On June 11, 2026, the European Central Bank raised its interest rates for the first time since 2023, ending a period of almost two years of stability at relatively low levels.

The move came in response to an external shock: the war in the Middle East had disrupted oil flows from the Strait of Hormuz, sending energy prices soaring and pushing inflation to its highest point since 2023.

What is interesting is that just a few days after the ECB's decision, the US and Iran appear to be close to an agreement to end hostilities and reopen the Strait of Hormuz. Oil prices fell sharply internationally (though not at the pumps), markets breathed a sigh of relief — but the ECB had already moved, and the question now is whether this was a one-off, forced move or the beginning of a new tightening cycle.

What the ECB decided

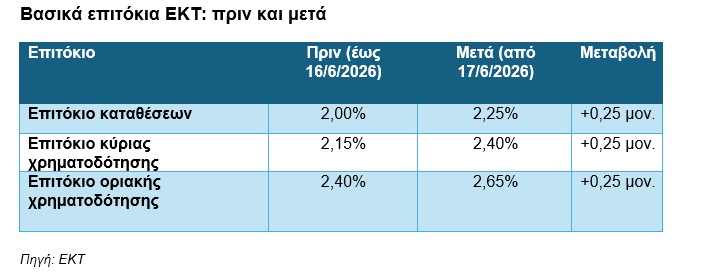

The ECB's Governing Council raised its three key interest rates by 25 basis points, bringing the deposit rate —the ECB's main policy indicator— to 2.25%.

It was the first increase since September 2023, when the rate had peaked at 4.0% before the easing cycle began, which lasted until early 2026.

The decision was not self-evident. Markets had priced it in almost with certainty in the last few weeks before the meeting, and as the minutes of the previous April meeting show, several members of the Governing Council would have supported an increase even then if the matter had been put to a vote. The environment had already been created.

Why inflation surged

The cause had nothing to do with reasons inherent to Europe. It was purely geopolitical: the war in the Middle East had cut off a large part of the oil flow from the Strait of Hormuz, through which before the war about one fifth of global oil and liquefied natural gas production passed.

This disruption created the biggest oil supply shock in history, and the effects quickly passed through the entire price chain.

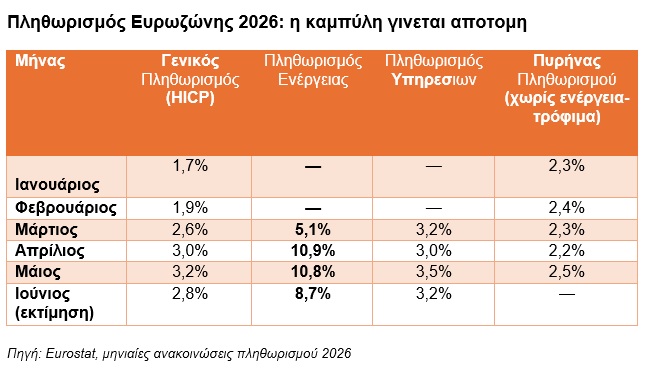

Within three months, headline inflation almost doubled. A worrying element for the ECB was not only energy itself, but also that core inflation —which excludes energy and food— also rose, from 2.2% to 2.5%.

This meant statistically, something we also observe in raw everyday life, that high prices were no longer limited to fuels, but had begun to spread to broader categories of prices.

The ECB's Executive Board had warned before the meeting that “the risk of inflation expectations becoming unanchored is increasing,” arguing that the ECB could no longer ignore the shock, regardless of the outcome of the peace negotiations.

Peace arrived fragile a few days later

Four days after the ECB's decision, the US and Iran announced a new agreement to end the war, with the immediate reopening of the Strait of Hormuz and the lifting of the US naval blockade of Iranian ports. The market reaction was immediate: Brent crude oil fell about 8% within one week, with stocks worldwide posting a relief rally.

The decline in the energy component of inflation in June (from 10.8% to 8.7%) probably already reflects this development. However, analysts warn that the full restoration of production and refineries will take months, and the ECB itself has described any peace as "fragile," with a risk of relapse. The question that remains open is whether the de-escalation in energy will be enough to avoid another interest rate increase at the next meeting, on July 24.

What the ECB forecasts

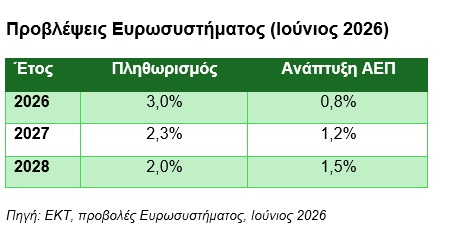

The Eurosystem projections, which accompanied the June decision, were revised significantly upward for inflation and downward for growth — even before the effect of the peace agreement was fully incorporated.

The eurozone had already contracted by 0.2% in the first quarter of 2026 compared with the previous quarter, even before the energy shock had fully manifested — a factor that raised concerns about stagflation (weak growth combined with persistent inflation).

The ECB acknowledges that the environment remains unusually uncertain, with upside risks to inflation if peace proves fragile, and downside risks to growth if high prices hit consumption.

What it means for loans and deposits

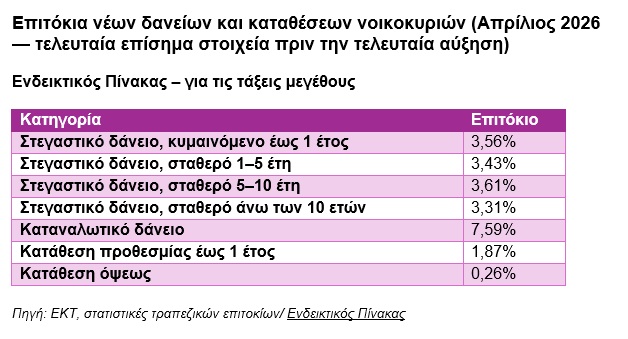

The increase in key interest rates is gradually passed on to bank rates, but the transition is neither immediate nor uniform. The most recent official ECB data, concerning April, show the picture just before the increase.

Mortgage loans were already on an upward path even before the ECB raised its interest rates in June, as banks had begun to incorporate expectations of tighter monetary policy. Deposits, by contrast, remain at low yield levels — much closer to 1.9% than to 3%+ — which means that savers still do not see a substantial benefit from the tightening.

Greece and Cyprus: exposed, but more resilient

Greece and Cyprus have double exposure in the current situation. Due to the lack of deep capital markets, they depend more on bank financing compared with other European economies.

As a result, the increase in borrowing costs passes more directly into the real economy. On the other hand, both countries are energy importers, and therefore more vulnerable to oil price shocks —and will benefit proportionally more from de-escalation if peace holds.

The positive element is that both banking sectors are entering this phase in much better condition than in the past: lower non-performing loans, stronger capital adequacy. This does not eliminate the risk, but it means that the system has more room to absorb the pressure without turning it into a crisis.

What comes next

The ECB's next monetary policy meeting is scheduled for July 24, 2026. Markets are already pricing in the possibility of one more increase within the year, although the possibility of a peace agreement in the Middle East reduces these expectations.

The ECB has stated that it will follow a “meeting by meeting” approach, without committing to a specific interest rate path, assessing incoming data on inflation and growth.

Conclusion: A forced move, not the beginning of a new crisis

The June 2026 interest rate increase is not a sign that the European economy is out of control. It is the reaction of a central bank that, after almost two years of stability, found itself faced with an exogenous shock that it could not ignore — and which, ironically, began to subside just a few days after its decision.

The critical question for the next period is no longer whether the shock was caused, but how deeply it has already passed into the economy. The elevated core inflation shows that the battle has not yet been decided, even if energy begins to become cheaper.

For households and businesses, the message is clear: the cost of money is not returning soon to its 2025 lows, and planning -borrowing, saving, investments- must take into account an environment of increased uncertainty, at least until it is proven that peace in the Middle East will hold.

Sources: European Central Bank (ECB) — Monetary policy decision, June 11, 2026, ECB — Monetary policy statements and Press Conference, June 11, 2026, ECB — Hearing at the European Parliament's Committee on Economic and Monetary Affairs, June 22, 2026, ECB — Bank interest rate statistics (MFI Interest Rate Statistics), January-April 2026, Eurostat — Monthly eurozone inflation releases (HICP), January-June 2026, Euronews — "ECB raises interest rates for the first time in three years as Iran war fuels inflation", June 11, 2026, NBC News — "Oil prices fall on Iran peace deal, but may not go much lower", June 15, 2026, Al Jazeera — "Oil prices fall, stocks rally as US, Iran sign framework to end war", June 18, 2026

* Nicholas Havoutis has many years of experience leading strategic financial units, having served as an executive at JPMorgan (New York), Chase Manhattan Bank (London) and Eurobank (Athens). At the same time, he has a significant presence in the media sector. Today, as head of SoZone Limited, he advises businesses and investors on international growth, organic optimization and merger and acquisition strategies.