The stock market’s strong rally has narrowed the significant discount seen in previous years, but it has not eliminated it.

The new valuation landscape indicates that the Greek market has entered a more mature phase, where the upward momentum no longer applies across the entire market but rather to specific stocks with visible profitability, strong cash flows, high dividends, and target prices that remain well below current levels.

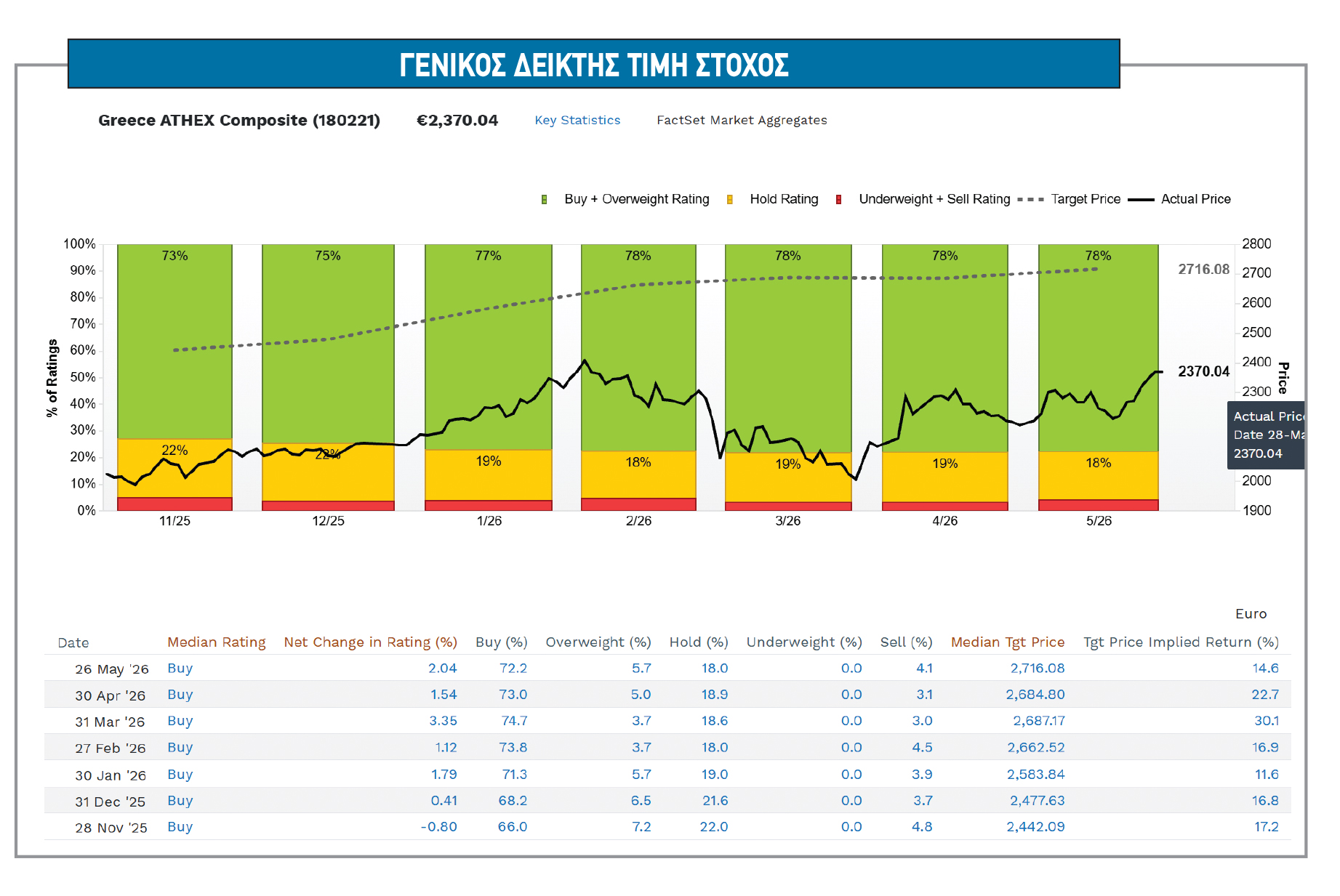

The average target price for the General Index, as indicated by analysts’ estimates, reflects the shift in market sentiment that has taken place. The index is currently at 2,370 points, while the median target price set by analysts stands at 2,716 points, suggesting a theoretical upside potential of 15%.

This picture comes after a period during which analysts’ estimates have been steadily rising. The median target price was 2,442 points at the end of November 2025, rose to 2,478 points in December, to 2,584 points in January, to 2,663 points in February, to 2,687 points in March, to 2,685 points in April, and to 2,716 points at the end of May.

The most significant factor is not only the rise in the target price, but the maintenance of a very high percentage of positive recommendations. The percentage of buy and outperform recommendations has risen from 73% in November to 78% in May, with simple hold recommendations limited to 18% and negative sell recommendations at 4.1%. This means that, despite the rally, analysts have not turned defensive toward the Greek market.

On the contrary, the overall stance remains positive, with the net change in recommendations at 2.04% in May and the median recommendation remaining in the “buy” category. Of course, the upside potential is now lower than the 30.1% shown in the table at the end of March, when the market correction had widened the gap from target prices.

Valuations

The reduction of the theoretical upside to 15% indicates that the market has already priced in a significant portion of the improvement in fundamentals. At the same time, however, the new rise in the median target price to 2,716 points indicates that analysts continue to incorporate better estimates for earnings, dividends, and valuations.

In other words, the stock market is no longer a market of generalized undervaluation, but remains a market with selective opportunities, especially where 2026 earnings and dividend yields provide support for valuations.

Target Prices

For individual stocks, the picture is clearly mixed. The largest theoretical upside potential is not necessarily found in the heaviest stocks, but in securities where either the market remains cautious or analysts value assets and future cash flows more highly.

Lamda Development shows the highest upside potential, at 81%, as the average target price of €11.30 compares to the current price of €6.30. Lamda’s case, however, is unique, as the valuation is not based on current profitability but on the value and development of the properties.

In the mid-cap segment, Premia Properties also shows a high margin of 48%, from €1.40 to an average target price of €2.10. The stock trades at a 2026 P/E of 6x and a dividend yield of 4.3%, figures that place it among the cheapest valuations in the table.

EYATH shows a margin of 32%, Fourlis 26%, ABAX 23%, Alter Ego Media 22%, Allwyn 21%, and Qualco 18%. The picture, however, is not uniform. In some cases, high upside potential is accompanied by limited liquidity or higher business risk, while in others valuations are already demanding, as evidenced by Qualco’s 2026 P/E ratio of 67.8 times.

Among large non-bank blue chips, Aegean Airlines stands out with an upside potential of 37%, as the average target price is 16.8, up from the current price of 12.3. The stock has a negative return of 13.6% in 2026, but the 2026 P/E of 8.6 times and the dividend yield of 7.4% create a strong combination of valuation and income.

Jumbo has an upside potential of 32%, with a target price of 30.9 compared to the current price of 23.5, despite a 15.8% decline since the start of the year. With a 2026 P/E of 9.5x, a P/BV of 1.9x, and a dividend yield of 6.2%, it remains one of the most notable cases where the market remains cautious, but the numbers still indicate significant upside potential.

Metlen has an upside potential of 27%, with an average target price of 52.1 from a current price of 40.9. The stock is trading at a 2026 P/E of 9.9x and a P/BV of 1.4x, while the dividend yield is estimated at 3.7%. The high-case scenario raises the target price to 61, indicating that some analysts see significantly greater value than what is currently reflected in the stock price.

Titan shows a 26% upside, with an average target price of 62.3 versus 49.5, a 2026 P/E of 12.2 times, a P/BV of 1.9 times, and a dividend yield of 2.8%.

On the other hand, there are stocks where prices have risen faster than estimates. Cenergy shows a negative margin of 16%, as the average target price of 21.1 falls short of the current price of 25 euros, despite a 66.7% increase in 2026. Euronext Athens has a negative margin of 12%, ADMIE 5%, Austriacard 4%, and HELLENiQ Energy 2%. In these cases, the market has already priced in a large portion of the positive scenario.

Banks

For banks, upside potential has narrowed, but valuations remain reasonable relative to profitability and dividends. Eurobank has a 19% upside potential, with an average target price of 4.7 from a current price of 4.0, a 2026 P/E of 9.4x, a P/BV of 1.3x, and a dividend yield of 4%.

Alpha Bank has a margin of 17%, with a target price of 4.6 versus 3.9, a 2026 P/E of 9.3x, a P/BV of 1x, and a dividend yield of 3.9%. Piraeus Bank has a 13% upside, with a target price of 10.2 from 9.1, a 2026 P/E of 9.6x, a P/BV of 1.3x, and a dividend yield of 5.6%.

The National Bank has a 12% margin, with a target price of 16.9 from 15.1, a 2026 P/E of 10.8x, a P/BV of 1.4x, and a dividend yield of 5.1%.

Bank of Cyprus presents an even better picture in terms of distributions, with a dividend yield of 9.1%, a 2026 P/E of 9.6x, and an upside potential of 16%, as the target price of 11 compares to the current price of 9.5. In contrast, Optima Bank has nearly exhausted its upside potential, as the target price of 10.8 is just slightly above the current price, with a 2026 P/E of 11.8 times and a P/BV of 2.4 times.

The Greek stock market is not cheap in the simple, generalized way it was a few years ago. It remains, however, attractive for select stocks, where 2026 P/E ratios are in the single digits or low double digits, dividend yields exceed 4% to 6%, and target prices still indicate clear upside potential. The market has entered a phase of stock selection.

From here on out, confirmation of earnings and dividends will matter more than the general narrative of Greece’s rerating.

The new target prices for| Company | Current price | Target price | Margin of change | 2026 Return | Market Cap | High target price | Low target price | P/E 2026 | P/BV 2026 | Dividend yield 2026 |

|---|

| TITAN S.A. | 49.5 | 62.3 | 26% | -5.8 | 3,892.8 | 70.0 | 55.0 | 12.2 | 1.9 | 2.8 |

| COCA-COLA HBC AG | 50.5 | 54.7 | 8% | 12.9 | 18,341.3 | 59.5 | 40.5 | 17.5 | 4.1 | 2.6 |

| METLEN ENERGY & METALS PLC | 40.9 | 52.1 | 27% | -6.6 | 5,843.9 | 61.0 | 42.0 | 9.9 | 1.4 | 3.7 |

| GEK TERNA S.A. | 43.1 | 44.1 | 2% | 69.5 | 4,455.5 | 54.0 | 27.0 | 27.4 | 2.1 | 1.0 |

| MOTOR OIL CORINTH REFINERIES | 36.7 | 37.9 | 3% | 16.9 | 4,068.0 | 41.0 | 31.5 | 5.8 | 1.0 | 5.9 |

| JUMBO S.A. | 23.5 | 30.9 | 32% | -15.8 | 3,157.6 | 37.5 | 21.1 | 9.5 | 1.9 | 6.2 |

| KRI-KRI MILK INDUSTRY S.A. | 24.9 | 25.1 | 1% | 31.1 | 823.3 | 25.1 | 25.1 | - | - | - |

| PUBLIC POWER CORPORATION S.A. | 21.0 | 23.1 | 10% | 15.4 | 12,545.3 | 26.7 | 17.4 | 13.7 | 1.1 | 3.8 |

| CENERGY HOLDINGS SA | 25.0 | 21.1 | -16% | 66.7 | 5,309.6 | 25.3 | 15.6 | 21.0 | 4.9 | 1.4 |

| HELLENIC TELECOMMUNICATIONS ORGANIZATION S.A. | 18.5 | 20.2 | 9% | 9.7 | 7,467.2 | 23.0 | 17.5 | 11.3 | 4.2 | 5.3 |

| NATIONAL BANK OF GREECE S.A. | 15.1 | 16.9 | 12% | 16.3 | 13,830.5 | 19.4 | 14.1 | 10.8 | 1.4 | 5.1 |

| AEGEAN AIRLINES SA | 12.3 | 16.8 | 37% | -13.6 | 1,110.9 | 19.4 | 14.7 | 8.6 | - | 7.4 |

| GR. SARANTIS S.A. | 15.4 | 15.5 | 0% | 12.6 | 982.3 | 16.7 | 13.0 | 16.7 | - | 2.8 |

| HELLY AG | 12.6 | 15.3 | 21% | -30.1 | 10,201.8 | 20.0 | 13.1 | 14.7 | - | 7.8 |

| LAMDA DEVELOPMENT S.A. | 6.3 | 11.3 | 81% | -12.0 | 1,107.3 | 12.7 | 8.6 | 31.3 | 0.8 | - |

| Company | Current price | Target price | Price range | Yield 2026 | Market Cap | High target price | Low target price | P/E 2026 | P/BV 2026 | Dividend yield 2026 |

|---|

| BANK OF CYPRUS HOLDINGS PLC | 9.5 | 11.0 | 16% | 19.5 | 4,132.5 | 11.6 | 10.4 | 9.6 | 1.5 | 9.1 |

| OPTIMA BANK S.A. | 10.7 | 10.8 | 1% | 38.1 | 2,357.1 | 12.7 | 8.5 | 11.8 | 2.4 | 2.8 |

| ATHENS INTERNATIONAL AIRPORT S.A. | 10.2 | 10.6 | 4% | -5.1 | 3,242.4 | 11.8 | 9.1 | 16.0 | 4.2 | 6.4 |

| PIRAEUS BANK S.A. | 9.1 | 10.2 | 13% | 33.2 | 11,185.4 | 12.1 | 8.5 | 9.6 | 1.3 | 5.6 |

| HELLENIQ ENERGY HOLDINGS S.A. | 10.1 | 9.9 | -2% | 21.1 | 3,093.0 | 11.3 | 8.8 | 8.1 | - | 5.1 |

| AUSTRIACARD HOLDINGS AG | 9.7 | 9.3 | -4% | 58.2 | 351.9 | 10.0 | 8.6 | 19.0 | 2.4 | 1.2 |

| QUALCO GROUP S.A. | 5.8 | 6.8 | 18% | -11.6 | 405.5 | 7.1 | 6.5 | 67.8 | 4.1 | 0.8 |

| ALTER EGO MEDIA S.A. | 5.5 | 6.7 | 22% | -13.0 | 320.5 | 6.9 | 6.5 | - | - | - |

| EURONEXT ATHENS HOLDING S.A. | 7.4 | 6.5 | -12% | 16.8 | 445.4 | 6.5 | 6.5 | - | - | - |

| THESS. WATER AND SEWAGE COMP. | 4.4 | 5.9 | 32% | 14.0 | 161.0 | 5.9 | 5.9 | - | - | - |

| FOURLIS HOLDINGS S.A. | 4.4 | 5.5 | 26% | 2.6 | 226.5 | 5.5 | 5.5 | - | - | - |

| EUROBANK S.A. | 4.0 | 4.7 | 19% | 15.8 | 14,402.6 | 5.5 | 4.1 | 9.4 | 1.3 | 4.0 |

| ALPHA BANK S.A. | 3.9 | 4.6 | 17% | 8.6 | 9,004.1 | 5.2 | 3.8 | 9.3 | 1.0 | 3.9 |

| ADMIE HOLDINGS SA | 4.0 | 3.8 | -5% | 31.3 | 925.7 | 3.8 | 3.8 | - | - | 1.8 |

| AVAX S.A. | 3.6 | 4.4 | 23% | 19.9 | 528.0 | 4.9 | 3.8 | 10.6 | - | 2.9 |

| BRIQ PROPERTIES REAL ESTATE | 3.0 | 3.5 | 14% | 2.4 | 142.9 | 3.5 | 3.5 | 8.2 | - | 5.6 |

| TRADE ESTATES REAL ESTATE | 2.1 | 2.2 | 8% | 4.6 | 250.2 | 2.7 | 1.7 | 8.6 | - | 7.3 |

| PREMIA REAL ESTATE | 1.4 | 2.1 | 48% | -6.4 | 175.3 | 2.1 | 2.1 | 6.0 | - | 4.3 |

| BALLY’S INTRALOT S.A. | 1.2 | 1.4 | 15% | 11.3 | 2,200.3 | 1.4 | 1.4 | 16.6 | - | - |