Despite the strong rally that has taken place in the Greek market, the valuations of many FTSE 25-listed companies still trade at a significant discount to their international peers, leaving room for further upward revision of their multiples.

The picture emerging from Beta Securities’ comparative valuation (based on closing prices as of June 11 and estimates for 2026) shows that banks remain the biggest “bet” on the Greek stock market, while interesting divergences are also observed in sectors such as telecommunications, refineries, building materials, retail, and industry. In contrast, some companies are already trading at a premium relative to their international competitors, reflecting higher growth expectations.

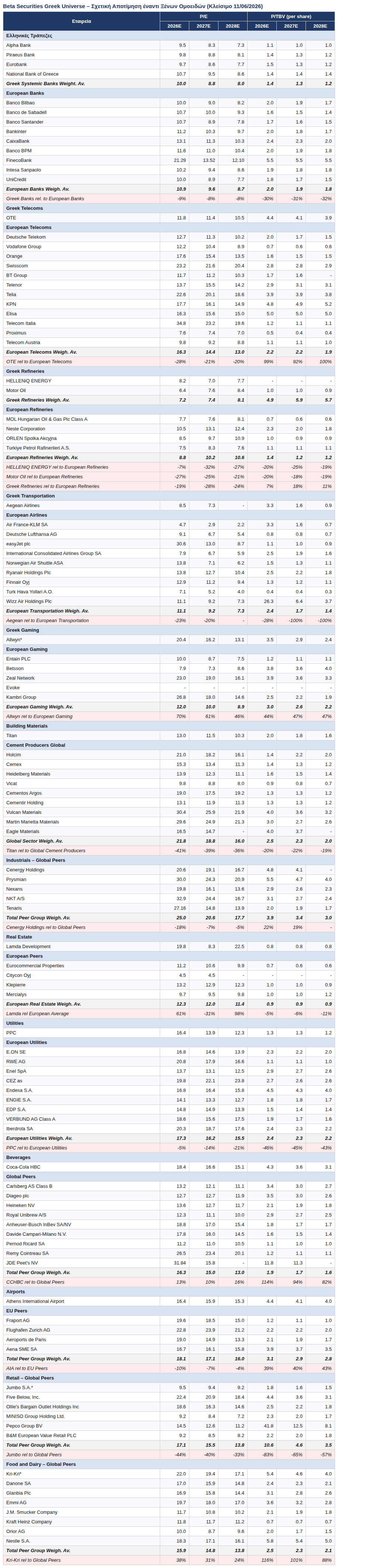

Banks remain cheaper than in Europe

The most striking example remains the banking sector. Despite strong returns since the start of the year, the four systemic banks are trading on average at a P/TBV ratio of 1.4 times for 2026, compared to 2.0 times for European banks, representing a discount of approximately 30%.

The largest deviation is seen in Alpha Bank, which trades at a 46% discount relative to its European peers in terms of P/TBV. It is followed by Piraeus Bank with a 30% discount, Eurobank with 26%, and National Bank of Greece with 25%.

It is worth noting that Greek banks also have single-digit or marginally double-digit P/E ratios for 2026. Alpha Bank is trading at 9.5 times estimated earnings, Piraeus Bank at 9.8 times, Eurobank at 9.7 times, and National Bank of Greece at 10.7 times.

Despite the significant improvement in their profitability and capital, the market continues to value the sector at significantly lower multiples than European peers, although in terms of P/E the gap has now narrowed significantly, with the sector’s average discount limited to 9%.

OTE: A value story in telecommunications—with one caveat

Among non-financial companies, OTE stands out as one of the most attractive cases in terms of profitability. The stock is trading at a P/E ratio of 11.8x for 2026, compared to 16.3x for European telecommunications groups, which corresponds to a 28% discount.

At the same time, the dividend yield for 2026 is estimated at 4.67%, higher than the European industry average, while the stock has already risen nearly 15% since the start of the year.

The picture, however, is not one-dimensional: in terms of book value, OTE is trading at a P/BV of 4.4 times, nearly double the European average. This divergence partly reflects the group’s higher return on equity and share buybacks, but it serves as a reminder that the stock’s value story is based on profitability rather than its book value.

Refineries: Strong returns, but still cheap

The two listed companies in the refining sector continue to trade at attractive valuations. HELLENiQ Energy is trading at a P/E of 8.3x for 2026 and a 7% discount relative to European peers, while Motor Oil trades at a P/E of 6.4x and a 27% discount.

On a weighted basis, the sector trades at a discount of approximately 19% relative to European refineries, despite the fact that the stocks have already delivered an average return of over 25% since the start of the year. At the same time, dividend yields remain particularly attractive, exceeding 5%.

Jumbo: The deepest discount on the board

If the comparison is made strictly in terms of multiples, the largest deviation across the entire FTSE 25 is not found among banks but in Jumbo. The stock is trading at a P/E of just 9.5 times for 2026, which is 44% lower than the average for international discount retailers, while in P/BV terms the discount reaches 83%.

The market, however, has its reasons: the stock has recorded losses of over 18% since the start of the year, as investors are pricing in a slowdown in growth. The high dividend yield, estimated at over 5%, does, however, offer a significant “cushion” as long as the outlook remains uncertain.

Titan and Cenergy lag behind competitors in terms of earnings

Titan is one of the most notable discount cases outside the financial sector. With a P/E ratio of 13 times for 2026, its valuation remains 41% lower than the average for international cement producers, despite the significant improvement in its results in recent years.

Similarly, Cenergy Holdings is trading at a P/E of 20.6 times, approximately 18% below the average for international industrial groups in the sector, although in terms of P/BV, the stock has already moved into a 22% premium. The stock has posted the best performance among large-cap listed companies, rising over 63% since the start of the year—an indication that the market has begun, albeit belatedly, to reflect its growth momentum.

Aegean: High dividend, low P/E ratio

Aegean Airlines has a P/E ratio of just 8.5 times for 2026, a level that represents a 23% discount compared to European airlines.

At the same time, it offers an estimated dividend yield of 7.5%, more than four times the European industry average. However, the stock remains under pressure this year, posting losses of approximately 15%, due to the surge in oil prices amid ongoing tensions in the Persian Gulf.

On the value side of the board, we find PPC, which trades at a small 5% discount in P/E terms but a 46% discount in P/BV terms relative to European utilities, as well as Athens International Airport, with a 10% discount in P/E terms – although in its case, the comparison in terms of book value shows a premium, due to the high returns on capital from the concession.

Stocks trading at a premium

On the other hand are companies for which the market is already pricing in higher growth rates. Allwyn has the highest premium, trading at a P/E of 20.4 times, approximately 70% higher than the European average for the gaming sector—based on estimates by Beta Securities. It is noteworthy that the premium is maintained despite the stock’s losses of over 20% since the beginning of the year.

Lamda Development also trades at a premium, with a P/E of 19.9 times and a 61% deviation relative to European real estate companies, although in P/BV terms the stock continues to trade at a small 5% discount—the most meaningful metric for a real estate development company.

A similar picture is seen with Coca-Cola HBC, which trades at a 13% premium in P/E terms and with a P/BV 114% higher than the average for international beverage companies, as well as Kri Kri, which is valued at a 38% premium in terms of P/E and 116% in terms of P/BV, reflecting high expectations for the future growth of its earnings.

Data source: Beta Securities, “Greek Universe Relative Valuation vs. Foreign Peers,” closing prices as of June 11, 2026. For Allwyn, Jumbo, and Kri Kri, the estimates are from Beta Securities.