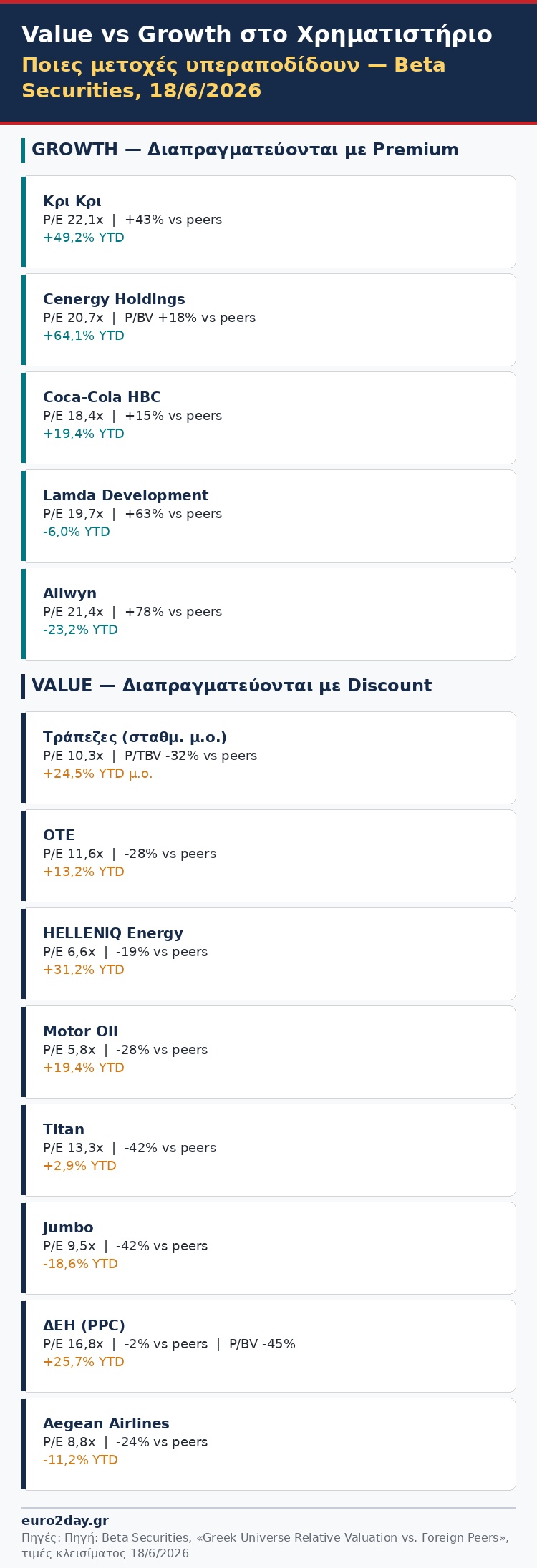

The Greek stock market is no longer moving at a single pace. Data from Beta Securities, based on closing prices as of June 18, clearly show a growing divide: on the one hand, stocks trading at a premium to their foreign counterparts and continuing to outperform; on the other, stocks that remain cheap in terms of multiples but fail to convince the market.

In the first category, Kri Kri and Coca-Cola HBC stand out.

Kri Kri is trading at a P/E of 22.1 times for 2026—a 43% premium over its international peers—and has already posted a 49.2% gain since the start of the year. Coca-Cola HBC, with a 15% premium in P/E and an 118% premium in P/BV relative to its global competitors, is up 19.4% this year.

Cenergy Holdings is a special case. With a P/E ratio of 20.7 times and a 19% discount compared to its international competitors, the stock is not expensive on an earnings basis—however, the market values it at an 18% premium to book value, discounting accelerating profitability in the coming years. The 64.1% gain so far this year confirms this assessment.

In contrast, banks are the most typical example of stocks that remain undervalued yet deliver returns. With a weighted P/TBV of just 1.5 times compared to 2.2 times for European competitors—a 32% discount—and a P/E of 10.3 times versus 11.7 times, the sector remains clearly cheaper than in Europe.

Nevertheless, returns are impressive: Piraeus Bank is up 38.1% so far this year, Eurobank 25.3%, National Bank of Greece 18.6%, and Alpha Bank 15.1%. The sector demonstrates that a valuation discount is not an obstacle to strong stock market performance when accompanied by improving fundamentals.

OTE presents a similar picture—a 28% P/E discount—yet has gained 13.2% so far this year. Refineries, with a weighted P/E discount of 24%, are posting a weighted return of 24.7%. PPC, with a P/E discount of just 2% but a P/BV discount of 45%, is up 25.7%.

In conclusion, in 2026, the Greek market is rewarding both “value” stocks and those characterized as growth stocks—provided they are backed by reliable earnings prospects. Growth stocks with premium valuations rise only when fundamentals justify the price—as seen with Kri Kri and Cenergy.

Similarly, value stocks with strong business momentum, such as Piraeus Bank, demonstrate that a discount is not, in and of itself, an obstacle to high returns. What is penalized is stagnation—as illustrated by Jumbo, which is down 18.6% despite an attractive P/E ratio of 9.5 times.