The Ministry of National Economy and Finance is introducing a legislative provision that provides substantial relief to thousands of borrowers with active repayment plans under Law 3869/2010, ensuring the full, universal, and uniform implementation of the recent decision by the Plenary Session of the Supreme Court, according to an announcement.

The legislative initiative resolves a critical issue that arose during the practical implementation of the ruling and clarifies beyond any doubt how interest is calculated in primary residence rescue arrangements. Specifically, it clarifies that interest is calculated on the monthly installment set by the court decision and only for the period between two consecutive payments, rather than on the total principal amount of the debt.

This clarification leads to a substantial and immediately measurable reduction in the monthly burden on debtors, as it eliminates a distortion that for years has placed an excessive burden on thousands of households.

At the same time, the provision provides for retroactive recognition of excess amounts already paid by borrowers in good standing with active repayment plans. These amounts are recognized as principal already paid, reducing the outstanding balance and correspondingly limiting the number of installments remaining until full repayment.

The same arrangement provides for a fair sharing of the relevant financial burden between the banks and the “HERACLES” state guarantee program, in proportion to the amounts each party has received. This approach strikes a balance between social protection, financial stability, and fiscal responsibility.

The legislative measure also clarifies that settlements reached through the Out-of-Court Mechanism continue to be governed by the current framework. The monthly payment under the out-of-court arrangement is calculated as an amortizing installment based on the total amount of the debt being restructured, rather than on the monthly payment itself, as already provided for by law, regulatory acts, and restructuring agreements.

WHAT EXACTLY DOES THE LEGISLATION PROVIDE?

1. For installment payments made from now on, interest is calculated on the monthly installment: For active payment plans as of June 5, 2026—the date of publication of Decision No. 6/2026 of the Plenary Session of the Supreme Court—interest will be calculated based on the monthly installment. More specifically, the interest provided for in Article 9(2) of Law 3869/2010 is calculated on the monthly installment set by the court. Each monthly payment includes a principal portion in the amount specified by the court decision and the interest corresponding to the period from the previous installment to the payment of the next installment. Specifically for the first installment, the interest period is calculated as thirty (30) days.

2. Retroactive overpayments made in connection with active repayment plans are recognized as principal paid and reduce the number of installments remaining to be paid:

For active payment plans that have not been completed or for which the conditions for declaring them forfeited have not been met as of the effective date of this law, provided that excess amounts have been paid since the start date of the repayment plan as specified in the court decision, or in cases where the repayment plan has been modified by a court decision, from the start date of payments under the most recent modification, then the difference between the total amount that was due and the amount actually paid for the aforementioned time period is deducted from the most recent installments due in chronological order, thereby reducing the total number of remaining installments due.

The difference between the interest paid and the interest that should have been paid, based on other methods of calculating interest, is treated as a principal repayment and reduces the outstanding balance of the debt as it stood at the time this law took effect. Any amounts paid in connection with settlement agreements that have been finalized or for which the conditions for declaring them void have been met shall not be recovered retroactively.

3. Any excess amounts collected by credit institutions during the period prior to the transfer of the loans to HERAKLES shall be returned by the credit institutions to HERAKLES.

4. It is clarified that in cases of out-of-court debt settlement arrangements, the monthly installment is calculated as an amortizing installment based on the total amount of the debt subject to the arrangement and not on the monthly installment itself, as provided for by law, in regulatory acts, in the settlement agreements, and in the calculation of the approved settlement to which the borrower agreed upon entering the settlement.

QUESTIONS AND ANSWERS

1. What does the arrangement achieve?

The arrangement achieves four critical things:

- It universally applies the Supreme Court’s ruling so that no borrower who has been making timely payments will need to go to court again.

- It substantially reduces the cost of repayment, as interest is now calculated only on the monthly installment and not on the entire principal.

- It retroactively recognizes any excess amounts paid and offsets them in the borrower’s favor, reducing the outstanding loan balance or the number of installments.

- It fairly allocates the costs between the banks and HERAKLES, based on the period during which the amounts were collected.

Therefore, borrowers benefit from: lower installments, a lower total cost, and faster repayment.

2. How do borrowers benefit?

Borrowers benefit directly in two ways:

- From now on, they pay a significantly lower monthly installment, with interest corresponding to only one month.

- Any additional amounts they paid in previous years are recognized as principal paid off.

This means that borrowers will see both a reduction in their monthly payment and a shorter repayment period.

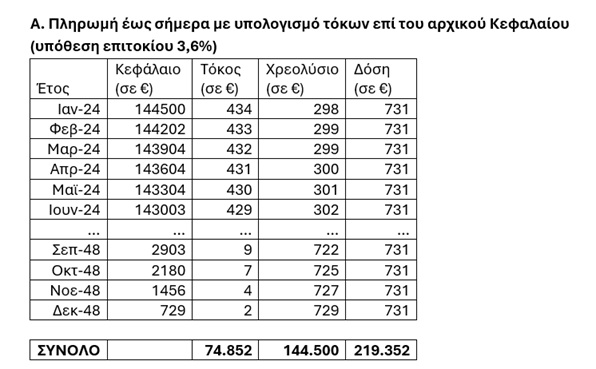

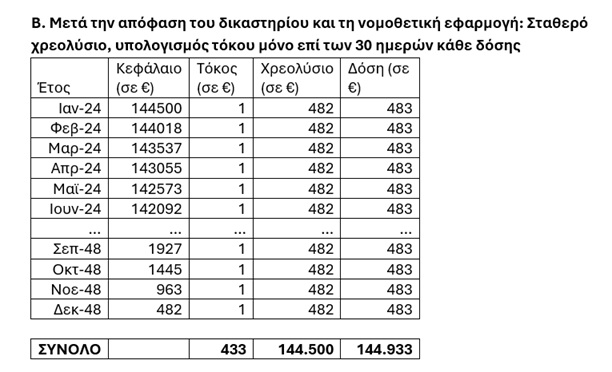

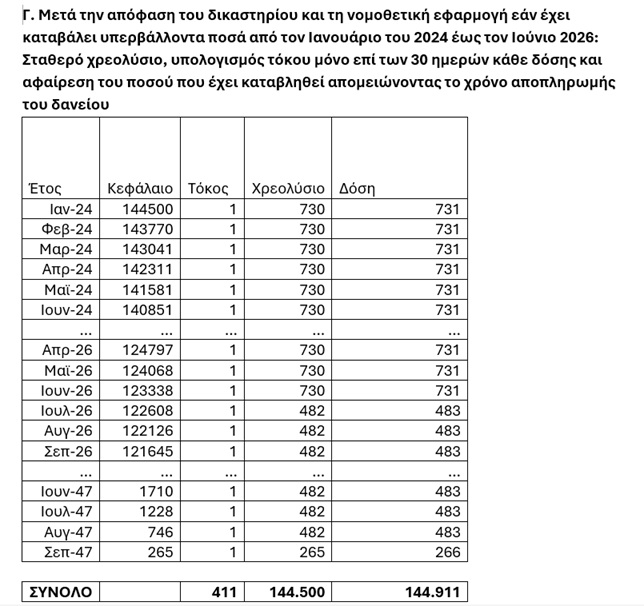

3. How much will the monthly payment actually change?

To illustrate how the calculation works before and after, consider the following example:

A borrower who had an outstanding balance of 144,500 euros in January 2024 would, under the previous calculation method, have paid a monthly installment of 731 euros for 300 months.

Under the new calculation method, they will pay an installment of 483 euros, consisting of 482 euros in principal repayment and 1 euro in interest.

If he paid 731 euros—the amount corresponding to the interest-and-principal installment—from January 2024 through June 2026, he would have overpaid by an amount equal to (731–483) × 30 = 7,440 euros over 30 months.

Consequently, instead of having 270 installments remaining to repay the loan, this amount is deducted from the remaining installments, and the borrower will ultimately pay 255 installments of 483 euros (with the final installment amounting to 266 euros).

In total, instead of paying 74,852 euros in interest, the borrower will pay just 411 euros.

4. Does the arrangement apply retroactively?

Yes, and this is one of the most important aspects of the arrangement. For those who have an active repayment plan and are consistent with their payments, the additional amounts they have paid are recognized retroactively. This retroactive effect was not provided for in the Supreme Court’s decision itself. It is granted by the government’s legislative intervention.

5. How is retroactivity applied?

The amount the borrower paid in excess of the agreed terms since the start of the repayment plan is calculated. This amount is deducted from the outstanding balance and reduces the final loan installments. The loan is paid off earlier.

6. Why is retroactivity not granted in cases that have been closed or declared in default?

Because in these cases:

- either the debt has been repaid and the primary residence has already been saved (usually through a lump-sum repayment of the remaining principal),

- or legal consequences have already arisen for both parties due to the non-payment of installments for a series of months or years.

A retroactive review of these cases would create serious legal and systemic uncertainty, as it would require reopening thousands of old cases, many of which are based on court decisions dating back a decade. Furthermore, in cases where the debtor has defaulted on the repayment plan, this means that a significant number of installments have not been paid. Therefore, there is no question of retroactive repayment for amounts that were never paid.

7. What applies to those under an out-of-court settlement or under Law 4605/2019?

In the case of other debt settlement mechanisms—specifically Law 4605/2019 and the out-of-court debt settlement mechanism— the provision explicitly stipulates that the monthly installment is calculated as an amortizing installment based on the total amount of the debt being settled, and not on the monthly installment itself, as is otherwise provided for in the law, in regulatory acts, in the restructuring agreements, and in the calculation of the approved restructuring plan to which the borrower agreed upon entering the restructuring program.

8. What is the cost to “HERAKLES”?

The reduction in installments results in lower future collections for the “HERAKLES” guarantee program.

Specifically, the total impact is estimated to be approximately:

- 500 million euros over a 20-year period, due to lower installments on loans totaling 16.5 billion euros

- an additional approximately 200 million euros from the retroactive application of the measure.

However, a significant portion of the retroactive costs will not be borne by the government, as they will be covered by the credit institutions themselves.

9. Why is legislation necessary now that the Supreme Court has ruled?

The Supreme Court’s decision provided the basic direction. However, during its implementation, differing interpretations arose regarding the time period for calculating interest on the monthly installment (i.e., whether it is calculated for the entire period from the start of the repayment plan until the payment of each installment, or the more favorable scenario, which applies only to the 30 days between two installments).

Furthermore, the decision did not specify what happens with retroactive payments.

The legislative intervention is intended to definitively resolve any ambiguity. This clarifies the calculation method, ensures uniform application for all, and eliminates the need for borrowers to resort to the courts again. This is the key benefit. With this legislation, it becomes a universal, enforceable, and immediately applicable right for thousands of borrowers.