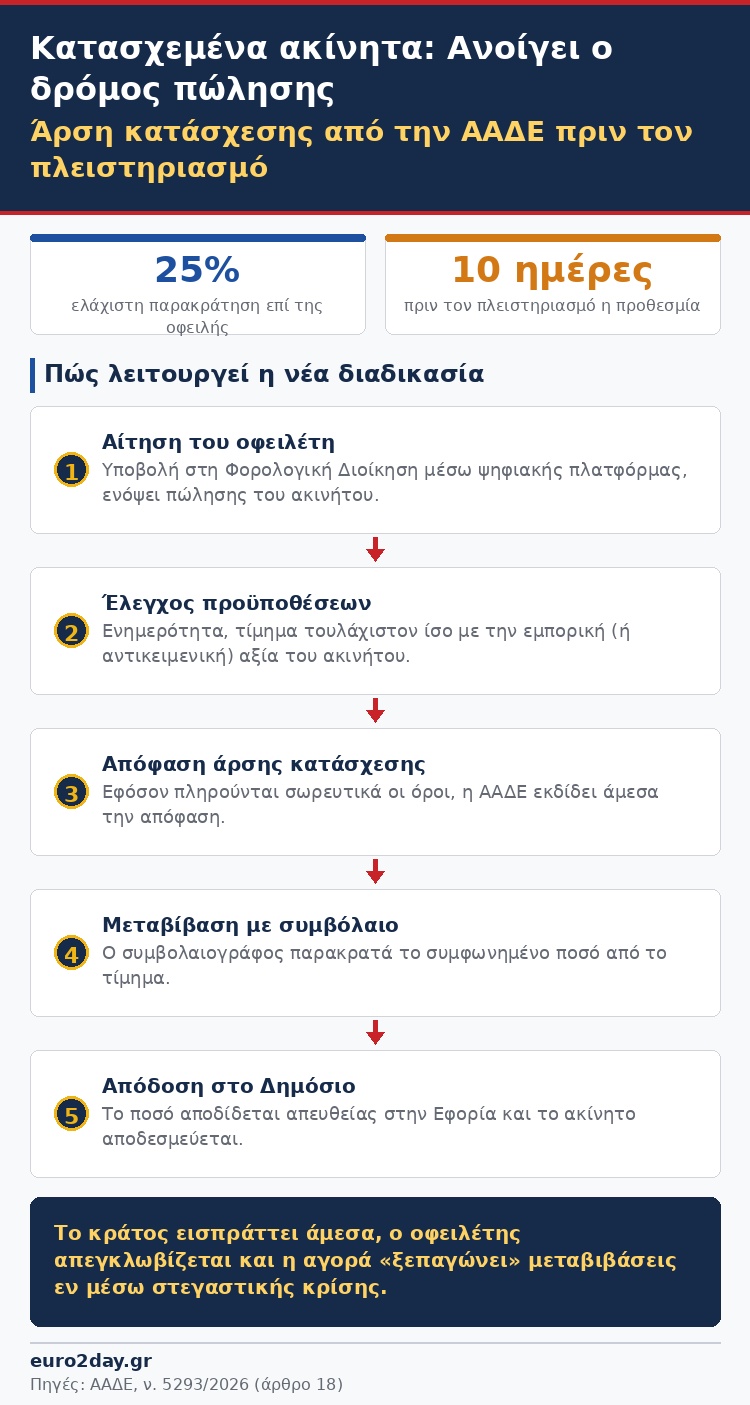

It is now only a matter of time before the decision of the Independent Authority for Public Revenue (AADE) is issued, for the activation of the provision (article 18 of law 5293/2026) that will open the way for the sale of thousands of properties that have been seized for debts to the Tax Office.

The regulation will give debtors to the State the possibility to release their seized properties for the purpose of their sale and purchase, so that the state can collect their debts and they themselves can escape from a dead-end situation.

The implementation of the measure is expected to unblock thousands of properties that remain idle (due to the seizure), giving debtors the possibility to sell them on the open market before they end up at auction, on the condition, however, that part or all of the price will be paid compulsorily directly to the State.

The withholding in favor of the State cannot be less than 25% of the debt, a condition that ensures repayment of the debt and releases the seized property with settlement of the remaining debt.

According to the current regime, the existence of a seizure by the Tax Office can block a transaction, even if there is an interested buyer and the possibility for the State to collect part of the debt. With the new procedure, the AADE will immediately collect part of the debts, while the debtor will be able to make use of his real estate property, which until today remained tied up.

At the same time, the real estate market acquires a mechanism for transfers of seized properties to “thaw” during a period of intense housing crisis.

Terms and conditions

The terms, the conditions and more generally the steps for lifting the seizure are described in the regulation, which is activated with the issuance of the implementing decision of the Tax Administration, with all the technical details, the digital platform for submitting applications, as well as the exact supporting documents that taxpayers must submit together.

Specifically:

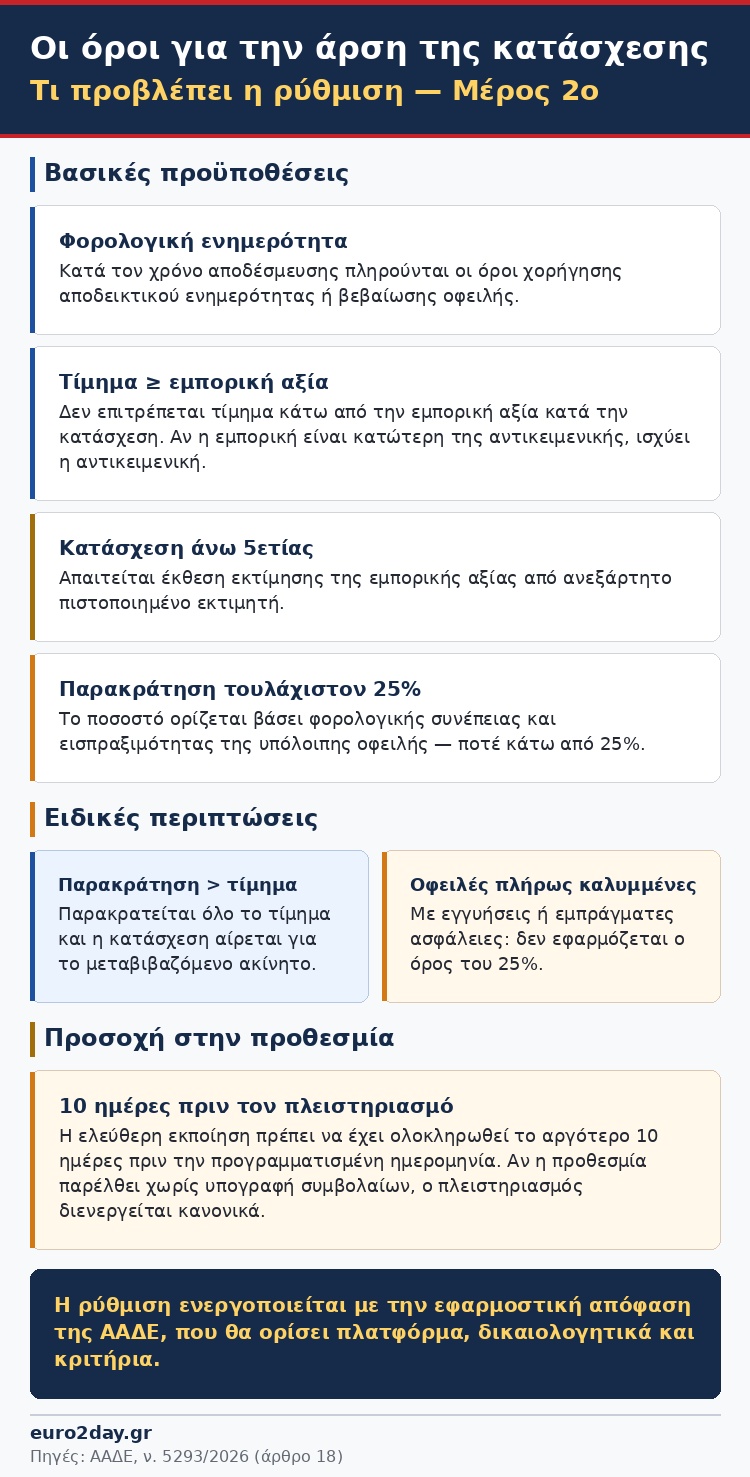

* The Tax Administration, following an application by the debtor, issues a decision lifting a seizure it has imposed on his property for certified debts to the Tax Administration, in view of its transfer for consideration with a price, provided that the following conditions are cumulatively met:

- At the time of release, the conditions for granting a tax clearance certificate or debt certificate are met.

- The transfer price may not be lower than the commercial value of the property, as this was determined at the time of the seizure.

- When the commercial value of the property is lower than its objective value, the objective value is taken into account.

- In the event that the seizure was imposed more than five years before the submission of the application, the debtor submits a valuation report of the commercial value of the property to be transferred from an independent certified appraiser.

- From the transfer price, an amount corresponding to a percentage of the total current balance of the imposed seizure is withheld and paid by the notary to the Tax Administration. The withholding percentage is determined on the basis of criteria of the debtor’s tax compliance and collectability of the remaining debt and in any case cannot be less than 25%.

- If the amount resulting from the withholding is greater, the greater amount is withheld and paid for the lifting of the seizure.

- In the event that the withholding amount exceeds the price, the entire price is withheld and paid and the seizure is lifted for the transferred property.

- The notary who draws up the transfer contract undertakes the obligation to withhold the agreed amount from the price and pay it directly to the Tax Office.

- In every case, the sale must be made for financial consideration that is deemed satisfactory for covering the claims or part of them, preventing fictitious or undervalued transactions.

* If the certified overdue debts have been fully covered by guarantees or real securities, the condition of the 25% withholding does not apply.

When the aforementioned conditions are met, the AADE immediately issues the decision lifting the seizure. The Governor determines the procedure, the form of the decision, the duration of validity and every necessary detail, including the criteria of tax compliance and collectability of the remaining debt.

Auction

It is worth noting that the process of free disposal must have been completed no later than ten days before the scheduled date of any auction. If the deadline passes without contracts being signed, the auction is conducted normally.