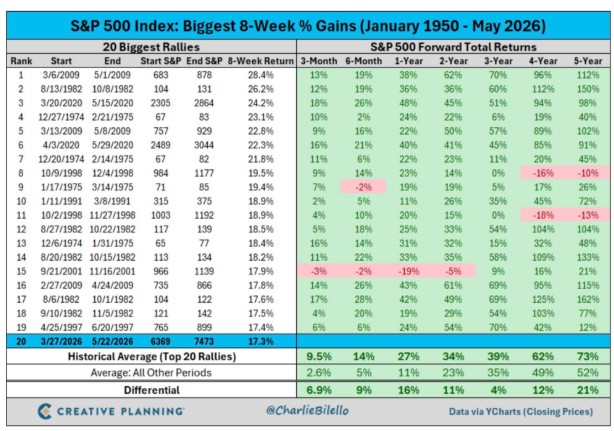

Every stock market has its own characteristics. It stands to reason that the Greek stock market is influenced by the state and prospects of the Greek economy, in which most listed companies primarily operate.But if there is one market that pulls the strings on a global level, it is Wall Street. U.S. stock indices have been rallying over the past 8 weeks, and this has not gone unnoticed by some analysts. As shown in the table below, the current rally, with gains of 17.3%, is one of the 20 largest recorded since January 1950.

Even more significantly, the S&P 500has recorded an average total return of 14% over the next six months, 27% one year after such a rally, 34% over two years, and 39% over three years. The 2001 rally was an exception, as was, to a lesser extent, the 1975 rally.

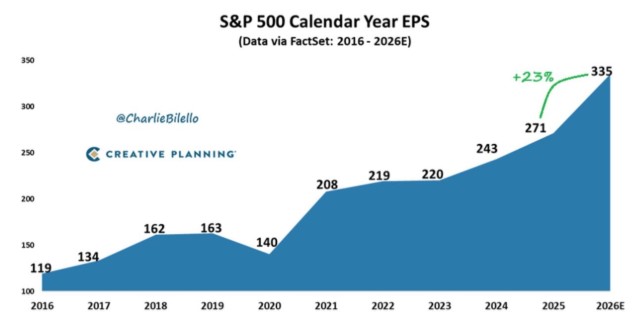

The recent rally is not without foundation. Listed companies reported a 28% increase in earnings in the first quarter, compared to expectations of 13%, resulting in an upward revision of corporate earnings forecasts for the entire year. The trend in earnings per share (EPS) for the S&P 500 from 2016 to 2026 is illustrated in the chart below.

Nevertheless, some remain unconvinced. One of them is Michael Hartnett of BofA, who believes that the current AI-driven rally resembles one of the biggest stock market bubbles in history. Nevertheless, he does not consider aggressive selling likely before the Fed begins implementing restrictive monetary policy and the cycle of a major OpenAI/SpaceX-style IPO is completed.

A few large-cap companies associated with AI dominate the S&P 500 index, with the result that the "AI bubble" is larger than past bubbles such as the railroad, Japanese, and dot-com bubbles, according to some indicators.

The bond market is sending the strongest warning signal, but it was recently noted in London “that fear in the bond market does not come close to the greed in the stock market.” Perhaps because investors believe that Trump wants to de-escalate tensions with Iran, boosting stocks and lowering bond yields.

Despite concerns about a bubble, Hartnett is bullish on emerging markets and commodities.

It is clear that Wall Street currently treats AI companies differently from the rest. If you don’t make AI chips, rent data centers, or sell automation, the U.S. market doesn’t pay you any attention.

For the more thoughtful observers, this is the picture of bull markets in their final stages. Today, the market is behaving as if AI could replace the real economy in the same way it saw no value in anything other than dot-coms in 1999. Or the speculative bubble of the American railroads in the 19th century.

Let’s see if history will end the same way this time around. The masses of investors chasing the glamour at the top, only to crash hard when the narrative loses its luster.