Greek systemic banks remain among the most attractive investment opportunities in Europe, according to a new analysis by Optima Bank, which is raising its price targets and maintaining a positive outlook for the sector, highlighting the combination of strong and sustainable profitability, increasing capital distributions, and “demanding” valuations relative to their Southern European peers.

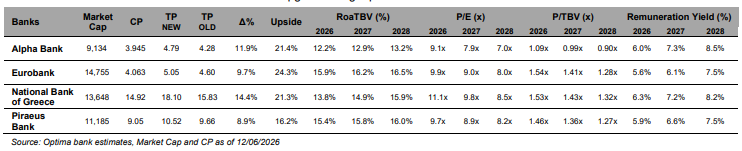

Specifically, the brokerage maintains “buy” recommendations for all four systemic banks, while setting a new target of €4.79 for Alpha Bank from €4.28, €5.05 for Eurobank from €4.60, €18.10 for National Bank of Greece from €15.83, and €10.52 for Piraeus Bank from €9.66.

The firm estimates that Greek banks can deliver medium-term returns in the range of 13%–16.5% on RoTE through 2028, with an average annual increase in earnings per share of approximately 10%. This growth is supported by healthy credit expansion, with corporate loans and investment projects serving as the main driver, as well as an increasing contribution from fees.

Optima notes that net interest income is now driven more by volumes than by margins, which are stabilizing. At the same time, commission income is growing at high single-digit rates, supported by bancassurance, asset management services, and fee-related income from lending.

Operational efficiency is also a key factor, with a cost-to-income (C/I) ratio near 35%-36%, as well as low risk costs at 40-50 basis points—factors that support sustainable profitability and double-digit EPS growth.

In terms of capital, banks report CET1 ratios significantly higher than regulatory requirements, creating room for increased distributions. The trend is shifting toward higher cash dividends, with total shareholder returns expected to range from 6% to 9% over the next three years.

In terms of valuations, Greek banks continue to trade at a discount relative to Southern European banks, both in terms of P/E (9x–11x for 2026) and P/TBV (1.09x–1.54x), a factor that Optima considers a key catalyst for further re-rating.

Other positive catalysts include potential inclusion in developed market indices (STOXX, FTSE, MSCI), continued strong credit demand from the corporate sector, and the possibility of higher interest rates for a longer period. On the other hand, geopolitical tensions and the election cycle remain sources of volatility, though they do not undermine the fundamental outlook.