After more than fifteen years of turmoil, recapitalizations, securitizations, and strict supervision, the Greek banking sector has entered a new era. For the first time since 2008, the issue is not survival, but the steady generation of capital and its disciplined return to shareholders.

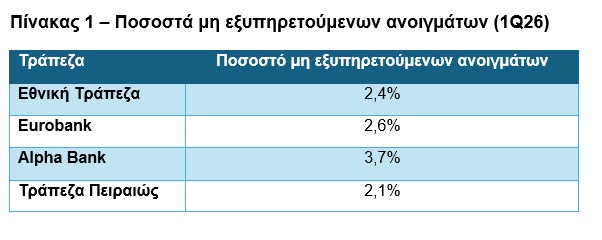

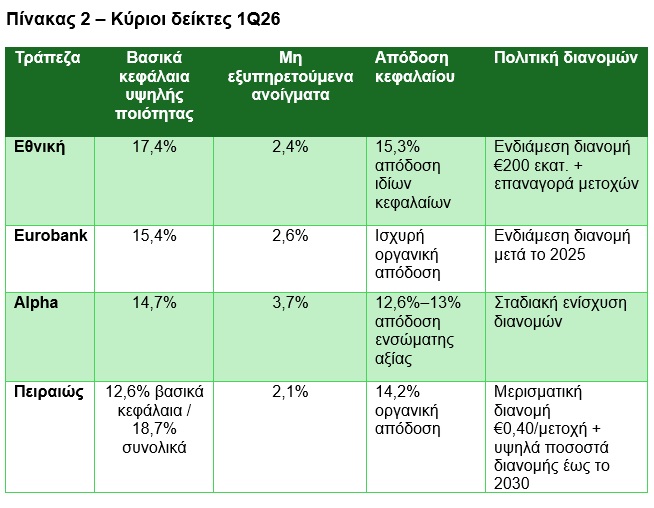

The four systemic banks now show non-performing exposure ratios -that is, loans that have not been serviced for more than 90 days- between 2% and 3.7%. Their capital adequacy remains strong, with common equity tier 1 ratios from 12.6% to 17.4%. Profitability is organic and recurring. And, above all, capital distribution -dividends and share buybacks- has now become a structural element of their strategy.

Greece no longer has a banking system under restoration. It has a banking system that not only generates capital but also returns it.

The great clean-up: From 49% to 2%!

The period 2010–2020 was characterized as one that included the most intense banking restructurings in Europe. The non-performing exposure ratio had reached 49% at the peak of the crisis. The clean-up was achieved through active portfolio management, massive securitizations, strict supervision, and the state guarantee program “Hercules,” which accelerated the derecognition of problematic loans.

At the end of the first quarter of 2026, the indicators have fully converged toward the European average.

Greece is no longer a “high-risk periphery.” It is a fully cleaned-up banking market.

The new profitability: Organic, stable, recurring

The current picture of Greek banks is based on three constants: purely organic profits, an adequate capital base, and low credit risk. The figures for the first quarter of 2026 show a sector that now operates under normal conditions.

The sector is no longer in recovery, but in repricing.

The new era of distributions: Dividends and share buybacks

The decade of dividends starts now, because the three necessary conditions now exist: excess capital generation, stable asset quality, and visibility into future earnings.

The National Bank has announced a total distribution of one billion euros for 2025. Eurobank continues its policy of interim distributions. Alpha is gradually increasing the payout ratio. Piraeus has entered a phase of substantial capital return.

Greek banks did not become “dividend companies.” They became companies of capital allocation.

The interest rate environment

The high profitability of the 2023–2025 period was supported in part by the environment of higher interest rates. As the cycle normalizes, and interest rates are declining, profitability will rely increasingly on fees, wealth management, insurance products through banks, and operating efficiency.

The quality of earnings is becoming more stable and more predictable.

Valuation: From the recovery story to the story of normalized returns

Despite the significant progress, Greek banks continue to trade at a discount to European groups. The investment opportunity is based on the sector’s ability to generate a high return on tangible book value, to gradually increase payout ratios, and to achieve repricing as the market gains confidence in the durability of earnings.

The transition from a recovery story to a story of normalized returns is the central investment narrative of the decade.

The economy as a multiplier: Greece on an investment trajectory

The banking restart would not have had the same weight without Greece’s macroeconomic improvement. The European Commission forecasts growth of 1.8% in 2026 and 1.6% in 2027. The country is in an investment cycle phase, with disbursements from the Recovery Fund peaking in 2026.

The sectors that will absorb the largest financing include energy, tourism, logistics, digital transformation, and quality real estate.

Banks will not only benefit from growth, but will simultaneously constitute the economy’s leverage mechanism.

Risks: From systemic to manageable

Despite the improvement, the risks have not disappeared. Geopolitical uncertainty, Europe’s slowdown, possible pressure on asset quality from vulnerable households, delays in Recovery Fund projects, and regulatory risk remain factors that must be monitored.

Risk, however, has shifted from systemic to manageable.

The institutional dimension: The country’s maturation through the banks

The improvement of the sector does not belong to one government or one circumstance. It is the result of many years of fiscal adjustment, banking clean-up, European supervision, and the reshaping of the economy. The relationship is now two-way: stability supports the banks and the banks support growth.

Conclusion: The new banking normality

The phrase we gave in the heading of today’s article, “The Decade of Dividends Begins,” describes a reality based on results and not on expectations. Greek banks are entering a period in which non-performing exposures are at manageable levels, capital remains strong, profitability is organic, and capital return is acquiring a lasting character.

The challenge is no longer resilience. It is the maintenance of high returns in a normal interest-rate environment, while the real economy is being financed.

If this is achieved, the next decade will not simply be the decade of the banks. It will be the decade of Greece’s repositioning as a normal, investable European banking market.

Sources: Bank of Greece – Financial Stability Reports European Central Bank – Supervisory Banking Statistics Single Supervisory Mechanism – Capital Requirements and Supervisory Expectations Eurostat – Greece macroeconomic data Ministry of Finance – Recovery Fund Program Annual financial statements of systemic banks (National, Eurobank, Alpha, Piraeus) International rating agencies – Fitch, Moody’s, S&P (Banking Sector Outlooks) International investment houses – Goldman Sachs, UBS, JP Morgan (European Banks Research)

* Nicholas Havoutis has many years of experience in leading strategic financial units, having served as an executive at JPMorgan (New York), Chase Manhattan Bank (London), and Eurobank (Athens). At the same time, he has a significant presence in the media sector. Today, as head of SoZone Limited, he advises businesses and investors on international expansion, organic optimization, and mergers and acquisitions strategies.