SYRIZA: Pavlos Polakis (and earlier Nikos Pappas) gave Socrates Famellos a ten-day ultimatum to reach an agreement with Alexis Tsipras on “coordinated” (i.e., inter-party) electoral cooperation.

If he doesn’t succeed, what then? “If he tried and failed, fine; we’ll discuss what to do next,” explain their friends within the party.

What if he didn’t even try? This is where I need your input, because the answers vary: “The Central Committee should meet again,” says one; “We should table a motion of no confidence against Famellos,” argues another; “We should call for an extraordinary congress,” adds a third.

The truth is that whatever they demand or push for, the leadership group around Famellos holds the majority in the Central Committee. This was proven on Sunday with the Central Committee’s decision—you know, the one that says, “We remain a party but will not run in the elections, because we must stand by Alexis’s ELAS.”

SYRIZA II: Will the minority manage to become a majority in ten, maybe fifteen, days? No. As this column reported when rumors were circulating that some 70 members of the Central Committee were considering resigning to join ELAS, the issue of mass resignations is off the table so as not to “hand over” the party to the “Polakis faction.”

If anything, the presidential majority’s strategy is cynical yet simple: to lead the Polakis-Dourou-Papas group, etc., to continuous defeats in the party bodies, forcing them to leave SYRIZA in search of or to create another political home.

What is the deadline experts are giving for all this? The last week of August. Then, they say, a permanent congress will be convened (note: delegates from last year’s regular congress will participate; no new delegates will be elected, which is why it is called “permanent”), and they will make the final decision: SYRIZA will remain a party, but without representation in the next Parliament, because in the elections it will support ELAS.

Is this possible? It is, they say, because other parties exist without having MPs. With the hope that post-election osmosis will lead to the smooth absorption of SYRIZA by ELAS, with the issue of the former’s assets having been settled by then.

For example, as is said, the Koumoundourou building can be “transferred” by a conference decision but not sold, because in such a case, the proceeds from the sale cannot be distributed to the… eligible members.

Until then, the unprecedented surreal situation prevailing in this party—which, let’s not forget, was in power seven years ago—will continue to… get on people’s nerves: consider, for example, that MPs and officials who are essentially part of (or want to be part of) the Hellenic Police will be required to appear in public under the “SYRIZA” banner.

The question of whether all this will benefit Alexis’s new venture remains to be answered—if it opens doors for them, that is.

PASOK: MEP Nikos Papandreou is also following Anna Diamantopoulou’s lead regarding the alliances PASOK will be called upon to form on election night.

As he explained (Action 24), the decision for the party to go it alone remains in effect until the polls open. If they open and the party fails to secure a majority, things will change.

“The first Sunday will show us what the next Sunday will bring,” he emphasized, predicting that between these two Sundays “something spectacular may happen in the country.”

He might be open to a discussion with Tsipras, but only if he “apologizes” for the accusations he leveled at PASOK (and then-Prime Minister George Papandreou) as he was galloping toward his 2015 election victory. And, in fact, a “sincere apology,” not “with jokes,” as he clarified.

Given that the official position of Char. Trikoupi is “either PASOK as the leading party and discussions on government cooperation if necessary, or remaining in the opposition,” her stance toward Mr. Papandreou’s view will be interesting.

Because no one believes that Nikos Androulakis will expel him…

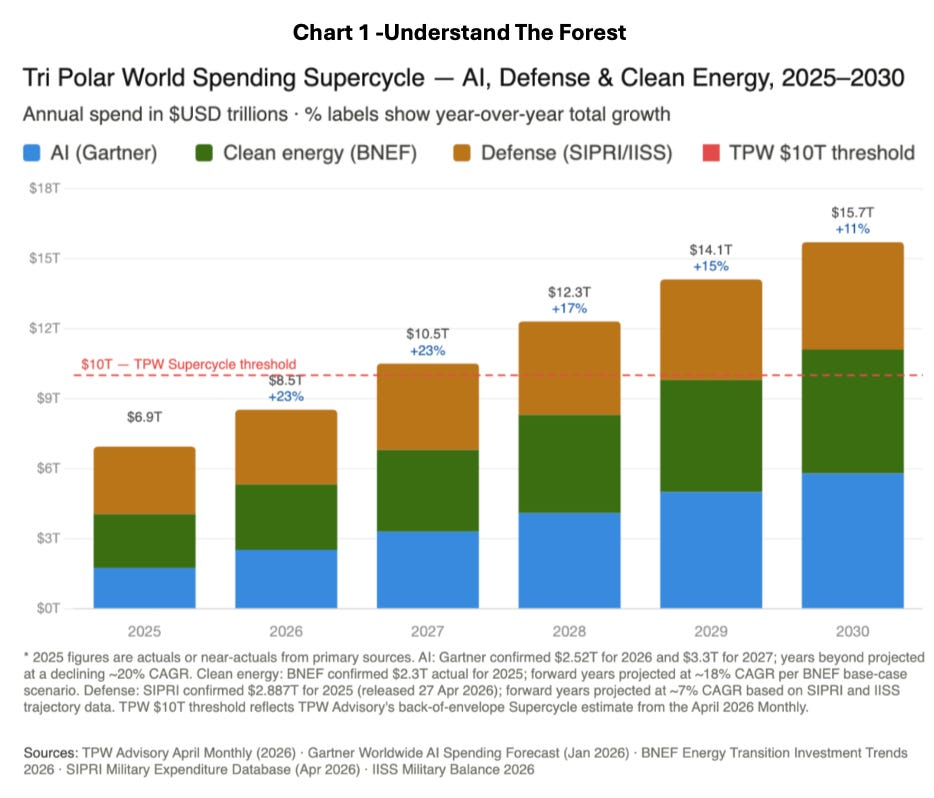

INVESTMENTS: All over the world, from West to East, there is an investment frenzy, in both the private and public sectors.

According to TPW Advisory and data from various reliable sources, we are on the cusp of an investment “supercycle” that, from the $8.5 trillion estimated for total investments in 2026, will reach nearly $16 trillion by 2030.

As shown in the following chart, the upward trend is very strong and the amounts are enormous, centered on three sectors: artificial intelligence, defense, and clean energy.

However, since the “potted plants” get watered along with the “royal plants,” such massive investments also impact other sectors that provide the raw materials and intermediate goods required for the final products. And this means there will be high demand for a wider range of industrial products and a fairly large variety of goods.

To make these investments, huge amounts of capital are needed, both equity and debt. Consequently, this creates a “momentum” in the capital markets (as is clearly the case with artificial intelligence and technology).

But also for the states themselves to channel their citizens’ savings toward investments, as the European Union has been attempting to do recently through the Savings and Investments Union.

INVESTMENTS II: For nations, the slogan “invest or die” that we used in the title stems from the economic and geopolitical competition among the three major blocs.

Competition that concerns both Artificial Intelligence (now considered the superweapon of the future, as nuclear weapons once were) and defense itself, as geopolitical conflicts become increasingly intense, as well as in clean energy, where China has clearly taken the lead.

For private investors, it has a different meaning, especially in Europe.

Consider that just yesterday, inflation of 5.2% was announced in Greece, compared to a year ago. Anyone who, during this period, had their money (even if it was a lot) in a time deposit not only failed to see it “grow,” but also lost real purchasing power—and a portion of their capital!

Perhaps not as pronounced, but certainly real, this phenomenon is also present in the other Eurozone countries. Returns without investment risk no longer exist; in many cases, as in the example above, capital protection has also ceased to exist!

“Invest or (slow) death” for a saver’s capital is the “motto” of this new era.

RISK: It would be a mistake to assume that this investment frenzy eliminates risk. The opposite may occur. In both the private and public sectors, such “races” hold great value for the winners and serious consequences for the losers.

Similarly, in both the private and public sectors, frenzied investment spending can have major consequences, especially when it is based (as is usually the case) on borrowed funds.

Such fears have been cropping up frequently lately regarding the investment programs of tech giants, but so far they have been allayed by the rapid rise in profitability and various types of “special-purpose vehicles.”

Perhaps more concerning is the phenomenon of countries that are already heavily indebted—and operating with large deficits—yet are eager to spend much more on new, ambitious investments, hoping to reverse their economic woes.

Even during periods of investment frenzy, the saying “there’s no such thing as a free lunch in the markets” holds true. The question is which securities (government or private) the investor will choose to hold when “the fat lady sings,” as the Anglo-Saxons are wont to say.

MOTOR OIL: Despite the slight deterioration in market sentiment caused by the resurgence of conflict in the Middle East, Motor Oil succeeded in pricing senior unsecured bonds at an interest rate below 4% (3.75%), in line with its target.

The liquidity raised will be used to repay the €400 million Eurobond (plus interest) maturing next month.

TRASTOR: The listed company has completed the acquisition of three properties from its “affiliate” National Insurance, for a total consideration of €38.64 million, formally confirming what had been reported in the prospectus for the Trastor IPO.

Together with renovation investments, the amount that AEEAP will allocate for the three properties mentioned above will reach €55.5 million.

Ethniki Insurance will record a capital gain of €25.75 million, which will boost its profitability for the current fiscal year. At some point, it will also acquire the Syngrou property from Ethniki Insurance, at a valuation of less than €120 million.

FESSAS: The chairman of the Quest Group commented on the prospects of the investment in Fourlis during yesterday’s General Meeting, stating that “we could help further improve the performance of this particular company. There may be synergies in certain areas, but that was not the motivation for our investment.

The motivation for our investment was that the stock is relatively undervalued. It has good management, and its ownership and management teams consist of honest and serious individuals. Some of the additional funds we received from the sale of the photovoltaic assets went to shareholders, and we used some to make an alternative investment.”

“We believe there is room for improvement at Fourlis,” said Quest CEO Apostolos Georgantzis.

On the other hand, when asked whether there would be any prospect of investing in another publicly traded company, Mr. Fessas replied that it would need to have specific characteristics. That is, serious shareholders and a management team distinguished by its past successes at other companies.

He added that it must possess the characteristics of a stock that has lagged behind for various reasons and has a broad distribution.

“These are the characteristics that made the Fourlis stock attractive. Of course, the company itself must prove that it will do well,” he noted.

TECHNICAL OLYMPIC: The Board of Directors of Technical Olympic is proposing a new two-year share buyback program to its shareholders. The proposed maximum purchase price is 4 euros and the minimum is 0.50 euros.

This will be preceded by a decision to terminate the existing buyback early, which is scheduled to expire on December 19.

DEI: The company continued its upward trend during a “red” trading session, with the stock attracting strong investor interest following the completion of the rights offering.

The stock closed at €22.4, up 1.17%, reaching levels that represent an almost 18-year high, with trading volume exceeding €23.5 million.

At the same time, it “capitalized” on the decline of National Bank of Greece, partly due to the dividend cut, to overtake it in terms of market capitalization. It is now the third-largest listed company, behind Coca-Cola and Eurobank, with a market value of €13.38 billion.

It was announced yesterday that it is partnering with Vodafone to provide fiber-optic services.

ALTER EGO MEDIA: Yesterday’s report by Euroxx Securities on Alter Ego Media (AEM) generated significant interest, with the brokerage firm raising its target price to €7.50.

The report appears to place particular emphasis on the Group’s strategic transformation from a traditional media player into a fully vertically integrated Media & Entertainment group, through its stakes in entertainment event management (Stages Network) and More.gr (a digital ticketing platform), which has no equivalent in the domestic market.

From this activity alone, the brokerage firm expects revenue of €17 million and EBITDA of €7 million for 2026, while for 2028 it estimates revenue of €25 million and EBITDA of €12.2 million, with a significantly stronger operating profit margin reaching 49%, a result of strong scale and cost synergies among AEM’s platforms.

The real gem of the report, however, lies in the streaming platform’s joint venture (with Antenna and Motor Oil). The most striking aspect of the whole story is that analysts have not yet incorporated any contribution from this specific activity into their official forecasts, while, as they emphasize, if the venture achieves its goals, this will immediately add up to 0.65 euros in additional value per share, highlighting significant hidden value associated with AEM’s investment proposal.

ELLACTOR: The stock came under a surprise attack yesterday, retreating to €1.36 with the decline reaching 7.34%. What is noteworthy is that nearly 560,000 shares changed hands, a volume not recorded in any other trading session this year.

It is worth noting that on Monday it was announced that Atlasinvest increased its stake by 5%, reaching 14.83%.

The seller was Reggeborgh.

OTE: The company’s stock is just six cents away from the year’s high it reached on May 15.

Despite a (marginally) negative opening and broader pressures in the domestic market, it closed at the day’s high of €18.80, with gains reaching 2.9%.

Recently, Euro2day.gr covered the stock, explaining that technical support is located at €18.30–18.60 and resistance at €18.87–19.20.