This year’s tourist season is moving at different speeds, as geopolitical upheavals and the increased caution of travelers are creating new balances in demand, with some destinations being tested and others regaining their lost momentum.

A central characteristic of this year’s tourist period is last-minute bookings, which are expected to be the determining factor for the final picture of the season.

Despite the fact that demand for Greece as a destination remains strong, the timing of tourists’ decision-making has changed significantly, with the result that a large part of searches is now turning into bookings just a few days before the trip.

At the start of the season, in March and April, the general picture pointed to a slowdown in the pace of confirmed bookings by 25%-35% on an annual basis, with demand, however, that is, searches in hotels’ online systems whether they are converted into bookings or not, remaining at last year’s or even higher levels.

“This year’s season is turning into a puzzle. Demand for Greece this year remains strong, even in the two-month period of March - April demand was high. This is a positive sign for Greek tourism,” stressed the founder of Square Lime, Vasilis Lapanaitis.

“There is demand, tourists want to travel to Greece, they just want a ‘signal’ mainly related to geopolitical developments, which is why they are shifting their holidays to a later time. September and October are very strong months,” he added, noting that in June the trend for last-minute bookings was particularly intense.

“The booking window, that is, the period from booking to travel, has been reduced to something less than a month,” said V. Lapanaitis.

This shift in demand has also caused reshuffling in prices, with ADR (average daily rate) for the September - November period being higher by 10%-15%, in contrast to the July - August two-month period, where it records a lag of 5%-7% on an annual basis. Hence V. Lapanaitis generally forecasts occupancy similar to last year for hotels, but lower revenues due to pressure on prices.

Among the characteristics of this year’s season, as reflected in the data of the WebHotelier platform for the hotel portfolio managed by Square Lime, which has developed a portfolio of 45 hotels across Greece, are also the changes in traveler behavior that are not limited only to the booking method, but also concern the deeper motives of travel.

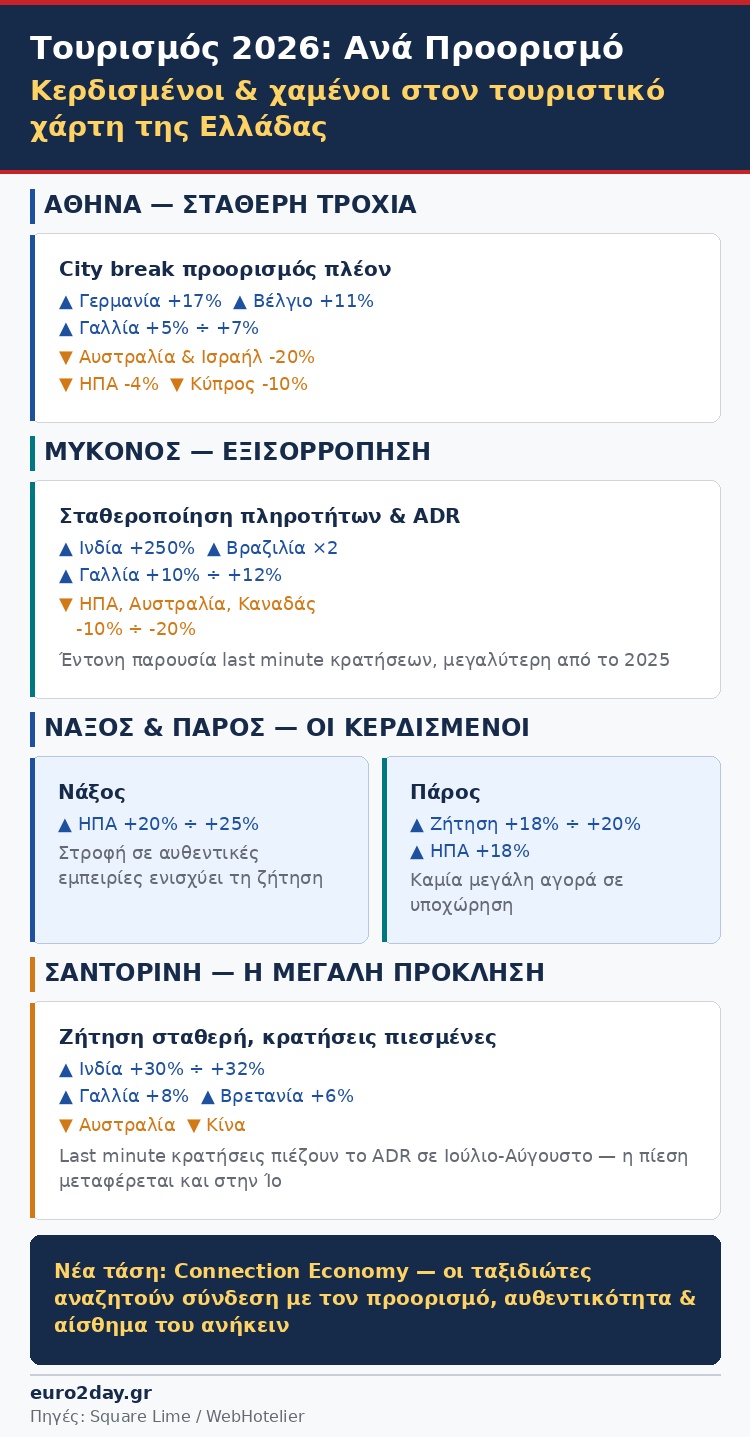

After a decade during which the search for unique experiences dominated, over the last two years the trend of the “Connection Economy” has been strengthening. Travelers now seek a meaningful connection with the destination, the local community and people, placing greater value on authenticity, the sense of belonging and the quality of the time they share.

The picture by destination

Athens: The capital is moving on a steady course this year, with demand from the beginning of the year recording a slight strengthening compared to last year. The major change concerns the composition of the markets, with Germany recording a significant 17% rise in demand, as the Greek capital has now established itself as an autonomous city break destination and not merely as an intermediate stop toward the islands, with the increase in air connections having strengthened this momentum.

The picture is also positive from Belgium (+11%) and France (+5%-7%), while on the contrary Australia and Israel are declining by about 20%, as is the US market, which shows a marginal drop (-4%). A drop of about 10% is also recorded from Cyprus, mainly due to the increased cost of airline tickets.

Of course, despite the positive picture of demand, the conversion of searches into bookings remains lower than last year, as travelers are delaying their decisions while waiting for a better picture on prices.

Mykonos: Mykonos is showing the first signs of rebalancing this year after the pressure of previous years, with the market appearing more stable in terms of occupancy and ADR. A key characteristic of this year’s season is, however, the strong presence of last-minute bookings, to a greater extent than in 2025.Demand shows significant variations by market. Particularly impressive is the rise from India, with an increase of about 250%, while Brazil records a doubling compared to last year. France is also moving upward, with an increase of 10%-12%. On the contrary, markets such as the US, Australia and Canada show a decline between 10% and 20%.

Naxos and Paros: Naxos and Paros are emerging as the big winners of this year’s season, two islands that are showing the greatest momentum this year, as they benefit from the shift in international demand toward more authentic experiences and less saturated choices.

In Naxos, demand from the US is recording an increase of 20%-25%, while the increase in bookings is similar.

Even stronger is the picture of Paros, where demand is strengthening by about 18%-20%. The US shows an increase of about 18%, while a significant rise is also recorded from Canada and Britain. A characteristic of this year’s period is that there is no major market showing a decline, a fact that differentiates Paros from other popular destinations.

Santorini: The island constitutes the biggest challenge of this year’s season. Although demand is moving at about the same levels as last year, searches in online systems are not being converted to the same extent into confirmed bookings, creating pressure on the market.The dominant trend in Santorini as well is the sharp increase in last-minute bookings, mainly for July and August, a development that negatively affects ADR and limits the ability to maintain higher prices.

India is moving upward, with an increase of about 30%-32%, while Brazil also shows a positive picture, although from a lower base. France is strengthening by about 8% and Britain by 6%. On the contrary, a decline is recorded from Australia, while the decrease from other markets such as China is more limited, which remains lower compared to the past.

The pressure recorded in Santorini is also affecting neighboring destinations, with the characteristic example of Ios, where May was characterized as a difficult month for tourist traffic.