The Greek economy is entering the second half of 2026 with a picture that leaves no room for either triumphalism or doomsday predictions. International agencies, organizations, and the Bank of Greece continue to describe an economy that is outperforming the Eurozone, is driven by investment, maintains fiscal credibility, and is seeing its public debt decline.

At the same time, however, these same reports show that the environment has become more challenging. The energy shock from the Middle East, persistent inflation, the high current account deficit, and dependence on imported investment inflows are creating a new web of risks. The key positive sign is that Greece continues to grow faster than the Eurozone.

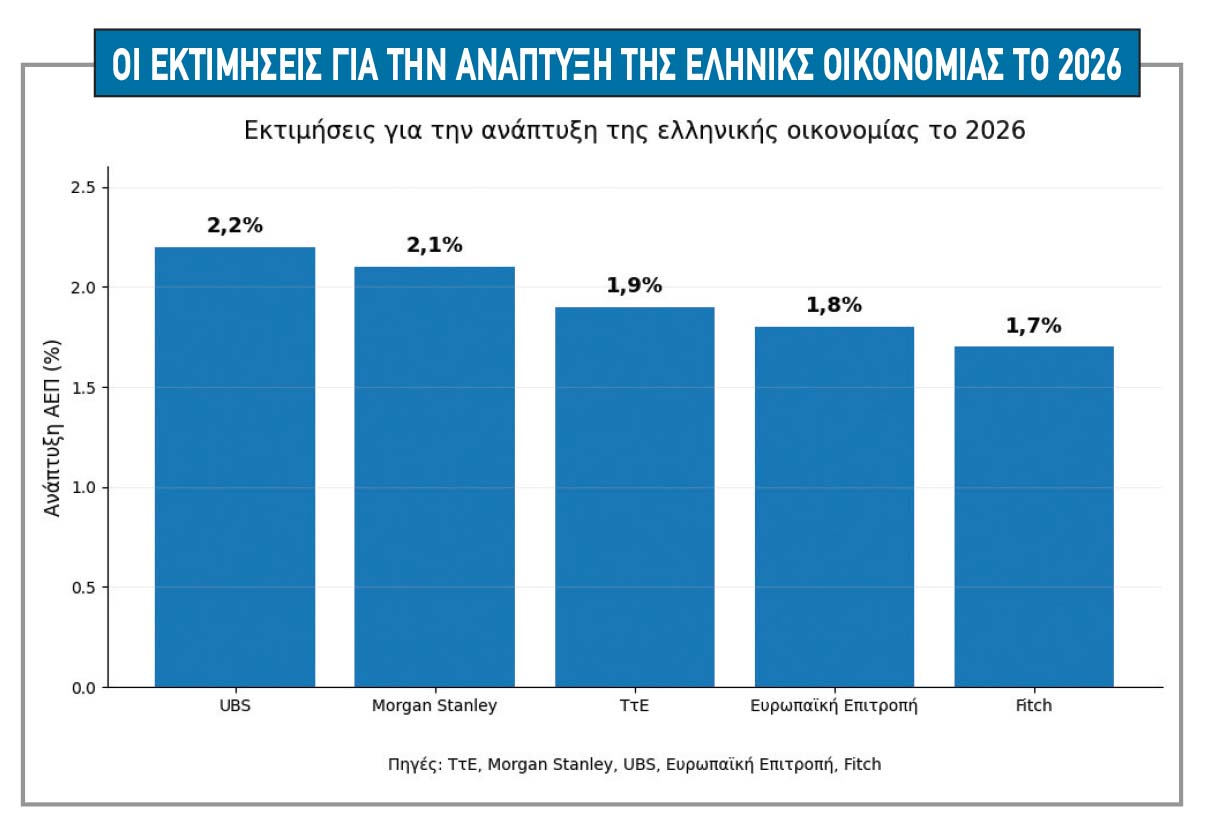

The Bank of Greece, in its most recent notes on the Greek economy, notes that GDP grew by 2.1% in 2025, compared to 1.4% in the Eurozone. Growth was driven by investment, private consumption, and net exports. For 2026, the Bank of Greece forecasts a growth rate of 1.9% and for the period 2027–2028 a rate of 2%, meaning that Greece will continue to outperform the Eurozone.

The role of tourism

This picture is not insignificant, especially in an international environment where energy, geopolitical risks, and market uncertainty are putting pressure on most European economies. Tourism holds a special place in this picture, remaining one of the main pillars of the Greek economy. Investment firms view it as a resilient pillar of growth, as it supports service revenues, employment, consumption, and liquidity across much of the region.

Greece continues to benefit from the shift in international demand toward higher-quality and more expensive destinations, while the extension of the tourist season supports GDP and tax revenues. However, there are downsides here as well. Heavy reliance on tourism leaves the economy vulnerable to geopolitical tensions, rising transportation costs, climate risks, and pressure on infrastructure.

In other words, tourism remains a strong asset, but it is not enough on its own to address the deeper challenge, which is increasing productivity and strengthening the productive base.

Analysts’ assessments

Morgan Stanley’s analysis suggests that Greece’s outperformance narrative is not yet exhausted. The firm forecasts growth of 2.1% in 2026 and 2% in 2027, driven primarily by domestic demand. Of particular importance is its assessment that the risks from the expiration of the Recovery Fund are limited, as investments do not automatically stop when disbursements end. There is a time lag between European funding and the actual implementation of projects, while private investment, credit expansion, and improvements in the investment climate maintain momentum.

UBS also remains positive, but more cautious. In its latest report, the Swiss firm lowered its forecast for Greek GDP by 20 basis points to 2.2% for 2026, acknowledging that higher energy and transportation costs are limiting the safety margins. Nevertheless, UBS maintains its core assessment that Greece rests on three resilient pillars: tourism, investments linked to European funds, and fiscal stability.

In its own scenario, private consumption slows, but investment remains the key driver for 2026. The European Commission appears more conservative. In its spring forecasts, it projects Greece’s growth to slow to 1.8% in 2026 and 1.6% in 2027. Despite the slowdown, the country continues to outperform the Eurozone average, which is under greater pressure from the energy shock.

The European Commission places particular emphasis on the fiscal outlook, as the general government balance is projected to show a surplus of 1.7% of GDP in 2025, higher than the previous forecast. For 2026, it expects a surplus of 0.8% and for 2027 a surplus of 0.6%, despite support measures, tax cuts, increases in wages and pensions, and the rise in defense spending. In this regard, rating agencies see the country’s greatest strength.

In its updated assessment in May, Fitch forecasts growth of 1.7% in 2026 and 1.9% in 2027, with inflation at 3.1% in 2026 and 2.4% the following year. The most significant observation, however, concerns fiscal credibility. The agency notes that Greece achieved surpluses of over 1% of GDP in 2024 and 2025, supported by improved tax compliance and spending controls.

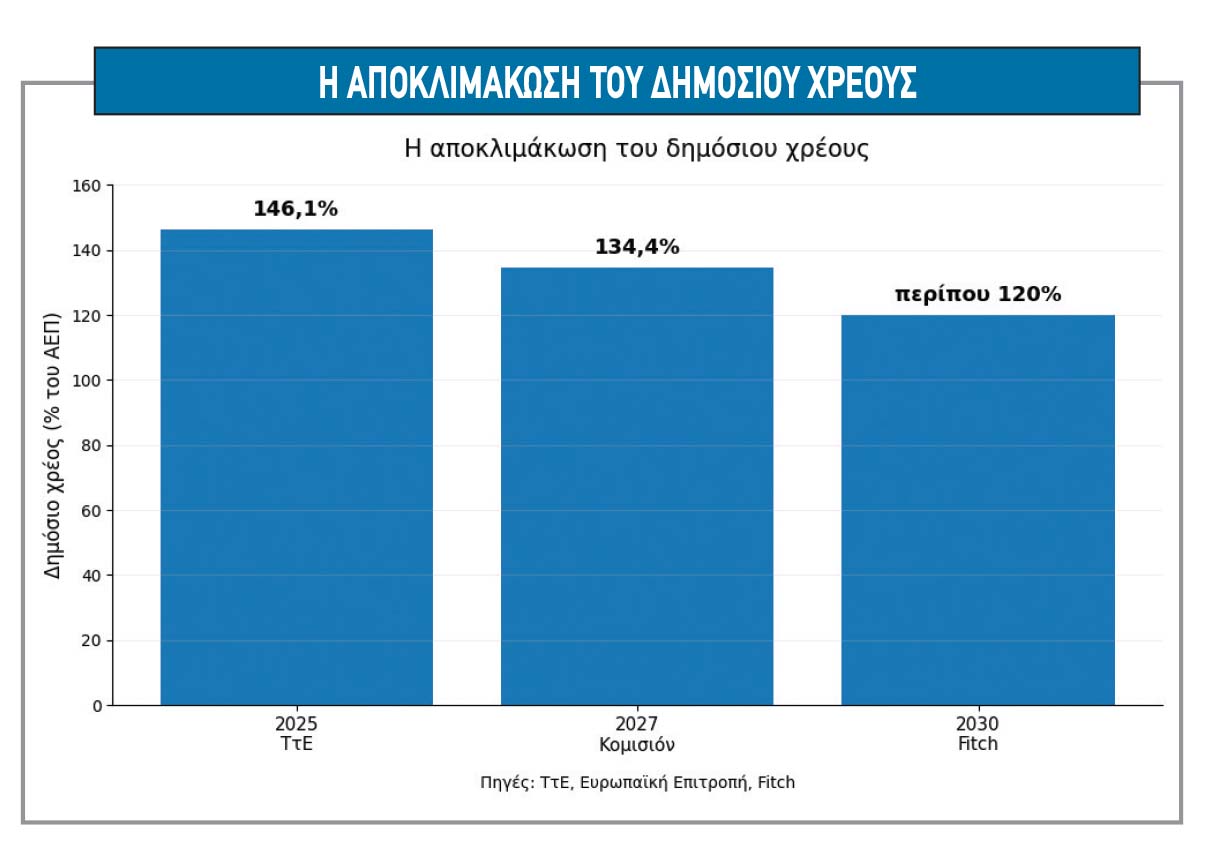

For 2026, it forecasts a surplus of 0.8% and for 2027, 0.7%, while it estimates that public debt could fall to around 120% of GDP by 2030, down from 146% in 2025. Signals from the debt This is where one of the clearest positive signals lies. Greece remains a country with very high debt, but the trend is downward and the debt structure continues to provide protection.

The European Commission estimates that the debt-to-GDP ratio will fall to 134.4% by 2027, while the Bank of Greece reports that in 2025 the debt-to-GDP ratio fell by 8 percentage points to 146.1%, thanks to the high primary surplus, early repayments, and the positive spread between interest rates and the growth rate.

This de-escalation is the key argument that keeps the door open for future upgrades. The second positive signal comes from the banks and the markets. The Bank of Greece, in its May Financial Stability Report, notes that Greek banks further strengthened their fundamentals in 2025.

The quality of the loan portfolio improved, non-performing loans fell to 3.3% of total loans, liquidity remains high, and all major banks are now rated investment grade. Fitch acknowledges the same trend, noting that banks have a stronger capital base, stable funding through deposits, and have largely completed the restructuring of their portfolios. However, the challenges are not insignificant.

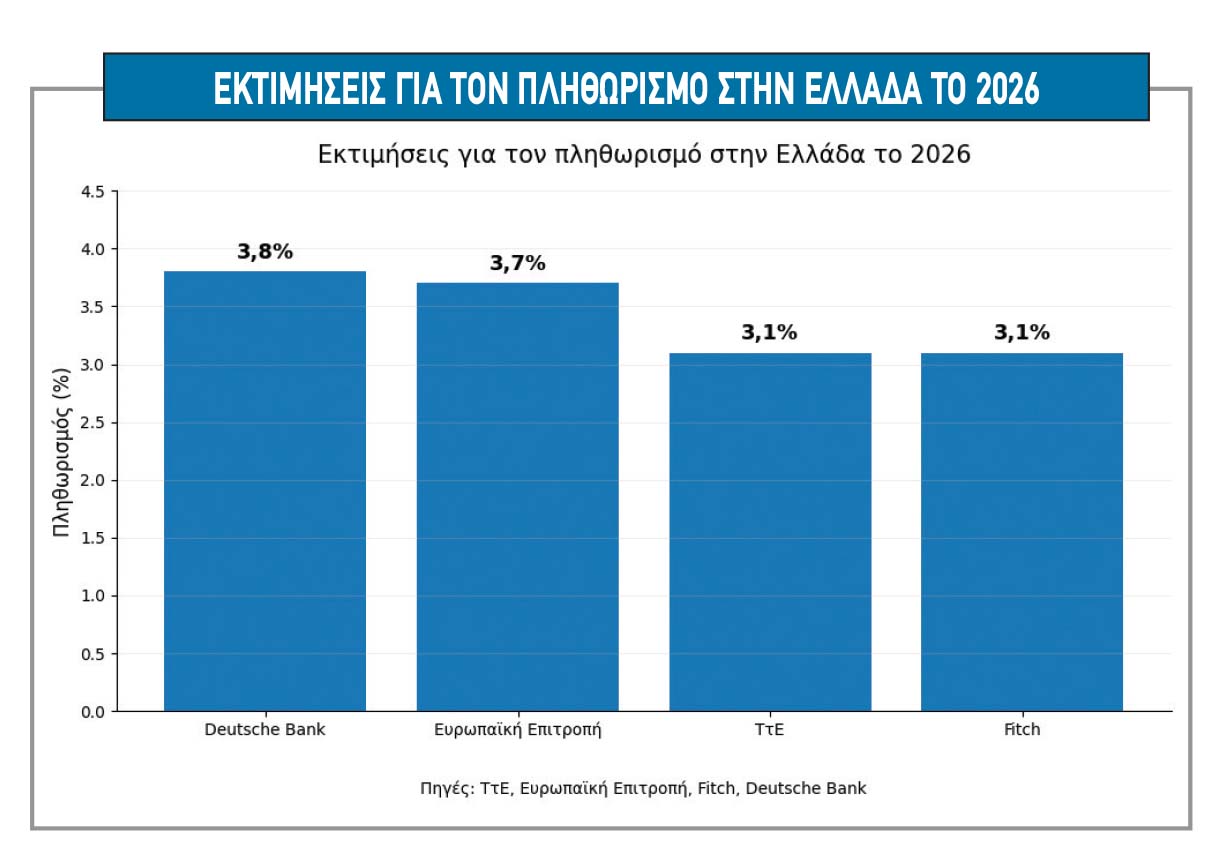

The first and most immediate concern is inflation. The Bank of Greece estimates that inflation will remain high at 3.1% in 2026, as energy and food prices drive up costs, while service inflation remains stubbornly high. The European Commission is even more pessimistic, forecasting inflation to rise to 3.7% in 2026 and fall to 2.4% in 2027.

Deutsche Bank is moving in the same direction, forecasting 3.8% inflation in Greece in 2026, higher than the Eurozone average. This means that growth may continue, but at a higher cost to households and with less room for easing fiscal policy. The second concern relates to the external balance.

Fitch notes that the current account deficit remains high and could widen again due to energy prices. Deutsche Bank is even more blunt, forecasting a deficit of 6.5% of GDP in 2026 and 6% in 2027.

The Bank of Greece, in its first-quarter data, reports a widening of the current account deficit to €7 billion despite an improvement in the goods and services balance. The problem is not merely cyclical. It is linked to low domestic savings, the import dependence of investments, and the fact that increased demand often translates into more imports. The third concern is the quality of growth following the Recovery Fund.

Most agencies do not foresee a sharp gap in 2027, but the transition will be critical. The question is not only whether investments will continue, but whether productivity will increase, whether the export base will expand, and whether investments will translate into a permanent increase in potential GDP. The Bank of Greece notes that the risks to growth forecasts are mainly downside and are linked to the further escalation of the war in the Middle East, the rise of protectionism, the more persistent trend of inflation, and unpredictable climate phenomena.

The Greek economy, therefore, has more positives than it did a few years ago. It has growth above the Eurozone average, investment momentum, a strong tourism sector, stronger banks, fiscal surpluses, and rapid debt reduction. However, it cannot afford to ignore the imbalances.

Inflation is eroding incomes, the current account deficit remains deep, energy uncertainty is testing resilience, and turning investment into a driver of productivity is not an automatic process. The year 2026 points to an economy that has gained confidence, but is now also called upon to prove that its strong performance can be sustained and is not merely the result of a favorable post-memorandum economic climate.