After nearly seven years of New Democracy rule, GDP has shown an impressive increase, cumulatively by about 34% at current prices through the end of 2025. However, this is only one side of the coin. A side that seems almost… magical, when viewed in light of certain other, very important data.

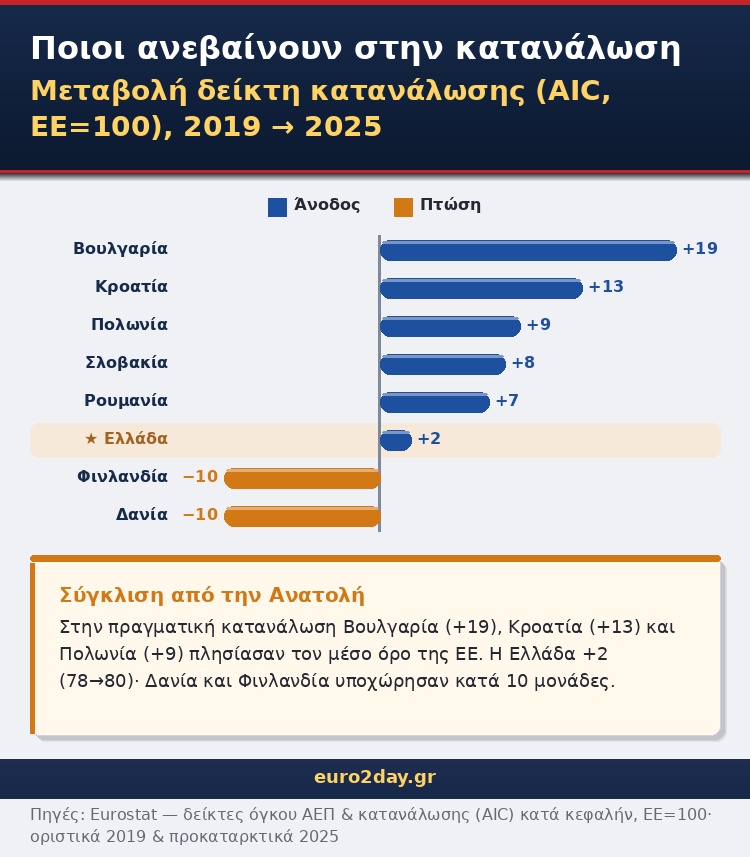

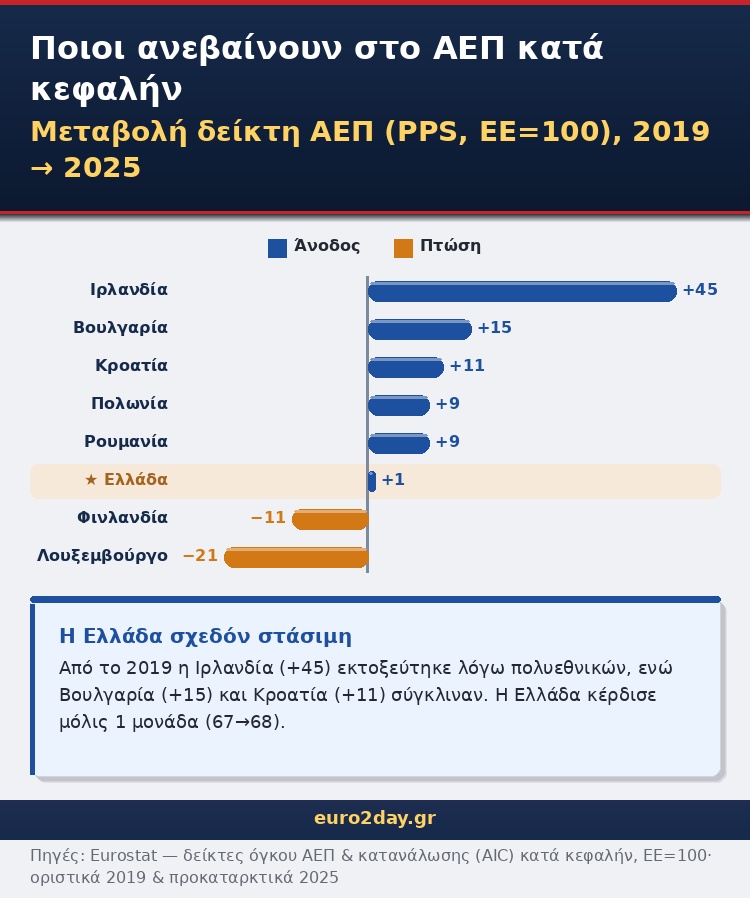

Throughout this period, Greece has shown only a marginal improvement in convergence with Europe. Real per capita consumption has risen only slightly, from 78% to 80% of the EU average, while per capita GDP has remained virtually stagnant, rising from 67% to 68% of the EU average in terms of purchasing power (Purchasing Power Standard)..

This is the appropriate methodological approach to account for the impact of differing prices from country to country. In other words, Eurostat does not simply compare how many euros the average resident of each country produces or consumes, but rather what those euros can buy in each economy.

We can see, then, that household consumption stands at around 80% of the European average, while per capita wealth production remains stable at around two-thirds of the European average.

There is one more detail that makes the picture even bleaker: in 2024, Greece stood at 69% of the EU average in terms of per capita GDP. In 2025, it fell to 68% and is now at the lowest level in the Union, alongside Bulgaria.

In any case, the overall picture is clear. We have not achieved meaningful convergence with Europe, either in terms of production or consumption. On the contrary, we have “stalled”!

What Causes the Greek Gap

However, the divergence between the two indicators (per capita GDP and consumption) also reveals something else critical: daily household consumption remains higher than the economy’s productive output.

Unfortunately, this does not mean that Greeks live comfortably. Nor does it mean that the country has no problems with inflation, wages, or disposable income. It simply means that Greece’s relative position in terms of consumption is significantly better than its relative position in terms of production.

And this is the crux of the matter. The country’s problem is not merely one of income or consumption. It is, first and foremost, a problem of productivity and low per capita output.

Why is this the case?

First, because the Greek economy remains heavily consumption-oriented. Second, because the real per capita consumption index includes services used by households, even if they do not pay for them directly, such as certain health and education services. Third, because domestic demand (as well as production) relies heavily on imports.

Simply put, we could say that we continue to “consume more than we produce,” to use a well-worn phrase from the past.

However, this is not because households are “to blame” or because citizens are living carefree beyond their means, but because the economy does not generate enough domestic value to sustain society’s level of consumption in a sustainable manner.

The real question, therefore, is not why Greece consumes at 80% of the European average, but why it produces at only 68% of the average of the other countries.

So why is GDP rising?

This is where the major pitfall of the public debate lies. Indeed, the Greek economy has been growing faster than many European economies in recent years.

However, nominal GDP grows both from an increase in real output and from rising prices. Inflation inflates the figures in euros. It helps, for example, to reduce the debt-to-GDP ratio. However, this does not automatically mean that the country is producing much more real wealth per capita.

In real terms—that is, adjusting for price changes—GDP growth between 2019 and 2025, according to the series, is approximately 11%. (Real Gross Domestic Product (Euro/ECU Series) for Greece, FRED/St. Louis Fed).

The second point is that Eurostat’s indices are comparative. The EU is set at 100 each year. For Greece to converge, it is not enough simply to grow. It must grow consistently faster than the European average, and in such a way as to increase the value it produces per capita and per hour worked.

The third point is the composition of growth. Tourism, consumption, construction, and funds from the Recovery Fund can generate strong growth rates.

However, they will not strengthen the country’s position in the European production hierarchy unless they are accompanied by higher added value, investments in technology, larger and more outward-looking businesses, higher skills, and more efficient institutions, e.g., in terms of bureaucracy and the administration of justice.

Productivity: The Big Issue and the Solutions

Greece isn’t lagging behind because people aren’t working. In fact, the opposite is true. Greeks work the most actual weekly hours in the EU—39.6 hours per week, compared to the European average of 35.9.

And yet, GDP per capita is the lowest in the Union. This clearly highlights the core of the problem: excessively low productivity—a point that the European Commission has also noted, pointing out that the country’s productivity stands at just 54.6% of the EU average. It is impossible to close this gap by simply working longer hours; therefore, we must produce more efficiently.

The causes are, more or less, well known: small businesses that struggle to grow, low investment, limited technology diffusion, skills mismatches, bureaucracy, a slow justice system, and a weak link between production and innovation.

Furthermore, there is a high concentration of GDP in sectors with low productivity and low participation by sectors that could dramatically increase it, such as industry and manufacturing.

Ultimately, the entire debate over wages hinges on this imbalance. The government frequently speaks of the need to raise wages and has pushed in various ways for higher pay.

However, for wages to rise in a sustainable manner, productivity and domestic production must also increase. Otherwise, this will lead to a rise in imports and a loss of competitiveness.

Greece appears to have left the worst years of the crisis behind; there is no question about that. However, a comparison with Europe shows that this improvement has not translated into meaningful convergence.

The next phase will therefore not be determined by whether GDP posts another strong figure—which, in any case, is projected to be lower in the coming years compared to previous ones.

It will be determined by whether Greece can generate more value with the same or less labor. For this to happen, it requires an appropriate development framework from the government, a focus on industry, manufacturing, and innovation, as well as significant related investments from the business community.

Without these, we will continue to have lofty goals for growth, but poor results in terms of convergence with Europe and the standard of living of our society.