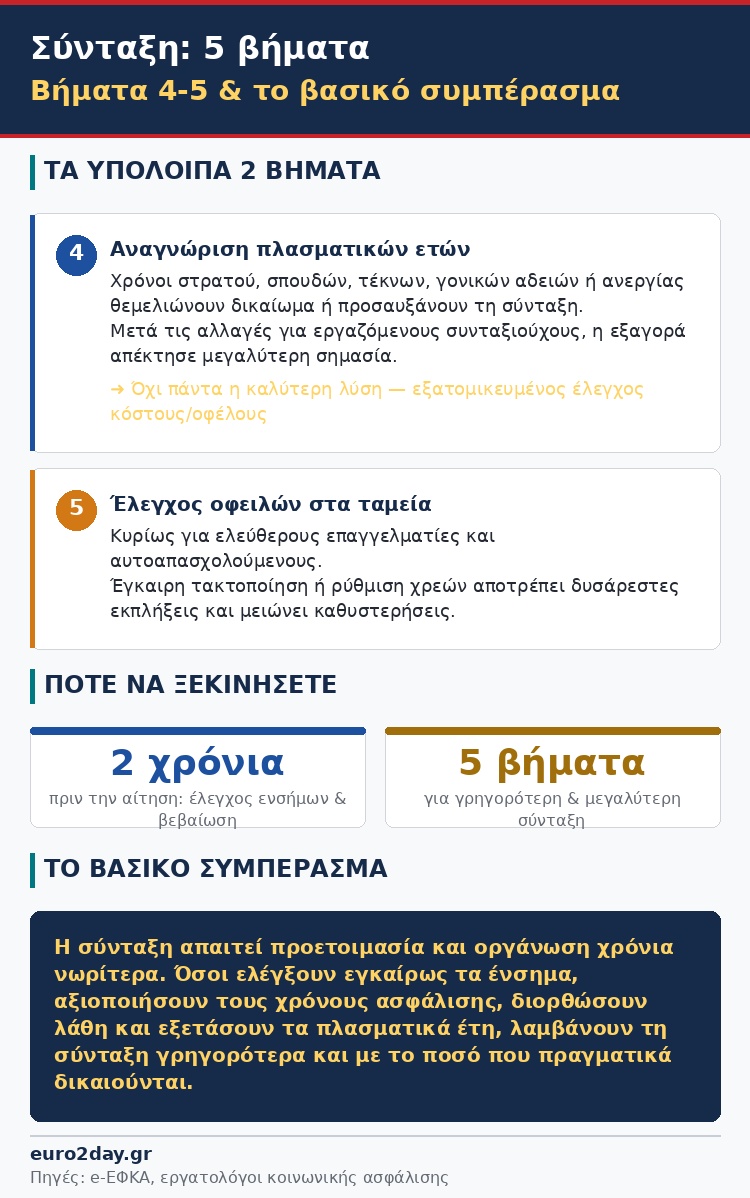

At the top of the list of options considered by those nearing retirement remains the recognition of fictitious years. This is the fourth, particularly careful and important step, as periods of military service, education, child-rearing, parental leave, or certain periods of unemployment can be used either to establish pension eligibility or to increase the pension amount.

Following changes to the employment regulations for retirees, the buyback of notional years has become even more important, as many insured individuals choose to retire early while continuing to work without losing their pension.

But be careful: Experts make it clear that buying back years is not always the best solution. A personalized cost-benefit analysis is required, as crediting service time can prove particularly advantageous when it leads to immediate eligibility or a higher replacement rate, but less efficient when retirement is still several years away.

Another point that is often overlooked is checking for any outstanding debts to social security funds, especially for freelancers and the self-employed.

The fifth step, therefore, involves settling or arranging for the payment of these debts in a timely manner, as this can prevent unpleasant surprises when the pension is issued and reduce delays.

The key conclusion reached by all social security experts is that retirement should not be treated as a process that begins just a few months before leaving the workforce.

Rather, it requires preparation, review, and organization several years in advance. Those who check their contribution records in a timely manner, make the most of their available contribution periods, correct any errors, and carefully examine the possibilities for recognizing fictitious years are more likely to receive their pension sooner, without complications, and, most importantly, in the amount to which they are actually entitled.