The question on everyone’s mind today as they look at the Greek stock market following the rally of recent years is simple: “Have I missed the boat?”

The answer provided by Beta Securities’ estimates for the 2026–2028 period is more interesting than a simple yes or no: for a large portion of large-cap stocks, the market is becoming cheap again—not through a price correction, but through earnings growth.

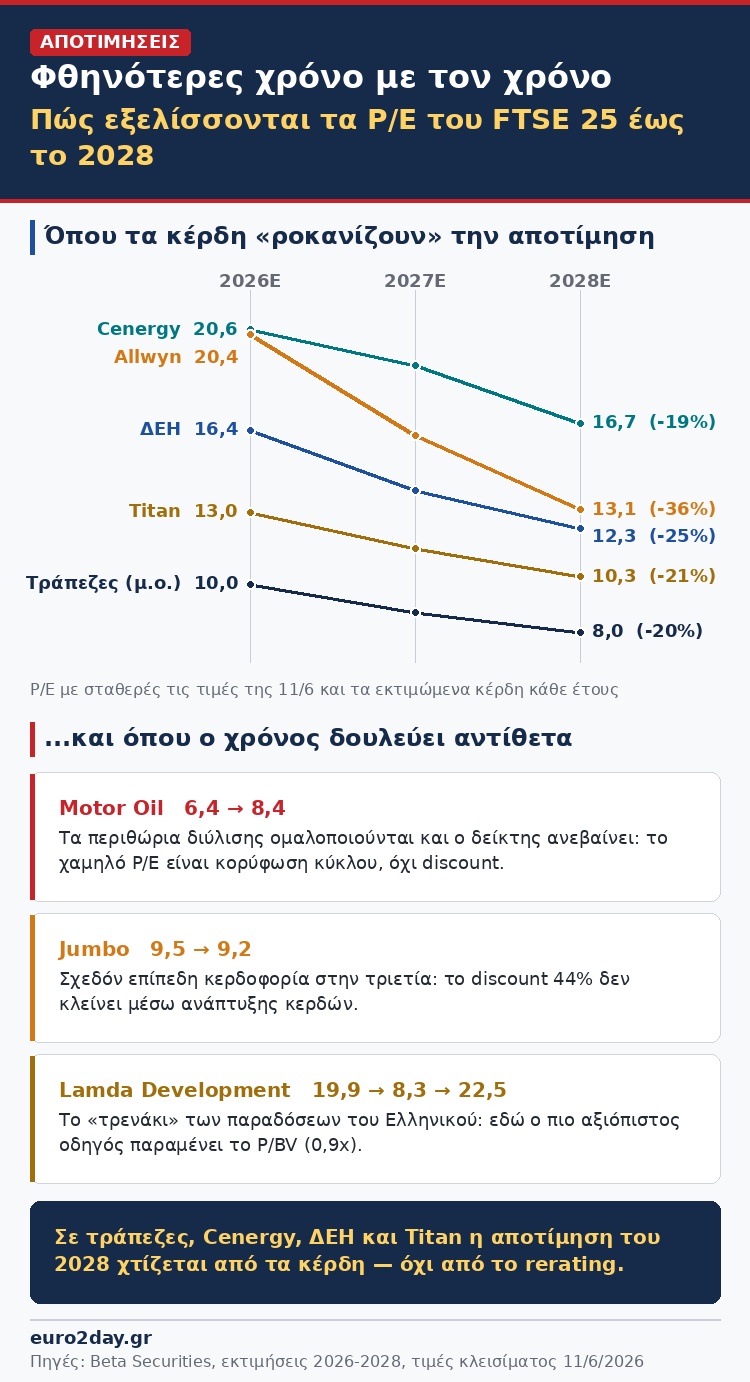

With current prices held constant (as of the close on June 11), the price-to-earnings ratios of several FTSE 25 constituents are set to decline significantly by 2028. In other words, an investor buying today is paying not only for this year’s earnings but for an earnings trajectory that, if confirmed, will “erode” the valuation on its own. There are, however, exceptions—sectors where time works in the opposite direction.

Banks: 8 out of 10 times, with rising dividends

The clearest example is, once again, the four systemic banks. The sector’s weighted P/E ratio declines from 10 times 2026 earnings to 8.8 times in 2027 and 8 times in 2028, as earnings per share continue to rise throughout the three-year period.

Alpha Bank shows the largest decline, from 9.5 to 7.3 times, with earnings per share estimated to rise from €0.42 this year to €0.50 in 2028. Eurobank moves from 9.7 to 7.7 times, Piraeus from 9.8 to 8.1, and National Bank of Greece from 10.7 to 8.6.

The same picture holds true in terms of tangible book value: the sector is declining from 1.4 times in 2026 to 1.2 times in 2028, as capital is being built up faster than it is being distributed—and this despite the fact that the estimated dividend yield is rising from 4.5% to 6.5% over the same period.

It is worth noting, however, that the same phenomenon is occurring in Europe: the average European banking P/E ratio is falling from 10.9 to 8.7 times, so the relative discount of the Greek sector in terms of earnings remains steady at around 8–9%.

Allwyn: The premium that disappears if the numbers “come in”

The most impressive P/E ratio “journey” belongs to Allwyn. The stock is currently trading at a P/E of 20.4 times for 2026—a premium of approximately 70% relative to the European gaming sector. However, based on Beta’s estimates, the ratio falls to 16.2 times in 2027 and to 13.1 times in 2028.

In practical terms, the current valuation discounts a near-doubling of profitability over the next two years. If the company does indeed deliver the projected figures, an investor in 2026 will have purchased a company with a dividend yield of 7.6% at 13 times its 2028 earnings.

Cenergy: Growth that justifies the multiple

A similar logic, with lower execution risk due to contracted backlog, applies to Cenergy Holdings. The P/E ratio declines from 20.6 times this year to 16.7 in 2028, with the EV/EBITDA ratio falling from 13.1 to 10.7 times.

Despite a +63% gain since the start of the year—the best performance among large-cap stocks—the stock is valued more cheaply by 2028 than its international competitors are today, as Prysmian and NKT are trading at 30 and 33 times this year’s earnings, respectively.

PPC and Titan: The Quiet Decline

In the same category, with less dramatic but steady steps, are PPC and Titan. DEI sees its P/E ratio falling from 16.4 to 12.3 times by 2028, with the dividend yield rising from 3.5% to 5.3% — although here the trade-off is increased leverage due to the investment program. Titan moves from 13 to 10.3 times, maintaining a discount of approximately 36–41% relative to international cement companies throughout the forecast horizon.

The other side

However, a three-year analysis also reveals cases where the current “cheapness” marks the peak of a cycle rather than an opportunity.

The most telling example is refineries. Motor Oil, with a P/E of just 6.4 times this year, sees the ratio rise to 7.6 times in 2027 and 8.4 in 2028—not because the stock is becoming more expensive, but because refining margins are normalizing and profits are declining.

HELLENiQ Energy shows a more complex trajectory (8.2 times this year, 7 in 2027, 7.7 in 2028). The low P/E of refineries is, in part, the price paid for cyclicality—a classic trap for anyone reading the metric statically.

Jumbo, for its part, remains virtually flat: from 9.5 to 9.2 times over the entire three-year period. The deep 44% discount relative to international retailers is not driven by earnings growth—estimates point to essentially flat profitability—and this explains why the market prices it so cautiously despite the balance sheet showing a cash surplus.

Lamda Development deserves special mention, where the P/E ratio is on a rollercoaster ride: 19.9 times this year, plummeting to 8.3 in 2027 as revenue from the Hellenikon project is recognized, and rebounding to 22.5 times in 2028. This is the best reminder that for real estate development companies, a single-year P/E ratio tells us very little—here, book value (P/BV 0.9, at a discount to European peers) remains the most reliable guide.