In the world of asset markets, time is not linear. Stock markets operate within two successive time frames and two distinct yet interrelated forces: secular markets and cyclical markets.

The distinction between these two concepts forms the foundation of asset allocation strategy and the understanding of major economic cycles.

Secular and Cyclical Markets

A secular market refers to a long-term trend—either upward (secular bull) or downward/sideways (secular bear)—that typically lasts 10 to 20 years or even longer. The term “secular” derives from the Latin saeculum, meaning a generation or century, implying that this trend extends beyond a single economic cycle and reflects deeper structural forces in the economy.

A cyclical market, by contrast, describes shorter-term fluctuations—typically ranging from a few months to five years—that unfold within a secular trend. A secular bear market, for example, is not a continuous decline, but a sequence of strong cyclical bull rallies and painful cyclical bear corrections, with the general index remaining, in real (inflation-adjusted) terms, bearish or sideways-bearish for a long period of time.

The Factors Determining Secular Trends

The transition from a secular bull market to a secular bear market—or vice versa—is not random. It is determined by the convergence of multiple structural factors:

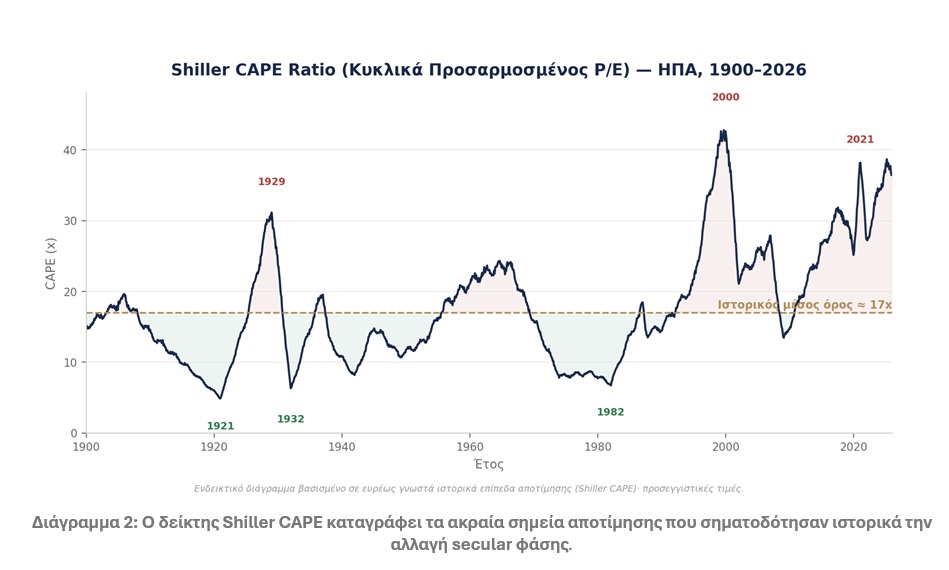

- Valuations: Secular bull markets typically begin at historically low levels of metrics such as the cyclically adjusted P/E (CAPE/Shiller P/E) and end at extreme valuation highs.

- Inflation and interest rates: Price stability favors the expansion of valuation multiples and thus secular bull markets, while high or volatile inflation compresses valuations and favors secular bear markets.

- Demographics: Generations that are numerically large, when they reach the age of saving and investing (e.g., baby boomers in the 1980s and 1990s), inject significant capital into the markets, reinforcing secular upward trends.

- Technological revolutions: New waves of technology (e.g., railroads, electricity, information technology, artificial intelligence) create new sectors of productivity that support long-term profitable growth.

- Monetary and fiscal policy: The stance of central banks, the cost of capital, and the level of public and private debt shape the liquidity environment in which valuations operate.

- Geopolitical environment: Periods of stability and globalization favor the emergence of a secular bull market, while conflicts, trade wars, and problems in energy and supply chains act as impediments.

It is worth noting that many of these factors—technological waves, credit expansion, and demographics—also form the core of the Kondratieff wave theory, which attempts to link 40- to 60-year economic supercycles with the secular phases of capital markets.

The Importance of Recognizing the Secular Market

The distinction between secular and cyclical markets has direct implications for investment strategy. In a secular bull market, the “buy and hold” strategy is generously rewarded, as every decline presents a buying opportunity.

In a secular bear or sideways-trending market, however, the same strategy can lead to one or even two decades of zero real returns at best, making active management, sector rotation, and range trading imperative and far more effective.

Furthermore, recognizing the market’s current phase influences asset allocation: in a secular bull market, growth stocks are favored, while in a secular bear market or a high-inflation environment, real assets—commodities, real estate, precious metals—and value stocks tend to outperform.

The Impact on Society, the Economy, and Assets

Secular trends are not limited to the stock markets; they permeate all aspects of economic and social life. A prolonged secular bull market amplifies the wealth effect: households feel wealthier, consume more, and businesses invest with greater confidence, fueling a virtuous cycle of growth, employment, and tax revenue for the government.

In contrast, a secular bear market is often accompanied by wage stagnation, increased intergenerational inequality in wealth accumulation, low consumer confidence, and political instability, as investors who entered the market at high valuations experience prolonged disappointment.

Historically, such periods have been associated with rising populism, social unrest, and demands for radical policy changes, as observed in both the 1930s and the 1970s.

At the asset level, the phase of the secular cycle determines which asset classes outperform. Long bull markets primarily favor financial assets (stocks, bonds), while secular bear markets or periods of high inflation favor real assets (hard assets), such as real estate, gold, and commodities—a distinction central to any long-term portfolio allocation analysis.

Historical Data from the U.S.

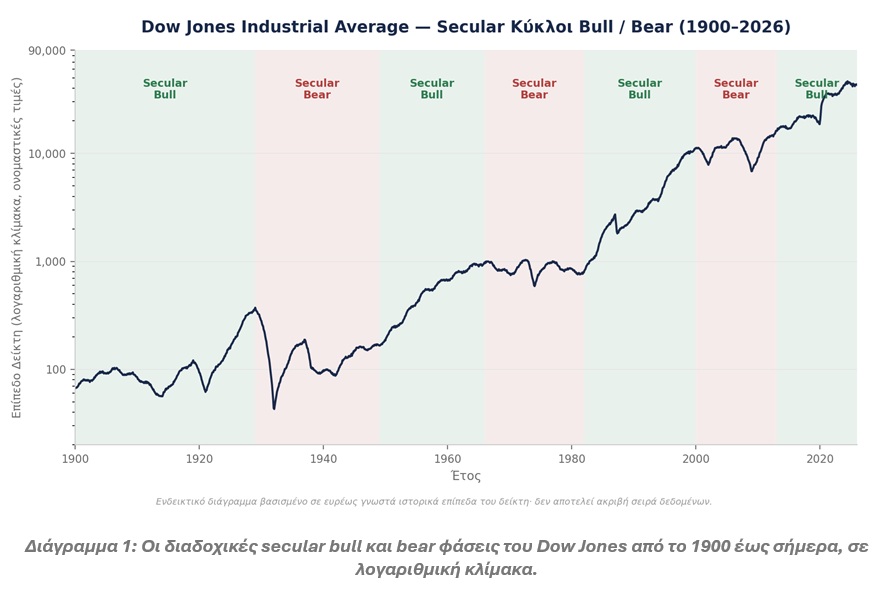

U.S. stock market history provides the most well-documented frame of reference for studying secular cycles, based on the Dow Jones and S&P 500 indices in real terms:

- 1929–1949: Secular bear market, with the 1929 crash and the prolonged deflation/recession of the 1930s keeping valuations very low for two decades.

- 1949–1966: Strong secular bull market, supported by postwar reconstruction, industrial expansion, and the baby boom.

- 1966–1982: Secular bear/sideways market, with high inflation (stagflation), oil crises, and high interest rates keeping the Dow Jones essentially stagnant for 16 years in nominal terms and resulting in significant losses in real terms.

- 1982–2000: One of the strongest secular bull markets in history, driven by the decline in inflation under Volcker, falling interest rates, fiscal reform, and the IT and Internet revolution.

- 2000–2009 (or 2011 according to others, e.g., Morgan Stanley): A secular bear market, marked by the bursting of the dot-com bubble, the 2008 financial crisis, and two major declines of over 50%, with the S&P 500 not returning, in real terms, to levels close to those of 2000 until around 2013.

- 2009–present: A new secular bull market, driven by low interest rates in the post-crisis era, the digital economy, and, more recently, the wave of artificial intelligence, with questions arising from 2025–2026 regarding extreme valuations and the return of inflation.

The study of these cycles is not intended to provide precise timing forecasts—something that is extremely difficult even for highly experienced analysts—but rather to place the current situation within a historical framework of probabilities.

An investor who understands which phase of the secular cycle the market is in is in a much better position to build or manage their wealth, choose the appropriate asset mix, and avoid complacency or, conversely, excessive pessimism.

Essentially, secular and cyclical markets represent two complementary levels of analysis of reality. The cyclical perspective explains the “when” of short- to medium-term fluctuations, while the secular perspective explains the “why” of major long-term shifts in the investment climate, valuations, and the economy.

* The above article does not constitute a recommendation regarding an investment strategy for financial instruments or issuers of financial instruments, nor does it contain any opinion regarding the current or future value of financial instruments. The information and opinions in this article are provided for the reader’s information only.