Insurance companies are in the midst of… weeding out policyholders with lifetime health insurance policies by imposing “inflated” premiums, as the old and “generous” insurance plans entail extremely high claims costs.

At the same time, insurance companies are burdened with high costs associated with elderly policyholders, which explains the equally sharp increases in their premiums.

Data released by the Hellenic Statistical Authority (ELSTAT), announcing the new Annual Adjustment Index for Long-Term Health Insurance (AIR) for 2024, confirm that insurance companies are rapidly “clearing out” their portfolios of old health insurance policies, which are no longer offered, while those who still hold such policies from the past are facing significant premium increases, which often lead them to cancel their plans.

Specifically, as reflected in ELSTAT data,

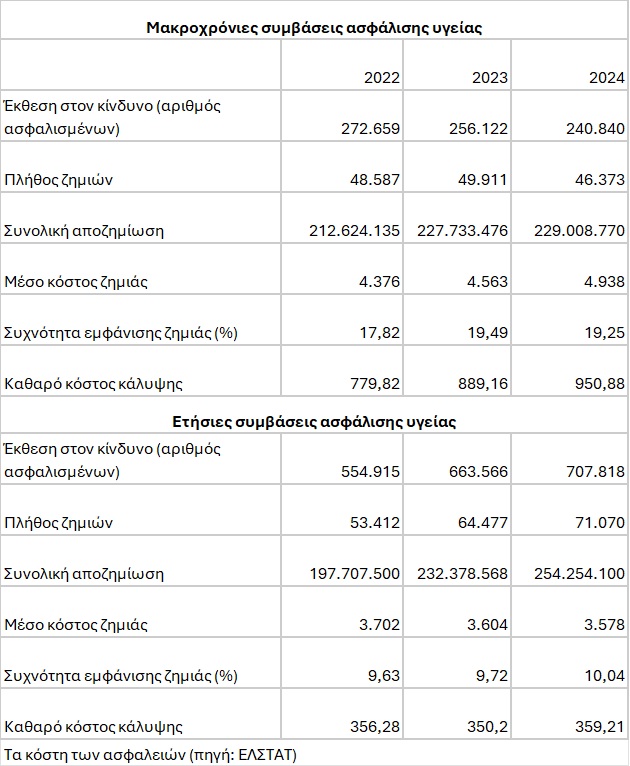

- between 2022 and 2024, the number of policyholders with long-term (whole-life) policies decreased by 31,819 (from 272,659 in 2022 to 240,840 in 2024). Obviously, part of this decrease is due to the deaths of policyholders, but the majority is explained by policy cancellations.

- In contrast, the number of policyholders with annually renewable policies increased by 152,903, reaching 707,818 in 2024 from 554,915 in 2022—an increase of nearly 28%.

Whole-life policies: a “financial burden”

Lifetime policies are a financial “burden” for companies, which are, to a large extent, paying for their own past mistakes, when they offered very generous coverage to attract policyholders, but it is now becoming clear that their cost estimates were completely off the mark.

It is telling that in 2024, the claims paid out by insurers for whole-life policies amounted to 229 million euros, a figure not much lower than the corresponding claims for annual policies, which totaled 254 million euros. This occurred despite the fact that the number of policyholders with annual policies was nearly three times that of those with whole-life policies.

The costs of whole-life policies are exorbitantly higher than those of annual policies, where coverage has been “scaled back.” It is telling that, on average, companies pay 950 euros per year per policyholder for lifetime plans—an amount 2.6 times greater than the corresponding cost for annual plans.

An “ageing” time bomb for insurers

To measure the average annual change in hospitalization expenses (the net cost of coverage) paid by insurance companies, ELSTAT compiles, based on the new legislation, the Annual Adjustment Index (AAI), which starting next year will serve as the benchmark for premium increases. The new index reveals that population aging is the most significant factor driving up insurance costs for companies and, consequently, the premiums charged.

As ELSTAT points out, for the year 2024:

- For long-term contracts, the annual change in the adjustment index, taking age into account, was 7.23%, while excluding the effect of age, it was just 1.76%.

- For annually renewable contracts, the annual change including the age factor amounted to 5.36%, while excluding it was just 0.79%.

The EDA, with the inclusion of the age factor, shows a… cap that was 5.3% for 2022, rising to 10.7% in 2023 and skyrocketing to 16% in 2024, according to ELSTAT.

The “storm” of increases in 2026

Continuing its policy of pressuring policyholders with lifetime plans to either pay more or cancel their policies, insurance companies imposed significant premium increases in 2026, before the EDA index was published, which sets certain limits on this policy.

According to the aggregate analysis by the Independent Authority for Market Control and Consumer Protection (AAEA&PK), which analyzed data from 11 companies covering a sample of 231,797 policyholders with active long-term health insurance policies, the net base premiums for 2025 amounted to 295.44 million euros (before premium tax).

An analysis of the 2026 increases reveals the following highly interesting findings:

- When the weighting is based on the number of insured individuals, the average increase is 7.49%.

- When weighted by the value of premiums (net financial burden), the average increase rises to 8.20%.

- More than half of the insured individuals experienced significant premium adjustments. Specifically, for 130,119 policyholders (56.13% of the sample), the increase exceeded 8%. At the same time, 36,923 policyholders (15.93%) saw their premiums rise by more than 9%.

In its announcement, the AAEA&PK sounded the alarm regarding the companies’ practices, highlighting the following lack of transparency, although it did not proceed with sanctions, even though large fines had been imposed in the past, which were also “endorsed” by the Council of State in a recent ruling.

Specifically, the Authority notes that, in many cases, hospital costs are not clearly distinguished from age-based adjustments and other contractual adjustment terms.

Furthermore, the letters sent to policyholders do not follow a standardized format. They often omit key information, such as the simultaneous listing of the old and new premiums, the exact percentage increase, and a clear explanation of the basis for the calculation.