Few times in the last two centuries has the concentration of the U.S. stock market in a few listed companies been so great, attracting capital and investor interest.In the 1960s, AT&T stock came to account for about a 10% share of the S&P 500 stock index. The share rose to 35% together with 5-6 other companies. Today, the 8 largest companies represent nearly 40% of the same index based on data at the end of this June. We are referring to NVIDIA, Alphabet, Apple, Microsoft, Amazon, Broadcom, Tesla, Meta Platforms, whose stocks closed with losses in the same month.

Other periods when the market showed such high concentration were the era of railroads, the Nifty-Fifty companies, Japan, the internet, and today’s artificial intelligence (AI).

They say the biggest investment risks do not appear when the narrative is wrong but when everyone already believes it. Perhaps this is happening today without meaning that AI technology is a bubble. Nor does it mean that the big companies have no value.

Internet technology changed the way of communication and commerce. AI could prove to be just as, and even more, influential.

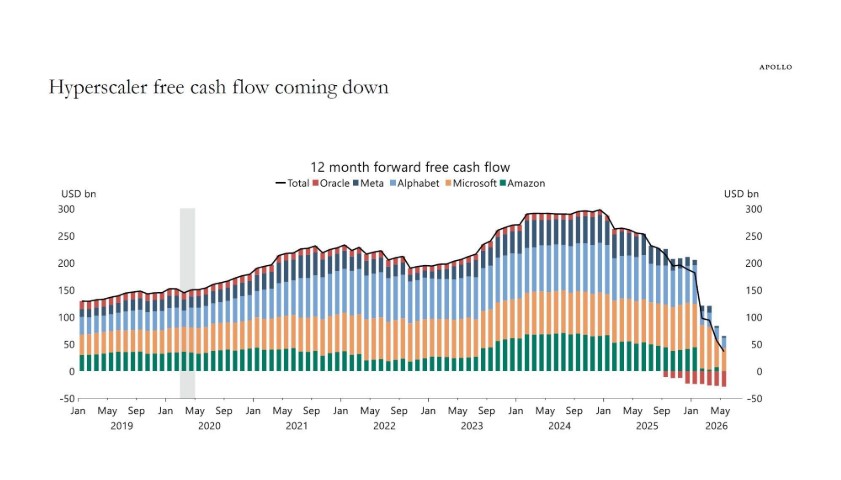

However, sometimes investors’ enthusiasm and expectations “run ahead,” making them more vulnerable to possible disappointments. Apollo gave us an idea by updating the chart below for the free cash flow of the major technology companies (hyperscalers) Alphabet, Microsoft, Amazon, Meta and Oracle over the next 12 months. Free cash flow refers to the cash left in companies after capital expenditures are subtracted from their operating activities. Unlike accounting profits, which are affected by non-cash items such as depreciation, free cash flow shows the cash in the till.

According to Apollo, the net cash flows of the above companies, which reached the highest level of $300 billion toward the end of 2024, have collapsed to close to $40 billion, recording a decline of around 40%. In fact, the biggest drop appeared in recent months. Already, Oracle’s free cash flow has turned negative while Amazon’s has almost fallen to zero.

The companies leading the race for AI investments, putting in enormous sums, are seeing their free cash flow collapse while investors are paying very high valuations to buy their shares. The expectation is that today’s investments will become large future cash flows. But what will happen if their expectations are disappointed, as happened in the past with other technologies?

It would not be anything unusual. In fact, the moment of the stock market crisis may come the next time it is confirmed that free cash flow is not enough for the large investments in AI.