Despite the strong rally of the first half, a significant number of Euronext Athens-listed companies continue to trade at price-to-book value (P/BV) ratios that remain low both in absolute terms and — above all — compared with their foreign competitors. This emerges from the relative valuation data of Beta Securities (closing July 2, 2026), which compare the Greek “map” with European and international peer groups by sector.

The interesting point is that this discount does not concern troubled or loss-making businesses. On the contrary, most of the companies that stand out show single-digit or low double-digit P/E ratios and offer dividend yields ranging from 2.5% to almost 7%.

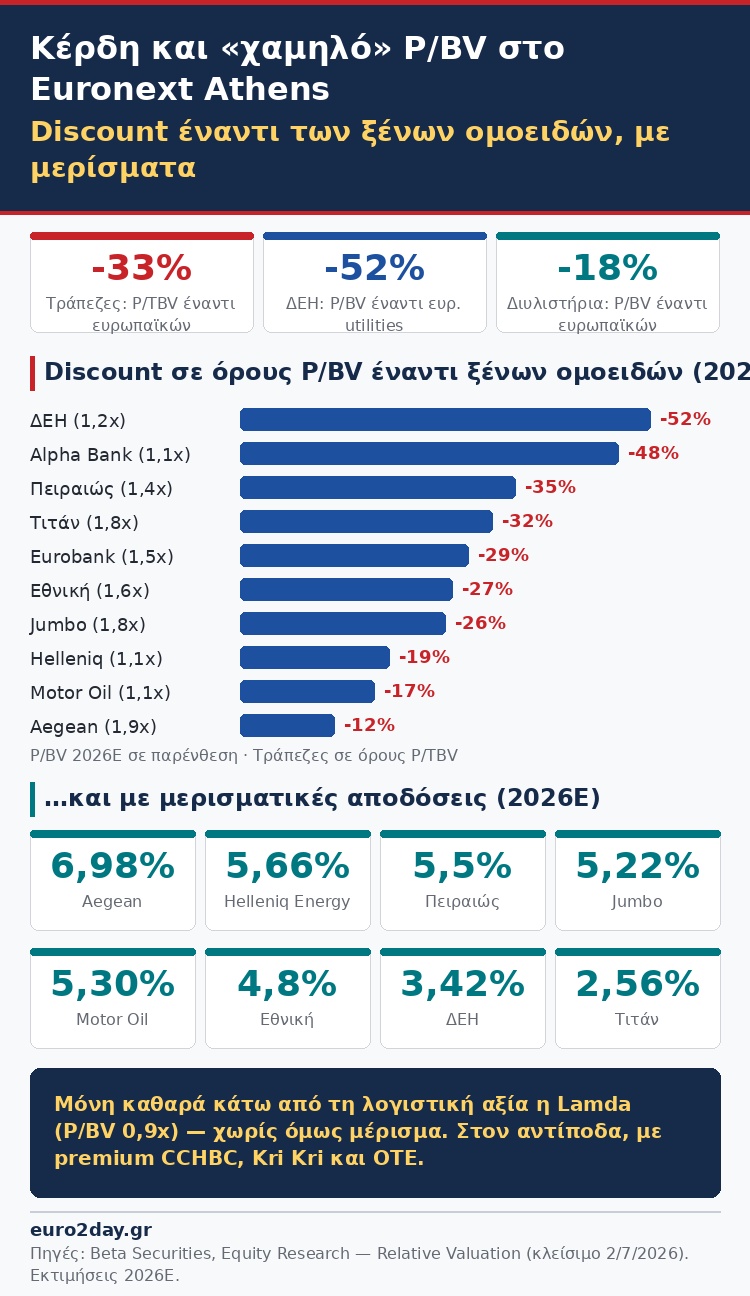

Banks: the biggest discount in the market

The four systemic banks remain the most characteristic case. With an average weighted P/TBV of 1.5 for 2026, they trade at a 33% discount to the average of European banks (2.2), while in P/E terms the discount stands at 14% (10.2 versus 11.9).

Alpha Bank shows the lowest P/TBV in the sector (1.1 for 2026), with a 48% discount versus European peers, and an estimated dividend yield of 3.8% this year rising to 5.5% in 2028.

Piraeus (P/TBV 1.4) combines a 35% discount with the highest dividend yield in the sector: 5.5% for 2026 and 7.5% for 2028. It is followed by Eurobank (1.5 and yield 3.8%) and National (1.6 and yield 4.8%), with discounts of 29% and 27% respectively.

It is also noted that the average dividend yield of the Greek systemic banks is estimated to exceed that of the European ones from 2027 onward (5.5% versus 5.1%).

Refining: single-digit P/E and yields above 5%

In the refining sector, Helleniq Energy and Motor Oil are both valued at 1.1x their book value for 2026 — with Helleniq falling to 0.8x by 2028, that is, below book value.

The discount versus European refineries reaches 18% in P/BV terms and 27% in P/E terms, as the two Greek groups trade at earnings multiples of 6.7 and 5.9 respectively for this year. The dividend yields are among the highest on the board: 5.66% for Helleniq and 5.30% for Motor Oil.

PPC: at half the valuation of European utilities

PPC is perhaps the most impressive example of relative undervaluation in book value terms: with a P/BV of 1.2 for 2026, it trades at a 52% discount to the average of European utilities (2.5). The discount in P/E terms is milder (13%), while the dividend yield is estimated at 3.42% this year, with the prospect of exceeding 5% in 2028 — at a time when the stock has already recorded a 28% rise since the beginning of the year.

Jumbo, Aegean and Titan: profitability at a discount

Three more companies with strong fundamentals follow the same pattern. Jumbo, with a P/BV of 1.8 (a 26% discount versus international discount retailers) and a P/E of just 9.6 (39% discount), offers a dividend yield of 5.22% while also having net cash — the net debt-to-EBITDA ratio is negative (-1.5). This year’s underperformance of the stock (-17.6% since the beginning of the year) makes the relative valuation even more attractive.

Aegean Airlines trades at a P/E of 8.7 and a P/BV of 1.9, at discounts of 23% and 12% respectively versus European airlines, while the estimated dividend yield of almost 7% for this year (and above 9% for 2028) is by far the highest in the sector, where several competitors do not distribute any dividend at all.

Titan, finally, is valued at a P/BV of 1.8 versus 2.6 for international cement companies (32% discount), while in P/E terms the discount reaches 47% (12.0 versus 22.7) — the largest in the sample. The dividend yield stands at 2.56%, exceeding the average of foreign peers by about 100 basis points.

The Lamda exception — and the other side of the board

The only company in the sample currently trading clearly below its book value is Lamda Development (P/BV 0.9), which however does not meaningfully distribute a dividend in the current period, as it is still in the investment maturation phase of Hellinikon.

Conversely, the Greek board also includes companies valued at a significant premium versus their peers, reflecting stronger profitability or growth momentum: Coca-Cola HBC (P/BV 4.9, 127% premium), KRI KRI (5.7, 118% premium) and OTE (4.2, 120% premium versus European telecommunications).