The decline in gasoline prices will be slow and gradual despite the drop in oil prices to $75, the improved sentiment in international energy markets, and expectations of a rapid reduction in transportation costs for households and businesses.

This is the outlook provided by fuel market sources regarding price trends; despite the sharp drop in the first few days following the U.S.-Iran agreement, they estimate that the decline will continue but at a more moderate pace.

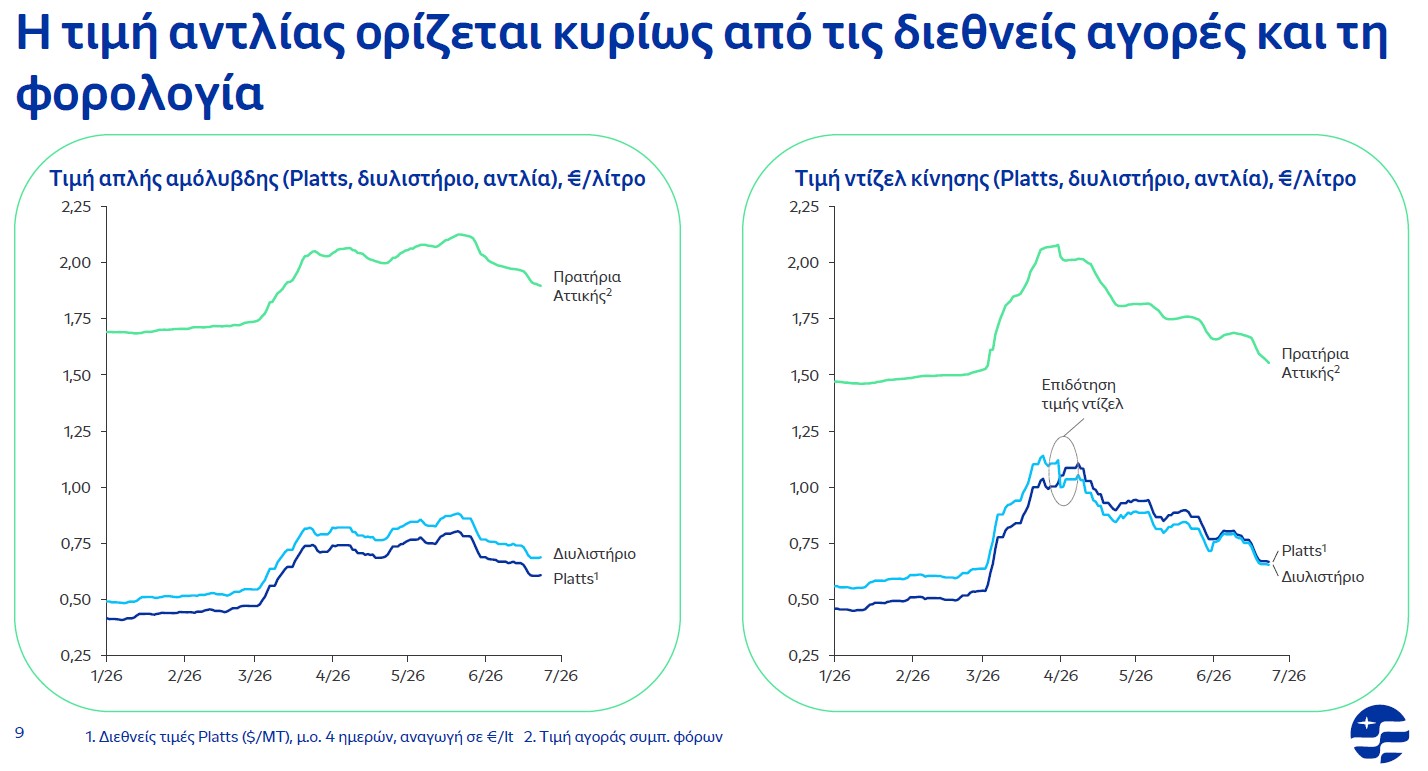

Since late May, when it became apparent that an agreement in the Persian Gulf was imminent, the price of gasoline has fallen from 2.13 euros to 1.92 euros nationwide today—a drop of more than 15 cents. However, on many islands, such as those in the Cyclades and the Dodecanese, the price exceeds 2 euros.

Diesel, for its part, has fallen from a high of 2.12 euros per liter to 1.62 euros. The drop amounts to 38 whole cents after subtracting the subsidy portion; however, the sharp plunge seen in the first few days appears to have slowed.

When asked about the reasons for the slower pace of price declines in recent days, sources at Helleniq Energy cite a number of factors.

“This is both because demand for fuel is high in the summer—as reflected in international prices for products such as diesel and jet fuel—and due to the unique characteristics of the Greek market,” commented group executives, alluding to the country’s geography, with its many islands and numerous small gas stations.

Other market sources have reached the same conclusion, “seeing” resistance to a rapid decline as we enter the height of summer and tourist demand for fuel keeps international prices for unleaded and diesel relatively high.

This picture is reflected in Platts’ prices for gasoline and diesel, which on Wednesday stood at $903.75 and $895.75 per metric ton, respectively; while they are trending downward, the decline is less steep than in previous days.

According to the same sources, the Greek market model itself is contributing to this slow decline, as at least 35% of the market is controlled by many small companies, there are many remote areas where supplies are not delivered daily, and quite a few gas stations still have stocks purchased at higher prices.

“In island and remote areas with few and small gas stations, it is to be expected that there will be a lag in how quickly the drop in international prices is passed on at the pump,” our sources explain, "in contrast to the speed with which prices rise when crude oil and petroleum products increase."

Consumption Holds Steady

It is interesting to note, however, that although gasoline prices remain consistently above 1.90 euros per liter, consumption is not declining. High prices have not led to a real decline in demand; in other words, the phenomenon of “demand destruction” has not materialized in the Greek market (or elsewhere, for that matter).

It is telling that despite the surge in prices over the past period, from March through June, the decline in consumption did not exceed 3%, according to sources at Helleniq Energy speaking on the sidelines of the group’s annual General Meeting, where management presented the outline of its strategy for the period 2026–2030.

Under the group’s new “Vision 2030+” plan, petroleum products, investments in refining, crude oil trading, and fuel marketing will remain the mainstays; however, a series of game-changers are also being added, ranging from the further development of renewable energy and batteries to opportunities and potential revenue from the hydrocarbons sector.

At the same time, the group is working to strengthen its position in the power generation sector through Enerwave, where it is examining a range of scenarios for the investment project, amounting to approximately 450 million euros, involving the construction of a new 800 MW gas-fired power plant in Thessaloniki. “We are running alternative scenarios for a smaller plant, under 800 MW. A project of this size lacks flexibility. We are considering plants of 200 MW and above,” say sources within the group.

Another major project that, while still on the table, has not yet led to a final investment decision by the group is the Thessaloniki FSRU project.

“Investing 300–500 million euros, only to see the balance of the natural gas market shift a few months later, would not be prudent,” says a source at Helleniq Energy regarding the plan for the floating terminal in Thermaikos.

And it is interesting to note that one of the reasons the group has not yet made its decisions is our interlocutor’s view that the issue of Russian gas has not been definitively resolved for Europe.

“If you can tell me that Russian gas is definitively a thing of the past and won’t start flowing again at some point, then I’ll tell you when we’ll build the FSRU,” he says characteristically.