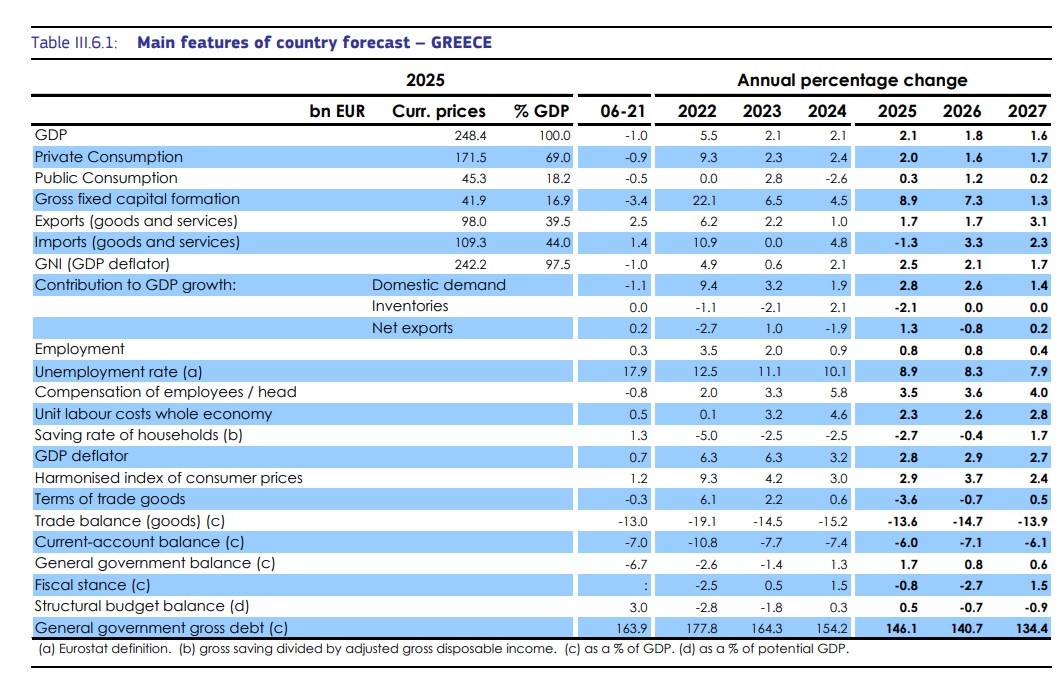

Economic activity in Greece is projected to slow from 2.1% in 2025 to 1.8% in 2026, as the energy price shock erodes real household income and limits consumption growth, the Commission notes in its spring economic forecast. Investment growth, however, is expected to remain strong, supported by the continued absorption of EU funds.

In 2027, GDP growth is projected to slow slightly again to 1.6%, as the implementation of the Recovery and Resilience Facility (RRF) nears completion.

Inflation is expected to rise to 3.7% in 2026, driven by a significant increase in energy prices. In 2027, it is projected to decline to 2.4%; however, inflation excluding energy and food is expected to remain elevated as the price shock is passed on to non-energy components.

Unemployment is projected to decline further, albeit at a slower pace, reaching 7.9% in 2027. Greece is expected to maintain a favorable fiscal position, with sustainable surpluses during the 2025–27 period, despite expansionary fiscal measures.

Strong nominal GDP growth and fiscal surpluses are projected to continue driving the debt-to-GDP ratio steadily downward, bringing it close to 134% by the end of 2027.

EU funds mitigate the impact of the energy crisis

In 2025, the Greek economy maintained its growth momentum. GDP grew by 2.1% for the third consecutive year, driven by investment, private consumption, and net exports.

Investment activity is expected to remain strong in 2026, supported by a historically high inflow of EU funds to Greece through the RRF. However, the energy price shock is expected to reduce households’ real disposable income.

The expansionary fiscal package announced in 2025, including cuts to personal income tax and increases in public sector wages, combined with recent energy measures, is expected to partially mitigate this impact. However, private consumption is projected to slow.

Demand for imports is expected to remain strong, due to the high dependence of investment on imports. Output growth is projected to slow further in 2027, as investment slows with the completion of the RRF.

Overall, GDP growth is projected to moderate to 1.8% in 2026 and 1.6% in 2027, while remaining above the EU average. Risks remain tilted to the downside, as a prolonged energy crisis could limit service exports, particularly tourism.

The labor market continued to expand in 2025, with the unemployment rate falling to 8.4% in the last quarter, the lowest level recorded since 2008, although it remains above the EU average of 6%.

The long-term unemployment rate remained broadly unchanged, at around 5% —the highest in the EU—reflecting long-standing structural challenges, such as skills gaps and inadequate childcare and eldercare facilities.

Job vacancy rates continued to decline, although they still point to a tight labor market, particularly in tourism and construction. Employment growth is expected to continue, but at a more moderate pace, constrained by structural barriers and weaker economic activity.

The energy price shock is fueling inflationary trends

Inflation remained elevated in 2025, averaging 2.9%, reflecting strong demand, a tight labor market, and the impact of measures to combat tax evasion.

The recent rise in energy prices is expected to push up retail energy prices and, consequently, inflation in 2026, gradually passing through to the prices of non-energy goods and services.

In 2027, an expected correction in energy prices should support a decline in inflation; however, the lagged increase in prices of energy-intensive goods and services will keep inflation at elevated levels.

Furthermore, strong demand and wage pressures fueled by labor shortages will continue to influence price developments. As a result, inflation is projected to rise to 3.7% in 2026 and settle at 2.4% in 2027.

Sustainable fiscal strength despite expansionary measures

In 2025, the general government balance recorded a surplus of 1.7% of GDP, exceeding the 1.1% of GDP projected in the European Commission’s 2025 Autumn Forecast.

The stronger performance reflects lower-than-expected expenditures, particularly in current expenditures, as well as higher-than-expected revenues, mainly from VAT, supported by ongoing improvements in tax compliance.

In 2026, the surplus is projected to remain strong but to decline to 0.8% of GDP. This projection incorporates expansionary measures estimated at 0.6% of GDP in 2026 and 0.8% of GDP on a permanent basis from 2027 onward, including reductions in personal income tax, property tax, and VAT, as well as increases in pensions and public sector wages.

It also includes temporary energy support measures, estimated at 0.2% of GDP, which were adopted in response to the recent rise in fuel prices. These measures are generally targeted and include fuel subsidies for households, support for transportation and agriculture, a one-time payment to families with children, and compensation for ferry operators.

In addition, recently announced changes to existing measures, such as the increase in the pensioner allowance and the revision of income criteria for the rent subsidy, are estimated to have a fiscal cost of approximately 0.1% of GDP.

Furthermore, defense spending is projected to increase from 2.4% of GDP in 2025 to 2.6% of GDP in 2026.

Revenue developments, supported by nominal growth, are expected to partially offset the fiscal impact of these measures. In 2027, the general government balance is projected to remain in surplus at 0.6% of GDP. This reflects the continued moderate growth in spending. At the same time, several measures that reduce the surplus are expected to weigh on the balance, including the full annual impact of the 2026 fiscal package (0.8% of GDP), a further reduction in social security contributions (0.1% of GDP), and additional increases in public sector wages.

The public debt-to-GDP ratio fell to 146.1% in 2025, nearly 43 percentage points below its pre-COVID-19 pandemic high recorded in 2018. The ratio is projected to continue declining, falling to 134.4% by 2027, supported by strong nominal GDP growth and sustainable primary fiscal surpluses.