Debtors may… love to hate them, but debt collection agencies in Greece are raking in the profits. The market’s “Big 3” (Intrum,doValue, Cepal) report exceptionally high profitability, with operating profit margins (EBITDA) exceeding 60%—a figure most companies in the country would envy. Returns on capital are extraordinary, with rates many times higher than those of Greek banks.

It is an open secret in the market that this exceptional financial performance is not due to some “magic formula” for the efficiency of Greek debt collection companies, which, moreover, are slowly pushing forward the settlement of the loans that the great economic crisis bequeathed to the banking system.

As shown by a comparison of the performance of doValue’s individual subsidiaries in various European countries, Greece is… a goldmine of commissions for servicers.

Sanctions have eased…

It is worth noting that, so far, servicers have seen only the positive side of the “Hercules” plan. The original law on the securitization of “non-performing” loans with state guarantees was particularly strict, providing for heavy financial penalties—even the complete exclusion of a servicer from the securitization—in the event of failure to meet the business plan’s targets.

Despite the fact that, in practice, deviations from the initial securitization business plans proved to be significant, servicers managed to avoid the anticipated penalties, as the government determined that the failures in implementing the securitization business plans were due to the disruptions caused by the pandemic. The legislative framework was amended in a manner favorable to management companies, providing the institutional flexibility needed to make it very difficult to trigger the provisions for penalties.

Non-performing loans… are piling up

Seven years after the first securitizations under the “Hercules” plan, servicers’ activities continue to expand, as clearly reflected in the increase in total loans under management.

According to data from the Bank of Greece, in December 2025, the total value of credit servicers’ managed exposures reached €91.5 billion, an increase of €4.1 billion compared to December 2024.

This increase, explains the Bank of Greece, resulted from the assumption of management of new portfolios, primarily on behalf of credit purchasers (funds). Of the total exposures under management, €81.5 billion (i.e., 89.1%) relate to exposures managed by credit managers on behalf of credit purchasers (funds), while the remaining €10 billion (i.e., 10.9%) relates to the management of exposures on behalf of credit and financial institutions.

Profits of €126 million and substantial dividends

Analyzing the sector’s financial results for the 2025 fiscal year, what is striking is not merely the absolute figure of the profits, but an exceptional operational efficiency that would be the envy of companies across all business sectors—even the banks themselves.

There are currently 17 credit management firms operating in the Greek market, but in reality, the market is controlled by the powerful trio of the largest companies: doValue, Intrum, and Cepal control 84.8% of the total market, based on the value of exposures under management. These are the three companies created through the spin-off of the respective divisions of Eurobank, Piraeus Bank, and Alpha Bank.

According to aggregate data from the Bank of Greece, in December 2025 the total assets of credit managers amounted to €1.3 billion, marking an increase of €97 million compared to December 2024. Total equity fell to €614 million (from €739 million in 2024), as they proceeded with high dividend distributions to their shareholders. Profit after tax for all fund managers stood at €126 million in 2025, representing a slight decrease of 6.3% compared to 2024.

The “Big 3” are breaking the bank

An analysis of the individual balance sheets of the three major players, who manage the overwhelming majority of the market’s assets, fully explains why the sector is considered extremely profitable (Note that the data for doValue was derived from the parent company’s consolidated financial statements, as the Greek subsidiary has not published financial statements):

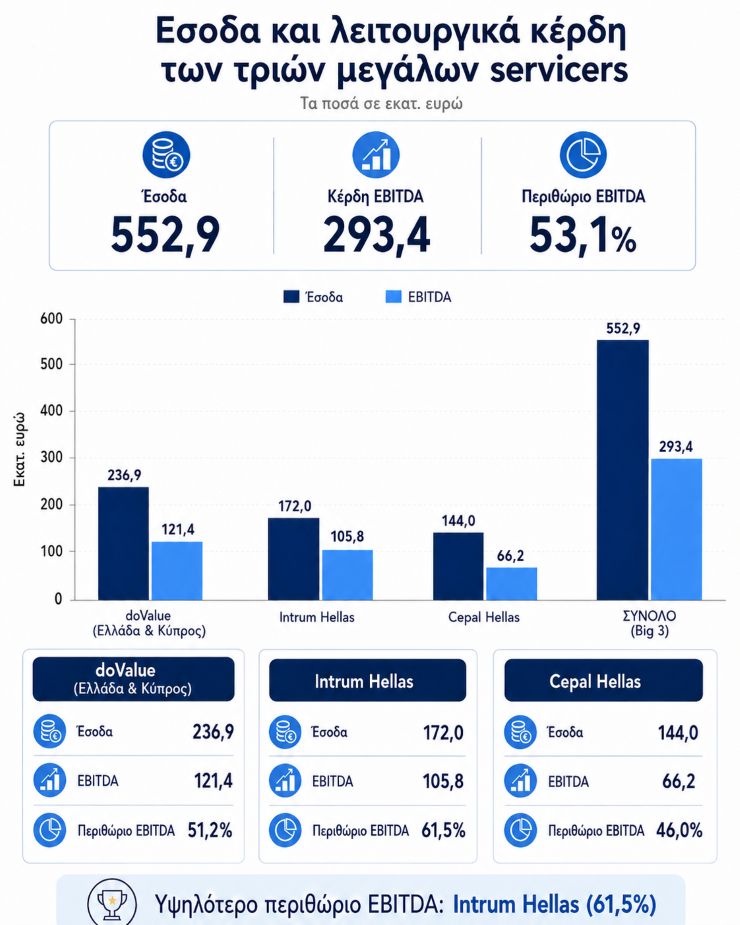

Intrum Hellas: This is the most characteristic example of high profitability. With revenue of €172 million, it achieved an operating profit (EBITDA) of €105.8 million, resulting in an impressive EBITDA margin of 61.5%. Net profit after taxes amounted to €60.6 million, while the return on equity (ROE) reached 54.2%, enabling the distribution of a total dividend of €53 million.

doValue (Hellenic Region): The Greece and Cyprus region has emerged as the primary driver of profitability for the parent group. With gross revenue of €236.9 million, the Greece - Cyprus region generated adjusted EBITDA of €121.4 million, resulting in an EBITDA margin of 51.2%. This is by far the best performance among the group’s subsidiaries. It is noteworthy that in Italy the corresponding margin was 31.1% and the Group average was 37.4%. The Greek region contributed nearly 56% of the Group’s total operating profit, even though it had significantly fewer loans under management than Italy.

Cepal Hellas: With €30 billion in loans under management, the company saw its net operating income reach €144 million. Net profits reached €19.7 million, with the EBITDA margin reaching 46% (compared to 44% in 2024), confirming its consistent ability to maintain high operational efficiency.