Some people are upset about the (temporary?) losses they suffered because they invested in stocks, and others because didn’t dared to do so. The latter belong to those who watched stock market indices rise over the long term while they themselves had put their savings in bank deposits and losing purchasing power as deposit interest rates were lower than inflation. Unfortunately, this is particularly true for Greek households. The latter are not only the only ones in the EU that have been spending more than they earn for over 15 years, according to OECD data. They are also the ones that hold the overwhelming majority of their financial assets in bank deposits.

From May 2016 through May of this year, the Athens Stock Exchange General Index has returned 164%. The return over the last five years is 150%.We doubt that a typical deposit offered a cumulative return of more than 15% over the same period, while inflation exceeded 25%.

Saving is valuable. However, if the money saved is not invested and simply becomes a bank deposit, households lose out.

Of course, it’s understandable that in the current climate, many are wondering whether they should invest in stocks after such a massive rally.

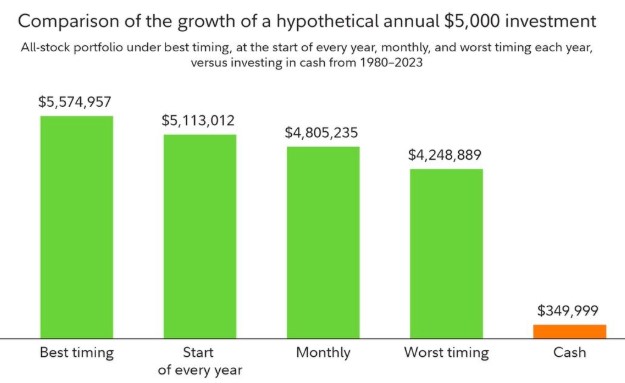

The answer comes from a study by Fidelity Investments, which examined what would happen if someone invested $5,000 annually in U.S. stocks from 1980 through 2023. It even compared the returns if the money had been invested at the best and worst times of the year.

The results showed that investing $5,000 in the S&P 500 index at the best time of the year for the stock market would yield $5.6 million by 2023. If the investment were made at the beginning of each year, the result would be $5.1 million.

If the $5,000 had been invested at the worst possible time each year, the total investment would yield $4.3 million. However, if the same amount of $5,000 per year had been deposited in a bank, the investment would have yielded just $350,000.

The conclusion is clear. Market timing is more important than the timing of the investment. There is a difference between $5.6 million and $4.3 million. However, neither amount compares to the mere $350,000 the depositor would have received.

“You have to be in it to win it,” said an old US Lotto ad, implying that you can’t win if you don’t play.

The phrase may have been a marketing tool to promote the Lotto, where the odds of picking the winning combination of numbers are one in a billion, but it holds true in the world of investing.

In investing, the real risk isn’t the sharp market fluctuations and often temporary losses, but rather not participating in the market—that is, never having started to invest, especially from a young age.